Homebuilder Names Enjoy Surprise Strength but Headwinds Await

Rising incentives and falling backlogs point to margin pressure for homebuilders and their suppliers.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We are seeing some surprising strength in the shares of homebuilding stocks on Tuesday on the heels of quarterly results from D.R. Horton DHI and PulteGroup PHM that were, by some accounts, not as bad as feared.

While both companies delivered EPS beats for their respective June quarters, we would chalk Horton’s upside surprise more toward its buyback activity than operational success, given the far greater drop in June quarter operating profit (24.5%) compared to the year-over-year decline of 7.4% for its top line. We can trace that margin pressure to elevated sales incentive levels, which the homebuilder is likely using to foster demand. Odds are the company is angling to pass that margin pressure along to key suppliers and partners like Masco MAS, James Hardie JHX and Builders FirstSource BLDR.

Pulte also saw a year-over-year drop in revenue of around 6%, but its net new orders for the quarter were more worrisome. They totaled $3.89 billion in the June quarter, down from $4.48 billion for the March 2025 quarter and $4.36 billion in the year-ago quarter. That led Pulte’s homebuilding backlog to fall to $6.84 billion compared to $7.22 billion exiting March and $8.11 billion at the end of June 2024. Like Horton, Pulte is also leaning on sales incentives to drive sales. Incentives for the second quarter were 8.7% of gross sales price, up from 6.3% last year, and on a sequential basis, up from 8.0%. That reaffirms the likelihood of added margin pressure on suppliers.

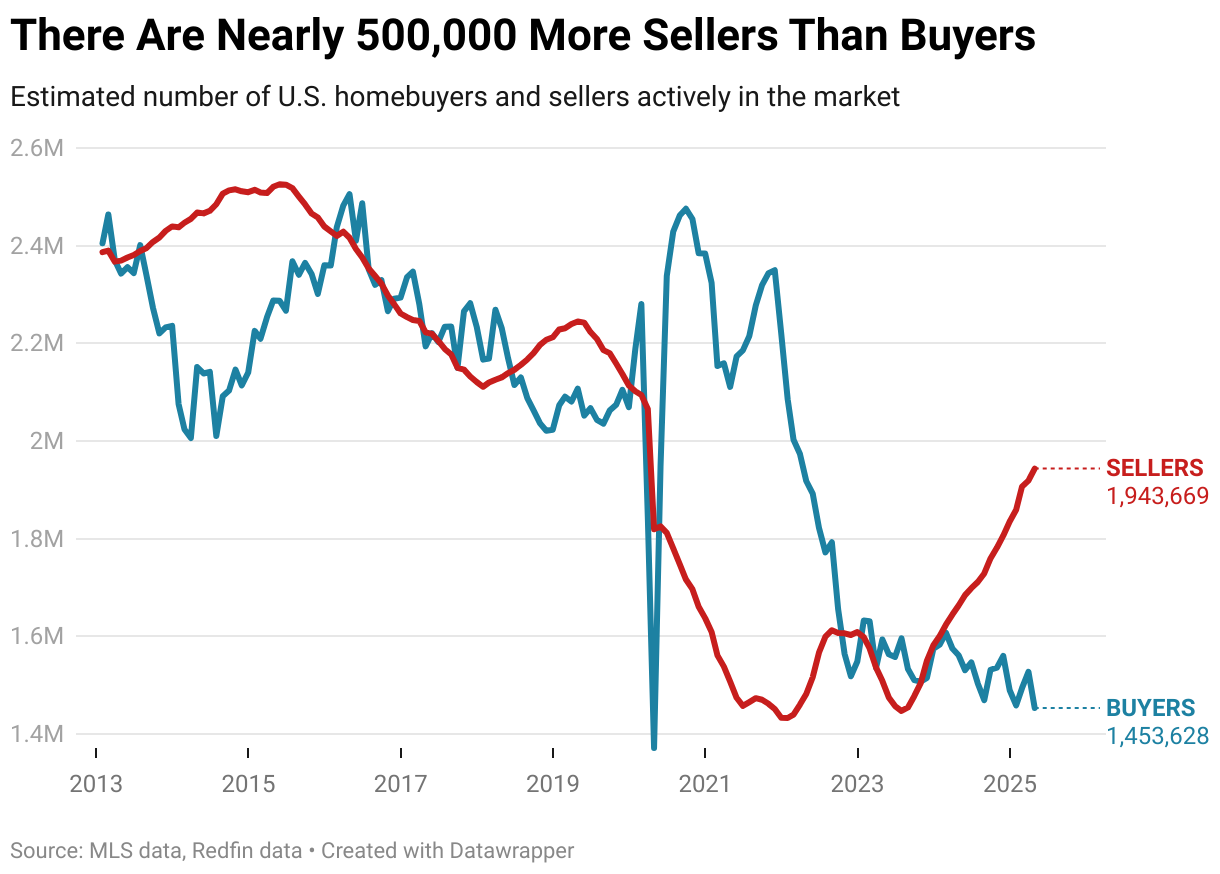

We are also reading findings from Redfin that the number of sellers in the housing market is significantly higher than the number of buyers. That glut of homes for sales is another tailwind for new home sales and explains why the use of selling incentives is likely to persist.

So if order levels are trending lower, margin prospects are facing incentive headwinds and net income is trending down on a year-over-year basis, why are DHI and PHM shares as strong as they are today?

The simple answer is the cosmetic effect of stock repurchase efforts on reported EPS that led both Horton and Pulte to report bottom-line beats. We see that as a low-quality earnings beat, but given the level of short interest on both stocks, it was enough to trigger some covering. The latest data from the NYSE pegged DHI's short interest at 7.7 million shares and 2.18 days to cover, while for PHM it was 7.8 million shares and 3.67 days to cover.

Given comments above about margin pressure as the use of incentives to move homes builds in the coming quarters, we do not subscribe to the market lifting BLDR, MAS or JHX shares today. At some point, a time will come when we will want to be long either a homebuilder or a building product stock, but that will most likely be when backlog levels firm and the use of incentives to drive home sales declines.