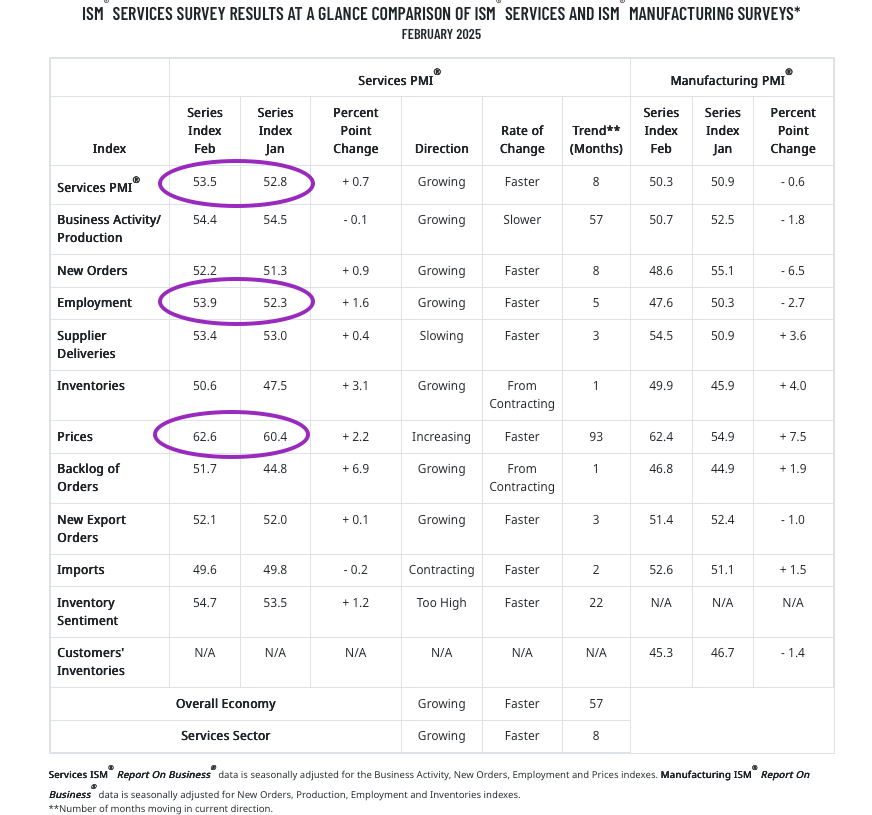

ISM Services Show Economy Is Better Than Feared

However, inflation persists and there is room for Friday’s February Employment Report to disappoint.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Following up on our moves with the Portfolio from earlier on Wednesday, let’s take stock of the morning’s February economic data, which offered a mixed picture of job creation but also showed the Service sector performing better than indicated by S&P Global’s Flash Feb PMI report.

Seeing that better performance as well as the uptick in new orders and backlog of orders tell us the economy did not fall off a cliff in February.

We did see inflation pressures tick higher, with ISM’s Prices sub-index reaching 62.6 from 60.4 in January and S&P’s report noted rising input costs. Mixed with similar findings in the February Manufacturing PMI report suggest next week’s CPI and PPI data for February isn’t going to show any dramatic improvement. To that, we can add the sticky wage inflation we saw today in ADP’s February Employment Change report that showed wages for job stayers still up 4.7% year over year with those for job changers up 6.7% compared to year-ago levels.

Our view after assessing the data is that the economy is on better footing than feared, but inflation remains and that will keep the Fed on the sidelines when it comes to rate cuts. While some may be tempted to consider Fed rate cuts this year, remember several quarters ago that Fed Chair Powell warned there could be some pain as part of getting inflation down to the Fed’s 2% target. Granted, efforts to shrink public sector employment at the Federal level are a new wrinkle into all of this, and we expect to see that impact before too long in monthly jobs data.

Aggregating ISM’s Manufacturing Employment reading that fell to 47.6 in February, its Service Employment figure that ticked higher to 53.9 from 52.3 in January, and the miss for ADP’s February Employment Change Report (77,000 versus the expected 140,000), we would not be surprised to see a miss relative to market expectations for Friday’s February Employment Report. The current consensus is 160,000 jobs being added, up from 143,000 in January. The Unemployment Rate is expected to remain at 4.0% in February.

Coming up at 2 p.m. ET, we’ll get the next iteration of the Fed’s Beige Book, an anecdotal collection of data points across the various Fed member banks. Based on the multiple February PMI reports, we expect it to reflect slower activity and continued inflation pressures. We will be interested in what is said about consumer spending, layoffs and hiring as we get ready for Friday and Powell’s lunchtime comments.