June Manufacturing PMI Stokes Stagflation Fears

Plus, here's what the May Construction Spending report means for four holdings.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

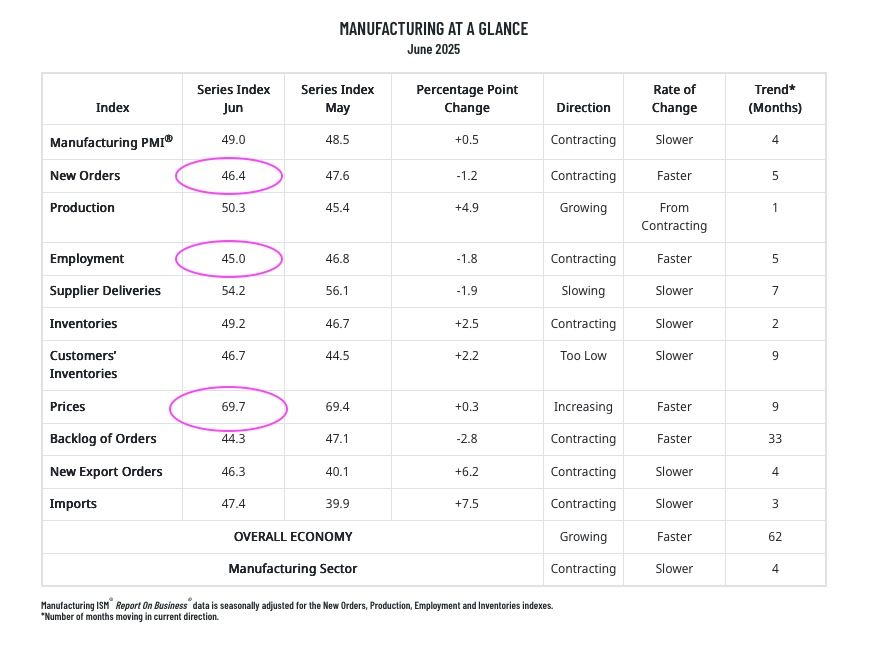

We began the September quarter today, and right on time, the flow of June economic data started. What it showed is the manufacturing economy slowed further while inflation pressures ticked higher.

Some may say that’s a recipe for potential stagflation, especially since new order figures softened further, as did manufacturing employment. But, we must remember that part of the economy only accounts for ~10% of GDP.

So, while the results of ISM’s Manufacturing PMI report will be a factor in dialing back rolling GDP forecasts for Q2 2025, we will place more weight on what ADP’s June Employment Change Report says Wednesday, as well as the findings in ISM’s June Services PMI report and the Labor Department’s June Employment Report on Thursday. We expect inflation pressures will tick up in ISM’s June Services PMI report, and we’ll have a better indication of June job creation after we have ADP’s reports in hand.

We also received the May Construction Spending report, which we track for the Pro Portfolio's holdings in United Rentals URI, Vulcan Materials VMC, Eaton ETN, and to a lesser extent, Waste Management WM. On both a sequential and year-over-year basis, overall construction spending dipped in May, due to declines in residential construction, especially private residential construction, and more modest declines in overall non-residential construction. In reviewing those figures, we should keep in mind trends in housing starts data, which explains the residential construction findings. We should also keep in mind May weather as 13 states experienced one of their five wettest Mays on record, and the month had two notable severe weather outbreaks between May 15-20.

A bright spot in the May Construction Spending report was the 3.1% year-over-year increase in public, nonresidential construction, and favorable year-over-year spending in private power construction. The former speaks to the ongoing infrastructure spending that has been a staple for our URI and VMC positions, while the power spending data is the latest supporting data point for our ETN shares.

Because we won’t receive the June Construction Spending report until August 1, the next catalyst for those four Pro Portfolio holdings will be a combination of their June-quarter earnings and those from other construction-related companies such as Caterpillar CAT, Terex TEX, Tutor Perini TPC.

At the time of publication, TheStreet Pro Portfolio was long URI, VMC, ETN, and WM.