Weekly Roundup: Market Adjusts to Trump Uncertainty While Fed Has More Work to Do

Amid an evolving landscape, we made multiple moves with the portfolio this week.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Coming into the week, we, like the rest of the market, were bracing for the outcome of a few potentially market-moving events. These included:

- President Trump delivering the reciprocal tariffs he teased last week and over the weekend.

- The January CPI and PPI reports, which based on other January data, had a high probability of surprising to the upside, making them the latest in a growing series of data showing inflation pressures remain.

- Fed Chair Powell delivering back-to-back testimonies in Washington, with one of those just hours after the January CPI report.

- Another wave of corporate earnings.

Powell’s first day of testimony on Tuesday was as expected, but the hotter-than-expected January CPI report Wednesday morning led him to say the Fed has more work to do. The combination of those comments and the January core CPI coming in at 3.3% on a year-over-year basis, well ahead of market expectations, pushed Treasury yields higher. It also pushed out the market's timetable for the Fed’s next rate cut well into the back half of 2025.

Heading into Thursday, the market was lower for the week and waiting for Trump’s reciprocal tariffs. That afternoon the president signed a measure directing the U.S. Trade Representative and Commerce Secretary to propose tariffs on a country-by-country basis with the intent to rebalance trade relations. Rather than the immediate or even near-term impact many expected, including ourselves, the process could take weeks or months, which means there is no clear date for when they would take effect. Much like we saw when Trump extended tariff implementation for Mexico and Canada, the market breathed a sigh of relief in response.

The message this week is that while we follow the data, we also have to be mindful of Trump’s comments and recognize his deal-like nature even as he seeks to keep his opposition off balance. We’ve also noticed consensus 2025 EPS expectations for the S&P 500 have moved lower in recent weeks to $271.45 from $274.19 about a month ago.

While a modest decline, mixed with the S&P 500 bumping up against its all-time closing high of 6118.71, its P/E multiple is back above 22x. Reading between those lines, EPS growth this year is now expected to be around 12.5%, down from 14.5% a month ago. We interpret that as folks paying more for slower growth, a combination we are not fans of.

While the pushout in Trump’s reciprocal tariffs led us to dial back our inverse ETF exposure, some prudent register ringing this week puts our cash position at more than 9%. Add in the smaller inverse ETF positions, and that brings our potential sources of near-term capital to around 11% of the portfolio’s assets.

As we discuss in The Week Ahead section below, we have some key February data coming. We will also start to hear from retailers and other retail-facing companies, and what they say about the consumer as well as the impact of U.S.-China tariffs could lead to a further softening in expectations.

While we wait for that to unfold, we’ll continue to follow the data, remain focused on the medium to longer-term opportunities and be mindful of the potential short-term volatility that Trump can cause in the markets. We will also continue to lean into our strategy of focusing on companies benefiting from pronounced tailwinds that are poised to deliver superior earnings growth. With that in mind, we would not be surprised to see some shake-up in Portfolio Bullpen.

Enjoy the long weekend, but be sure to check back for the next edition of "ripped from the headlines" confirmation points for our thematic strategies on Saturday. On Sunday, get ready for a different kind of interview with Mr. Microsoft himself – Bill Gates.

Catching Up on the Portfolio This Week

While the the TheStreet Pro Portfolio took its share of lumps this past week, as of Friday's close it is still ahead of the S&P 500’s year-to-date performance, although the level of outperformance is smaller than it was earlier this month. That narrowing was fueled primarily by shares of The Trade Desk TTD, Lockheed Martin LMT, and Applied Materials AMAT. Helping the portfolio keep its outperformance going, however, was the more than 20% jump in Dutch Bros BROS shares as well as high single-digit gains this week from Apple AAPL and Nvidia NVDA. Aiding those were gains in several holdings that were not as pronounced but still well ahead of the S&P 500 for the week.

Ahead of Fed Chair Powell’s congressional testimony on Tuesday and Wednesday, and the January CPI report sandwiched between those appearances, we held off making any moves with the portfolio. While we expected to see a hotter core CPI print, which we did get, we did not want to step in front of the market pushing out its expected rate-cut timing, which it did.

