Latest Economic Data Show Slow Jobs Growth, Inflation Picking Up… Again

There's more data to support the economy humming, but not any near-term rate cuts.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

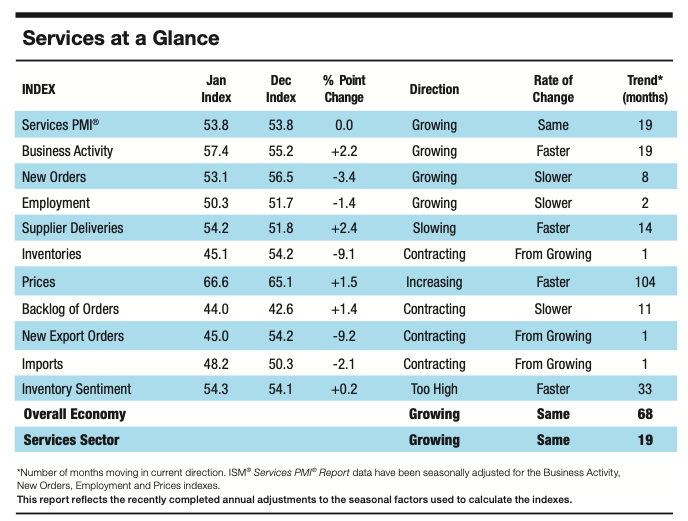

While we get our next set of stock-specific comments ready, let’s quickly discuss Wednesday's January economic data and what they say about job creation and inflation during the month. Remember, Monday’s January Manufacturing PMI from ISM showed a “better” but still contracting employment market for that part of the economy and inflation pressures perking up.

Wednesday's January ISM Services PMI lacked the strong pick up in New Order growth we saw for the manufacturing part of the economy, but at 53.1, it’s still growing at a nice pace. However, that bright spot was overshadowed by the downshift in job creation for the Services economy, and mashing it with the January Manufacturing PMI findings, that explains the miss we saw in Wednesday's ADP January Employment Report.

If you missed that data from ADP, it found 22,000 jobs were created in January, down from 37,000 in December, and well below the market forecast of 48,000. Pulling the camera back a bit, we find that the January figure was another big step down from the one we saw in December and the 74,000 jobs created in November.

This continues the narrative of a slower-growing jobs market, but at least so far, not one that is falling into net job losses. In other words, something that isn’t going to spur the Fed into action, especially when inflation pressures are rising.

To the January Manufacturing PMI figures that showed that, we can add the leg up in the Prices component of today’s January Services PMI from ISM. And then there was this found in Wednesday's final January Services PMI report from S&P Global:

"Higher supplier costs and payroll expenses also added to upward pressure on company operating expenses. In line with the trend for overall costs, selling prices increased to a lesser extent than in December, albeit also still higher than the historical average. Firms often sought to pass on their higher input costs to clients, though the rate of growth moderated amid reports of strong competition limiting pricing power."

So long as inflation pressures are ticking up, that is going to restrain the Fed from delivering additional rate cuts… at least as long as Chair Powell is around and subject to the data, potentially even after that.

We will continue to monitor comments in the second part of the current earnings season. Reading between the lines with S&P’s pricing comments above, it sure sounds like margin pressure is building. We saw signs of that at Chipotle (CMG) on Tuesday night as its restaurant-level margins slipped to 23.4%, falling 140 basis points compared to the year-ago quarter.