Manufacturing Data Misses Consensus: What it Means for the Economy

May Manufacturing PMIs show inflation elevated, nonresidential led April construction spending.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

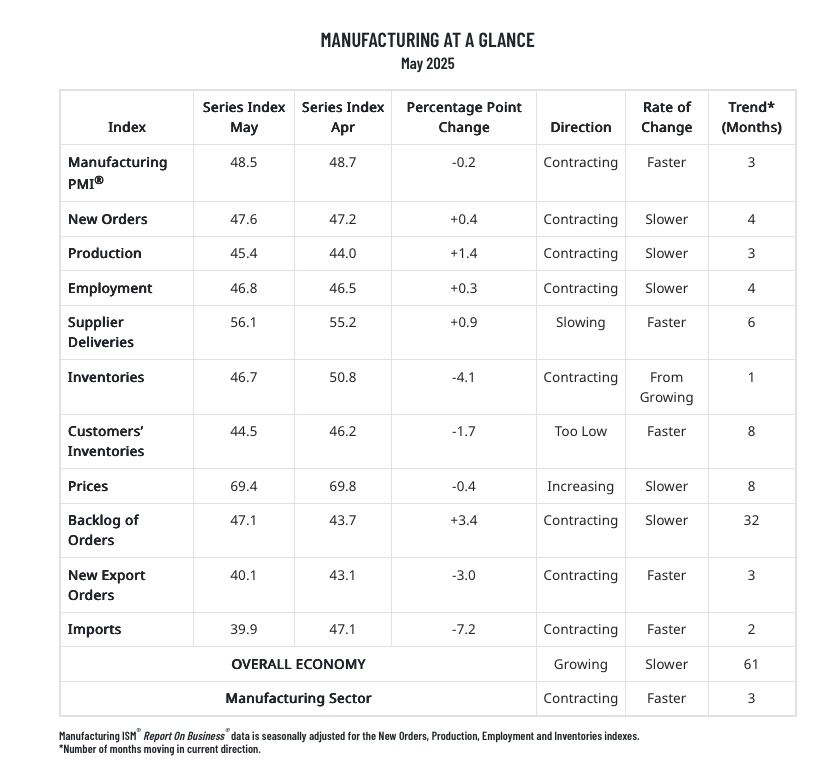

Following up on Monday's opening comments, the economic data from ISM we’ve been waiting for has been published and it shows the manufacturing sector cooled further in May as did job creation tied to that part of the economy.

ISM’s data also showed pricing pressure was little changed compared to April, remaining at high levels but not ticking as high as the market consensus called for.

Perusing the May Final Manufacturing PMI from S&P Global, we find indications of a slightly stronger manufacturing sector due primarily to efforts to front-run tariffs and supply chain concerns. That explains the pick up in new order activity, but also the record increase in stocks on inputs amid greater input price pressure. Per S&P’s findings, output charge inflation was at its highest level since November 2022, while delivery days were their longest since October 2022. Job creation per S&P for this part of the economy was “marginal.”

We would characterize the combined learnings of these May Manufacturing PMIs as largely expected when it comes to new job creation and input/output prices. The two differ on headline findings but when we look at the tick higher in ISM’s Inventories findings, it suggests S&P is more than onto something with its findings. However, because ISM’s data is used in GDP figures, we’re likely to see that robust 3.8% figure for the quarter we discussed in last week’s May Monthly Roundup tick lower.

Another reason behind our thinking that this is likely to happen is that construction Spending in April fell 0.4%, missing the expected 0.3% increase. The miss was led primarily by the sequential and year-over-year drop in residential construction. Nonresidential construction was little changed in April, but up 2.8% on a year-over-year basis led by nonresidential public construction, up 5.6% versus year-ago levels. That brings a formal confirmation to all the cranes, barriers, construction equipment and other items we see in our travels. We view this as constructive for our construction-related plays in the Pro Portfolio.

As we think about the April Construction Spending, we have to factor in weather, but we also have to remember what Vulcan Materials VMC said on its March quarter earnings call. The management team reminded Wall Street about the multiple weather challenges that plagued construction firms in the back half of last year. While we’ll have to see what the weather brings this year, we could be looking at some relatively easy comparisons. That could mean some nice monthly Construction Spending Report figures in the coming months.

As we get them and we revisit Big Tech data center spending expectations for 2H 2025 and get a sense as to what they could be for 2026, we’ll revisit our United Rentals URI and Vulcan Materials price targets. Between now and then, should we see VMC shares move past $275 and URI shares eclipse the $720 level, we’ll be revisiting their current One ratings.

After drinking all this in, let’s remember we have the May Service PMI data, as well as ADP’s May Employment Change Report, coming on Wednesday morning. That afternoon, we’ll get the Fed’s latest Beige Book and juxtaposing those findings with those outlined above will set us up for Friday’s May Employment Report.

More Pro Portfolio

- We're Cashing Out of This Holding After a Big Move

- Monthly Roundup: A Good May for the Market. Even Better for the Portfolio.

- Apple Glasses, AI Travel Agents, Aging States and More News for Investing

At the time of publication, TheStreet Pro Portfolio was long VMC and URI.