Wednesday night we received simply stellar results from portfolio workhorse Dutch Bros, but the subsequent jump in the shares was counterbalanced by the post-earnings report drop in Trade Desk shares. What we saw in terms of reduced profitability and red flags about the management team led us to downgrade TTD to a Four rating. Our plan is to utilize a rebound in the shares from being oversold as a source of funds for the portfolio.

Thursday morning, we rang the register again, locking in another slice of very big gains in Costco COST, the First Trust Nasdaq Cybersecurity ETF CIBR, Waste Management WM, Meta META, and Dutch Bros. As we made those moves, we boosted our BROS target to $85. In the same Alert, we also shared that ServiceNow NOW, and American Express AXP were on our radar.

In response to slower-than-expected near-term revenue for Applied Materials, owing to export control curbs to China, we trimmed our price target to $205 from $210 and discussed what it would take to revisit our Two rating. Following comments from President Trump that make the outlook for defense spending murkier, we downgraded shares of Lockheed Martin to a Three rating, which indicates we are in a holding pattern with the shares until we have greater visibility. As we outlined in the Alert, should we see LMT shares rally and move out of oversold territory, but the cloud of uncertainty remain, we may opt to lighten the portfolio’s exposure.

On Friday we also "exchanged" some of the portfolio’s inverse ETF shares for ServiceNow. The move took advantage of the selloff in NOW shares despite indications of ramping AI spending among enterprise customers. We laid the groundwork for the trade in comments Thursday afternoon discussing President Trump's reciprocal tariffs that aren’t expected to go into effect until April 1. As we approach the start of Trump’s April 1 tariff data, should the prospect for further tariffs emerge, we may be inclined to call these more of these ETFs back into the portfolio to tamp down volatility and protect existing gains.

Now let’s review what others on Wall Street had to say this week about the portfolio’s holdings:

TD Cowen trimmed its price target for Applied Materials to $225 while BofA lowered its to $205, matching our post-earnings target revision.

Philips Securities lowered its rating on Amazon AMZN shares to Accumulate from Buy but upped its target to $270 from $240. Loop Capital upped its AMZN target to $285 from $275.

Price targets for Dutch Bros were raised to $90-$95 at Baird and UBS from $67-$70. We raised our target and will look to revisit it further as needed following Dutch’s March 27 Investor Day.

Piper Sandler boosted its Labcorp LH price target to $260 from $240, which puts it a few bucks below our new post-earnings target of $265.

Ahead of its upcoming earnings report, Nvidia was added to the “Tactical Outperform” list at Evercore ISI. The firm reiterated its Outperform rating and $190 target.

Following our Thursday morning downgrade to a Four rating and our decision to work our way out of the shares over time, Trade Desk shares caught a number of price target cuts with some as low as $83 (Scotiabank), some near $100 (Wells Fargo, Cantor Fitzgerald) and others closer to $112-$130 (BTIG Research, BMO Capital, Wedbush, RBC Capital, BofA).

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, February 10: 3 Big Things That Will Really Impact the Market This Week

Tuesday, February 11: How Earnings From Super Micro, Others Can Impact Our Holdings

Wednesday, February 12: How Earnings From Super Micro, Others Can Impact Our Holdings

Thursday, February 13: It's Time for Our Latest Members-Only Portfolio Quarterly Call

Friday, February 14: Think Prices are High? Why Inflation is About to Get WAY Worse! (Taped last week when Chris was in New York, but published on February 13 by ITM Trading)

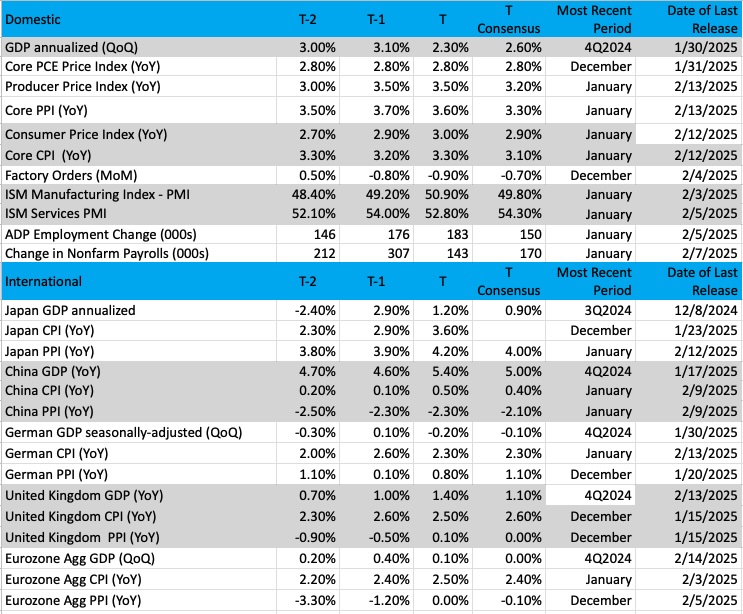

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: The Invesco QQQ ETF (QQQ)

