Market Enjoys False Sense of Calm as Iran Weighs Retaliation

Oil prices have given back some gains after jumping to a multi-month high.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

There appears to be what could be a false sense of calm in the stock market on Monday morning following President Trump’s unexpected weekend strike on Iran’s nuclear facilities.

Reports as to how effective that strike was are mixed, and while the conflict between Iran and Israel continues, we are waiting to see how Iran carries out vowed retaliation. Per reports, Iran’s parliament called for the closure of the Strait of Hormuz, a key artery for 20% to 25% of the world’s oil and natural gas, which makes it a potential chokepoint if disrupted. Whether or not that happens will hinge on Iran’s Supreme Leader Ayatollah Ali Khamenei.

After initially jumping to a five-month high early on Monday morning in response to that potential closure and the possibility of an expanded conflict in the Middle East, oil prices have tempered their gains. So far, Iran has yet to retaliate against the U.S. or its allies in the region, and that is fueling our comment about a potential false sense of calm. While diplomatic efforts are in motion to prevent a more heated conflict, we would not be surprised to see Iran look to save face on the global stage with some retaliatory efforts.

How much of an effort and whether that escalates tensions further remains to be seen.

For us, that means remaining vigilant as we get ready for today’s Flash June PMI report from S&P Global and Fed Chair Powell’s Semiannual Monetary Policy Report to Congress that begins Tuesday morning. We doubt the Fed Chair will alter his comments following the Flash June PMI data, but we will be examining it closely to see what it says about inflation pressures and demand patterns.

We also have what is likely to be a crucial week for President Trump’s "big, beautiful bill,” which looks to be getting a bit smaller as it winds its way through the Senate. As we understand it, Senate GOP leaders are aiming to hold a vote in the coming days and send it back to the House, with the aim of getting it to Trump’s desk by July 4.

We’re also moving closer to Trump’s July 9 tariff deadline. Rumblings out of the European Union point to the U.S. demanding “unbalanced, unilateral concessions.” Those same rumblings indicate the EU is also readying countermeasures subject to what happens on July 9. What we are likely to see emerge is an agreement on principles that would allow the negotiations to continue beyond the July deadline.

As you can see, we have multiple spinning plates to keep tabs on this week as we march toward the end of the June quarter and the start of the June quarter earnings season. As each of these market dominos falls, we’ll factor the repercussions into our thinking and reposition the portfolio as needed, alerting you to our thinking and any corresponding moves.

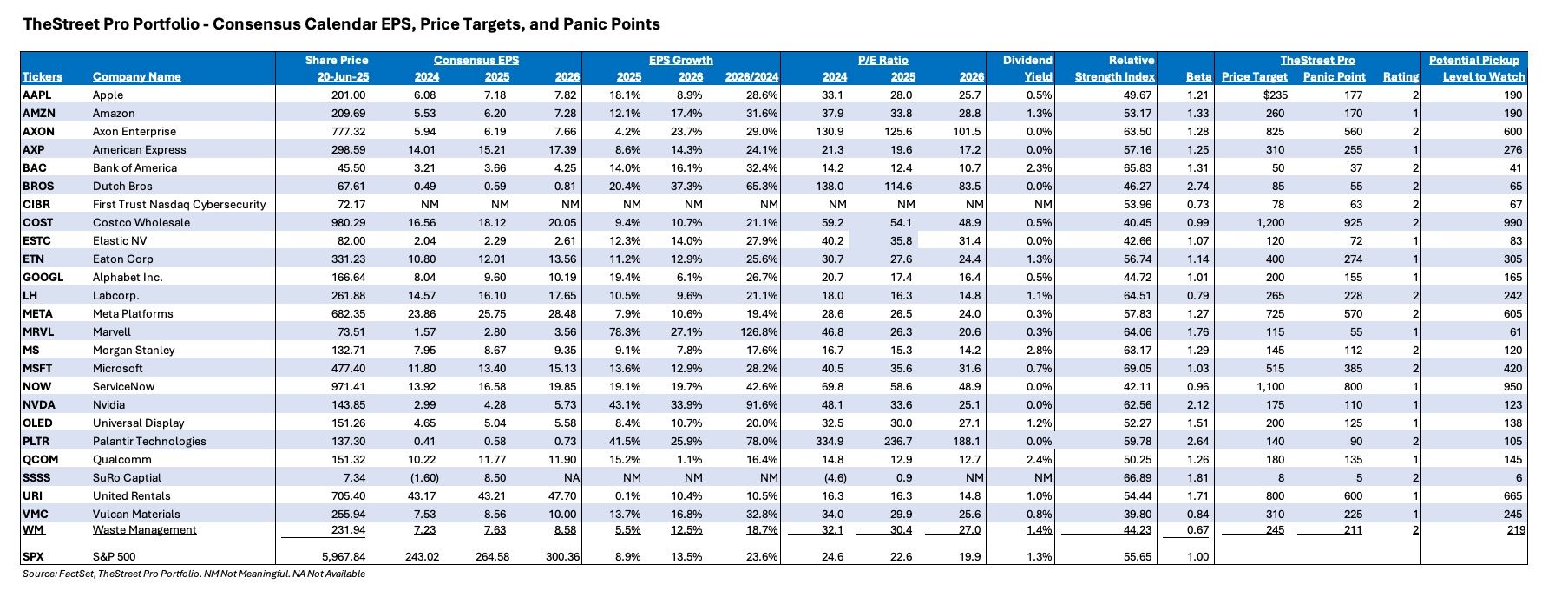

With that in mind, we’re sharing an updated Portfolio table with you on Monday morning. Week over week, there were no major changes to consensus EPS expectations for our holdings, and the same is true for their betas. We did see some changes in various relative strength index (RSI) levels, and while that is to be expected, none of the Portfolio’s positions are overbought or oversold entering this week. We’ll track those figures as well as market technicals as the items discussed above play out.

Coming Up

As we mentioned above, we have S&P Global’s Flash June PMI report, which will be out at 9:45 a.m. ET.

We also have this week’s Office Hours after today’s market close between 4 p.m. to 5 p.m. ET in the Portfolio Forum.

And ahead of this week’s "Stocks & Market" podcast with Cameron Dawson, chief investment officer at NewEdge Wealth, we’re collecting member questions. Feel free to drop them in the Comment section below, and we’ll be sure to fish them out.