Lutnick Hints at Volatility Ahead After U.S.-China Trade Deal Update

U.S.-China trade talks produce thin results and the personalities involve could sow chaos.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We are getting ready for Wednesday's release of the May CPI report, which is expected to show headline and core inflation tick higher on a year-over-year basis, halting the sequential decline we’ve seen over the last several months.

At the same time, the market is digesting what is being called “thinly detailed outcomes” from U.S.-China trade talks. While we have been hopeful for some progress on that front, we cautioned that details would matter more than initial headlines, and it seems the market is coming around to realizing that. Per U.S. Commerce Secretary Howard Lutnick, both sides have established a framework for implementing the Geneva Consensus that aimed at restoring their trade truce and removing China’s export restrictions on rare earth elements.

The deal now awaits approval from President Trump and Chinese President Xi, but some likely remember U.S.-China trade talks from 2018 to 2019. During those negotiations, constructive in-person meetings seemed to take a step back as the negotiating teams returned to their capitals. As we move to this next step, our view remains that the ultimate details will be what matters most, but given the personalities in play, we can’t rule out some last-minute negotiations that could inject some fresh volatility into the market. Supporting that potential, Lutnick shared expectations for Trump to remove export restrictions "in a balanced way" as China approves rare earth licenses.

We are also seeing on Wednesday morning the European Union (EU) is posturing for trade negotiations with the U.S. that could extend beyond Trump’s July 9 deadline. The shared thinking is the EU sees reaching an agreement on the principles of a deal by July 9 as a best-case scenario, which would allow further talks to work out the details. That seems to follow the path laid out by current U.S.-China talks, but let’s remember that the July deadline is when Washington is set to hit nearly all the bloc’s exports with a 50% tariff, likely triggering retaliation.

Naturally, we’ll be keeping a close eye on these and related developments and what they mean for the economy, sector demand and earnings prospects for 2H 2025 and 2026. Our view has been and remains that the longer tariffs are in place and trade remains uncertain, the more likely we’re going to receive cautious guidance. Speaking at the Morgan Stanley U.S. Financial Conference on Tuesday, JPMorgan’s JPM Jamie Dimon commented that, between trade and geopolitics, there are “a lot of moving parts” but tariffs are “hitting” and we will see bigger impacts in the coming months.