Without question, the broader stock market performs well when technology names, specifically the Nasdaq 100 (NDX) are rising, which is captured in the Invesco QQQ ETF QQQ. The biggest names are in this index, and yes, the Magnificent 7 are the largest representatives in the ETF. But the other 93 names are faring well on their own, and that broader participation from other names is a healthy condition for the markets.

Not shown here is relative strength, which sports a solid 78 rating in the Investor’s Business Daily ranking. What does that mean? This index is doing better than the S&P 500 on a relative basis and has been for the last month. That is bullish. Even more, the money flow (bottom pane) has been improving since the start of the year and is at its highest point since mid-December. Strong money flows from fund managers and big banks signal confidence and strength in the QQQ.

Stochastics (momentum) are also moving higher and are nearly embedded. What does that mean? Simply put, when an embedded condition exists then we see the dip buyers enter the market, adding stocks on the breaks (dips), which eventually produces higher lows in the chart, supporting a bullish trend.

Those candles in the top pane have been blue or teal for nearly the entire month, which reflects bullishness in the price chart according to the GoNoGo composite of indicators. All in all, even with only a handful of big names left to report earnings from the Nasdaq 100 (Nvidia is the biggest one remaining) it is good to see the QQQ starting to lead, which may guide other indexes to join the party.

The ETF is less than 1% away from an all-time high. Through the first six weeks of the year, QQQ is sporting a solid 5% gain, a stellar move following spectacular gains in the prior two years.

Other charts we shared with you this week were:

Monday, February 10: S&P 500 - Bulls Are Losing Their Edge

Monday, February 10: American Express (AXP) - A Rest Before a Move Higher?

Tuesday, February 11: Waste Management (WM) - One Person's 'Trash' Is Another Person's Treasure

Wednesday, February 12: Trade Desk (TTD) - The Trade Desk Is Not Showing Us 'the Money' Just Yet

Thursday, February 13: Applied Materials (AMAT) - A Holding Hits Resistance Before Earnings. Now What?

The Week Ahead

We catch a little bit of a break next week with U.S. equity markets closed on Monday for Presidents' Day. While nice, that does mean an extra day for weekend developments to occur and set the tone for how we begin the second half of the current quarter. So no one’s reading between the lines, this means potential Trump comments on a wide array of topics from trade to Israel-Gaza, Russia-Ukraine, and all things in between.

Despite the holiday, three Fed speakers are expected on Monday with a steady flow continuing throughout the week. This week’s hotter-than-expected January CPI and PPI prints led Fed Chair Powell to comment the Fed “has more work to do.”

Barring a collapse in GDP expectations our take it those Fed heads will largely reiterate the message. Given the data, it’s hard to see how their comments can be meaningfully different. Even after Friday’s disappointing January Retail Sales report, the rolling GDP forecast we track from the Atlanta Fed still pegs the U.S. economy growing at a 2.3% clip so far this year.

Along those lines, we’ll be reading through the Fed’s latest meeting minutes next Wednesday afternoon, but given the timing of those January inflation reports we doubt they will be market-moving. One piece of data that we do think could be market-moving next week is the February Flash PMI report from S&P Global. As we’ve discussed with you before, the Flash data brings the first hard look at the corresponding month.

