Manufacturing Prices Hit Multi-Year High and Stagflation Warnings Could Be Next

ISM’s manufacturing report raises flags on the economy and job creation.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Following up on this morning’s Daily Rundown video, we have both February Manufacturing PMI reports and, while they differed in some respects, both showed intensifying price pressure compared to recent months.

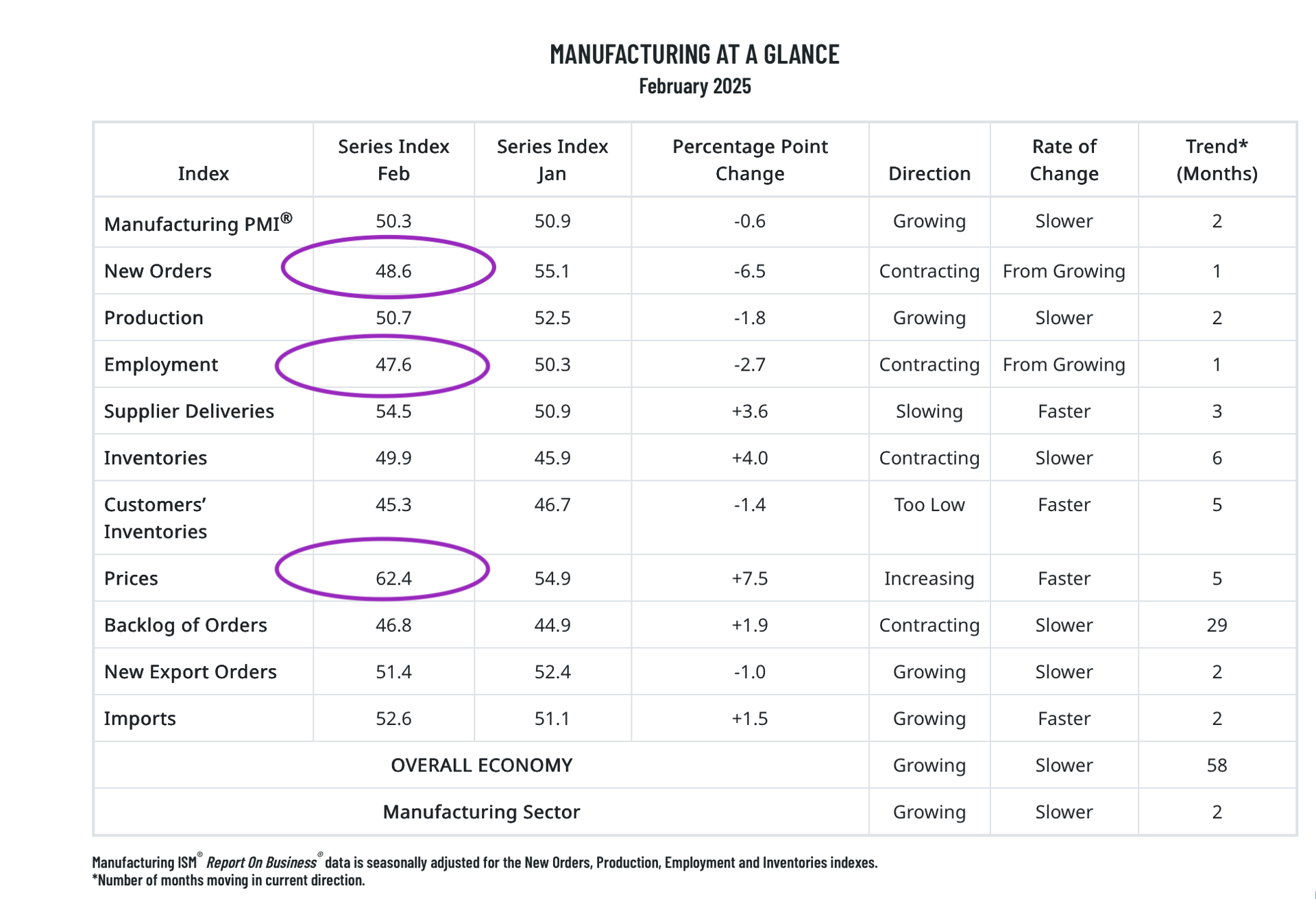

S&P’s report showed vendors were “adjusting their price lists ahead of a wider range of trade tariffs being imposed on goods and services” and that led output prices to climb as well. ISM’s Manufacturing Price Index gapped up to 62.4, its highest reading since mid-2022. Those findings will likely fuel more hawkish comments from this week’s barrage of Fed speakers, but it will be Friday’s comments from Fed Chair Powell the market will be listening to most.

As we discussed in the Daily Rundown, we have much more data coming including the February Services PMI and multiple looks at February job creation before Powell speaks on Friday. Those forthcoming reports should help us and the market get a clearer picture of the economy’s vector and velocity given the conflicting findings in the rest of S&P and ISM’s February Manufacturing PMI findings.

While S&P found the manufacturing economy turned up during the month, with new order growth coming in at its best levels in a year, ISM’s findings were the direct opposite. As we can see in the table below, the manufacturing economy slowed compared to January with new order activity dropping into contraction territory. Employment also contracted per ISM’s findings but prices, as discussed above, jumped considerably. Imports also moved higher, a likely sign that businesses were pulling forward demand ahead of expected Trump tariffs.

Reflecting on our comments shared in the Daily Rundown that the manufacturing sector accounts for 15% to 20% of GDP, ISM’s February Manufacturing PMI report is likely to push back some on last week’s drop in the Atlanta Fed GDPNow model.

However, the innards of the report are going to raise many questions about the speed of the economy just as Trump is expected to go forward with tariffs on Mexico and Canada and upsize those on China. Odds are, we will see a retaliatory response from China, and we’ll be looking into those details, but remember the Trump administration is also evaluating reciprocal tariffs on other countries with a potential April implementation date.

That suggests the price pressure we saw in February is likely to at least persist and could move higher in the coming weeks. In the back of our minds, should we see price pressure continue to rise and other signs point to a slowing or contracting economy, we wonder how long it will be until we hear cable TV talking heads warnings about stagflation.

We have a lot more poised to unfold on Tuesday and Wednesday, which means we will continue to sit on the sidelines until we have a clearer picture. We’ll also be mining investor presentations and retailer earnings for updated comments about tariff impacts, and what they mean for margins and therefore earnings expectations ahead. As we assemble those pieces, we’ll keep our eyes on the market’s valuation, especially its P/E multiple.