Latest Jobs Figures Miss, but the Fed Has a Bigger Focus for Now

Here's where we expect the Fed to concentrate after jobs were added at a slower pace than expected by the market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

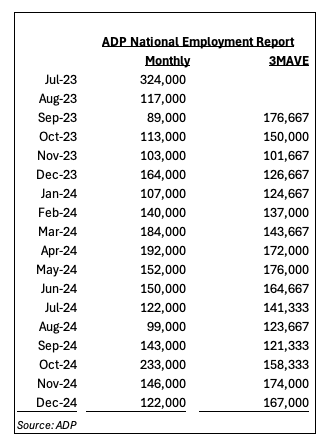

ADP’s assessment of job creation in December came in at 122,000 jobs, a slower pace compared to November’s 146,000 figure and below the market forecast of 140,000 for the last month of 2024.

The December figures were also below those for September and October, and in that vein, they can be viewed as somewhat rate-cut friendly. Why somewhat? Well, for one thing, the pace of job creation in December remained above 100,000 jobs but also, when we examine the data on a three-month moving average in the table below, the figures do not point to an economy that needs rescuing with rate cuts.

To that we can add that wage gains for December job stayers rose 4.6% year over year, while those for job changers were 7.1% higher compared to year-ago levels. While down month over month, those levels still suggest wage pressures remain, echoing comments in S&P Global’s December Service PMI report.

With the employment picture holding up, the Fed’s near-term focus will likely remain on inflation. Fed Chair Powell made it very clear at the Fed’s December policy meeting, and we suspect that message will be clear when we read through the meeting minutes for that meeting on Wednesday afternoon.

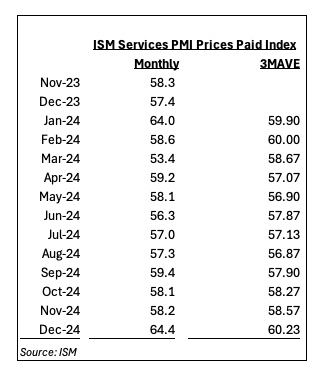

That message is also likely to be reiterated by several Fed heads making the rounds on Wednesday and Thursday, especially following what we saw in the price data from Tuesday's December ISM Service PMI. Whether we look at the monthly trend or the three-month moving average (3MAVE), it’s pretty clear inflation pressures in the service part of the economy have not been cooperating with the Fed’s objective.

In his comments on Wednesday, Fed Governor Christopher Waller shared the following:

"Based on the most recent Summary of Economic Projections, the median of policymakers' expected appropriate policy rate this year implies two 25 basis point cuts. But the range of views is quite large, from no cuts to as many as five cuts for different FOMC participants. As always, the extent of further easing will depend on what the data tell us about progress toward 2% inflation, but my bottom-line message is that I believe more cuts will be appropriate."

We would be surprised if the ISM data we shared above doesn’t lead some of the more dovish Federal Open Market Committee (FOMC) members to reconsider the number of potential rate cuts this year. Currently the market now only sees one rate cut and the timing for that has been pushed out to June or July from March just a week ago.

We will also have to be a little careful in reading the Fed December meeting minutes later on Wedensday. That thinking stems from the reconstitution of the FOMC that includes four new 2025 voting members — Boston Fed President Susan Collins, Chicago Fed President Austan Goolsbee, St. Louis President Alberto Musalem and Kansas City Fed President Jeffrey Schmid.

Of the four, according to InTouch Capital Markets, Goolsbee is the only dove and that could mean a tougher tone ahead, especially if next week’s December CPI and PPI figures confirm what ISM’s recent Service PMI pricing data shows. This also means we’ll want to pay closer attention to the overall tone of Fed speaker comments leading up to the Fed’s January and March policy meetings.