In this case, that means an early look at inflation pressures and whether they have improved, strengthened, or match what we’ve seen in recent months — sticky at elevated levels. We’ll also be looking for initial comments and reactions to Trump tariffs and whether they may have spawned some pull forward in purchasing activity, especially given China’s retaliatory response.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, February 17

· US Equity markets closed

Tuesday, February 18

· Empire State Manufacturing Index – February (8:30 AM ET)

· NAHB Housing Market Index - February

Wednesday, February 19

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Housing Starts & Building Permits – January (8:30 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

· Fed Meeting Minutes (2 PM ET)

Thursday, February 20

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Philly Fed Index – February (8:30 AM ET)

· Leading Indicators – January (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, February 22

· S&P Global Flash PMI – February (9:45 AM ET)

· Existing Home Sales – January (10:00 AM ET)

· University of Michigan Consumer Sentiment Index (Final) – February (10:00 AM ET)

International

Tuesday, February 18

· UK: Unemployment Rate – December

· Eurozone: ZEW Economic Sentiment Index - February

Wednesday, February 19

· China: House Price Index – January

· UK: Inflation Rate – January

Thursday, February 20

· Germany: Producer Price Index – January

· Eurozone: Consumer Confidence (Flash) - February

Friday, February 21

· Japan: Jibun Bank Flash PMI – February

· Eurozone: HCOB Flash PMI - February

· UK: S&P Global Flash PMI - February

Even though it’s an abbreviated trading week, we’ll start it off with quarterly results from Vulcan Materials VMC. Comments from United Rentals URI and others, including Vulcan competitor Martin Marietta MLM, set the stage for Vulcan’s results. Per Martin Marietta, which reported this week, the outlook for continued cement and aggregate volume growth is favorable with the same true for pricing.

We do, however, have to recognize the winter weather that has plagued parts of the country and the role that could have in Vulcan’s outlook for the current quarter. Indeed, weather tends to make the March quarter Vulcan’s seasonally weakest one. The real operating leverage at Vulcan occurs in the June and September quarters given they are far more construction-friendly. That leads us to take a longer view when it comes to Vulcan. Supporting that, public highway, pavement, and street construction is expected to continue to grow 8% in 2025 to $128.4 billion. Trump’s Stargate project as well as building efforts tied to Big Tech capital spending levels also bode well for higher volumes and firm pricing at Vulcan over the coming quarters.

All of that said, given where VMC shares are trading, if we don’t see sufficient upside in the shares to at least $320 we may need to revisit our One rating.

We also have Universal Display OLED reporting after Thursday’s market close. On Friday we walked through multiple data points that argue for a favorable earnings report from the company and why we’re interested in an update on its blue materials. As we digest the report and guidance, we’ll revisit our OLED price target as needed.

Ahead of that, Apple AAPL is expected to unveil its revamped iPhone SE on February 19, which was

Outside of those two portfolio reports, comments about consumer spending from Gildan Activewear (GIL), Wingstop (WING), Cheesecake Factory (CAKE), Toast (TOST), and Walmart (WMT) will be of interest. So too will be end-market comments from Arista Networks (ANET) and Rackspace (RXT), and from Visteon (VC) about what it is seeing in the automotive market for the instrument cluster, infotainment, and other connected applications. We’ll be interested in those comments given our holdings in Nvidia NVDA, Marvell MRVL, and Qualcomm QCOM.

As we tally next week’s earnings reports, we’ll move past the 80% mark for S&P 500 companies having reported. That will allow us to better assess expectations for the portfolio’s benchmark as well as reassess the EPS growth hurdle rate to use when evaluating new candidates.

Here's a closer look at the earnings reports coming at us next week:

Tuesday, February 18

· Open: Baidu (BIDU), Fluor (FLR), Visteon (VC), Vulcan Materials (VMC)

· Close: Arista Networks (ANET), Devon Energy (DVN), International Flavors (IFF), James Hardie (JHX), Toll Brothers (TOL)

Wednesday, February 19

· Open: Analog Devices (ADI), Gildan Activewear (GIL), Philips (PHG), Wingstop (WING)

· Close: American Water Works (AWK), CF Industries (CF), Cheesecake Factory (CAKE), NerdWallet (NRDS), Tanger Factory Outlets (SKT), Toast (TOST)

Thursday, February 20

· Open: Alibaba (BABA), Bandwidth (BAND), Hasbro (HAS), Lamar Advertising (LAMR), Shake Shack (SHAK), TripAdvisor (TRIP), Walmart (WMT)

· Close: Alarm.com (ALRM), AMN Healthcare (AMN), Block (SQ), Con Edison (ED), Indie Semiconductor (INDI), Insulet (PODD), Rackspace (RXT), Universal Display (OLED)

Friday, February 21

· Open: Balchem (BCPC), Diana Shipping (DSX).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.