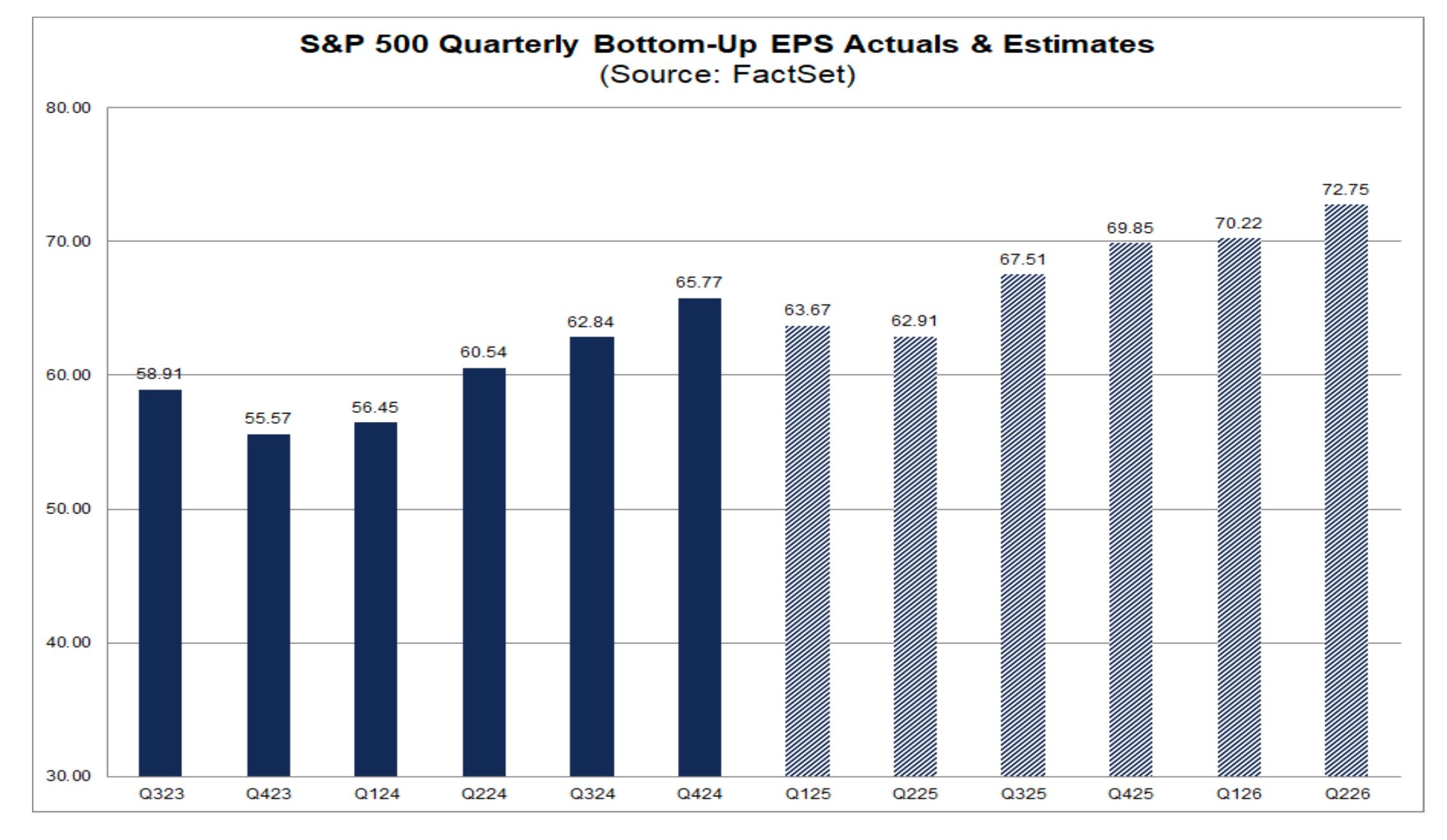

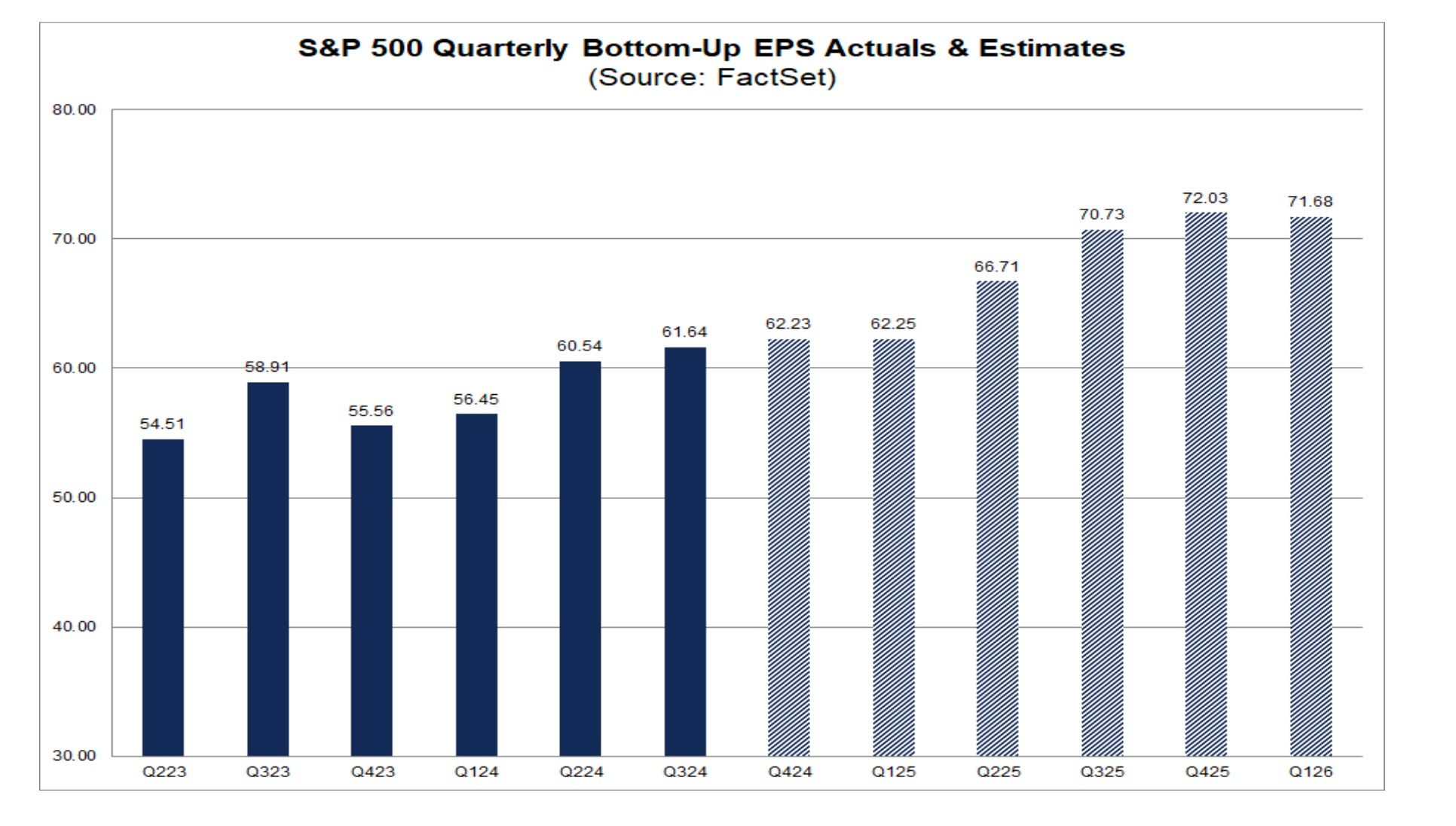

We see that supporting our thinking that, barring trade deals and their details, we are likely to see companies reset earnings expectations further for 2H 2025. So far, forecasted consensus EPS growth for 2H 2025 reduced to 8.5% exiting May from 10.7% at the end of January.

Gaming it out, more substantial cuts resulting from company guidance in the soon-to-be U.S. June quarter earnings season are a potential headwind for the market. The closer to that earnings season we get without trade deals and their details or the passage of Trump’s “big, beautiful deal” that would bring its own clarity on tax reform and other issues, the more likely that headwind becomes.

We’ll continue to track these and other developments, and position or re-position the Portfolio as needed.