February Monthly Roundup: Uncertainty and Volatility Jump in Roller Coaster Market

Amid a month of turbulence were profitable gains, nimble moves and the EPS Diplomats strategy working in our favor.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

While we’ve seen pronounced moves in the CBOE Volatility Index (VIX) before, including those in April, October and November of last year, the up and down movement during February seen in the chart below explains quite a bit about investor sentiment and the market’s February performance. Peeling back a few layers also reveals why the Nasdaq Composite fell more than 3% during the month, while the S&P 500 shed a far smaller 0.5%. Let’s discuss and get ready for the final month of Q1 2026.

From the continued fretting over potential AI disruption that moved across sectors during February and renewed tariff questions to escalating U.S.-Iran tensions and seeds of worry over the private credit market, the “big winner” during the month was the VIX with its cumulative gain of 16.75%. Through it all, we purposely slowed things down, aiming to take a calm and collected approach as we asked purposeful questions to help us determine if the corresponding moves in the market were justified or overreactions. While Anthropic’s Enterprise Agent presentation on February 24 and sequential gains in Salesforce’s (CRM) bookings and contract value bolstered the argument for an overreaction, Block’s (XYZ) massive layoff news fanned those uncertainty embers.

We have shared our view that Block’s issues are more company specific, but in a volatile market filled with increasing uncertainty and hair-trigger responses, the market’s downward reaction was hardly unexpected. Some will say that is what makes the market, but we’re more in line with Warren Buffett’s famous quote about when investors should be fearful and when to be greedy.

We’ll more than agree that volatile times are challenging on multiple fronts and can get those stomach juices churning, especially when the market seems to ignore the data. It’s common to second guess decisions, but as we’ve seen time and time again, it’s even more important to focus on and follow the data. Our shares of Axon (AXON) were a great reminder of that.

With growing tensions between U.S. and Iran resulting in a wider conflict, one that is poised to propel oil prices higher, we would be surprised if the knee-jerk action in the market didn’t continue. In our view, the key word is once again “duration.” The longer the duration of this conflict, the longer oil prices are likely to be elevated, and the more likely we will see inflation pressures remain sticky, possibly even tick higher in the near-term.

We’ll want to see how the U.S.’s move in Venezuela and its oil fits in this picture, but if the duration of the conflict moves from days to weeks to potentially months, we’re going to see renewed questions about further rate cuts. Gaming it out, we doubt that is something the White House wants, in part because it would push back on President Trump’s stance that inflation has been licked but also because it could become a hot topic for the upcoming mid-term elections.

Most likely the conflict will pressure the market in the near-term, but the silver lining is that it has the potential to make for even more compelling risk-to-reward tradeoffs. As we track the conflict, this week’s economic data, and comments from the Morgan Stanley tech conference, we’ll keep that Buffett quote in mind.

Catching Up on the Portfolio This Week

Along with the market, the Pro Portfolio gave up some ground during February, despite a strong finish to the month. Standouts during the final week of the month include the 25% pop in Axon (AXON) shares and the almost 15% jump in Netflix (NFLX) . Those moves were among the highlights for us in February, and to that group we can add TJX Companies (TJX) , Welltower (WELL) , Waste Management (WM) , Costco (COST) , and Eaton (ETN) shares. We’ll discuss more in the stock-specific sections below, but those gains were mitigated by our tech positions during the month. Given the more than 3% drop in the Nasdaq Composite vs. the smaller decline in the S&P 500 during February, this should not be much of a surprise.

The EPS Diplomats basket continued to deliver outsized performance during February, putting the strategy up more than 24% year-to-date. The February move was fueled by the substantial climb in Lumentum Holdings (LITE) and solid double-digit gains in Equinox Gold (EQX) , IAMGOLD (IAG) , and SiTime Corp. (SITM) . When we reconstitute this basket next, we will be increasing the Portfolio’s exposure to this strategy. We'll have more to say on that later this month.

During the second month of 2026, we added to the Portfolio’s position in Axon shares twice, first on February 3 and again on February 10. Following the significant post-earnings pop, on February 26, we trimmed a portion of those profitable AXON shares due to some prudent portfolio management as the position size moved past the 4.5% level.

On February 9 and February 10, we picked up additional shares of SuRo Capital (SSSS) and Microsoft (MSFT) . We followed those moves a few days later by taking advantage of the parabolic move in Eaton (ETN) shares, to book a gain north of 37%. A day later, on February 13, we made a similar move with Welltower (WELL) , securing an almost 26% profit on that slug of shares.

In a move that should remind members the Portfolio can be nimble when the right opportunity presents itself, we added Netflix (NFLX) to the our stable of stocks on February 26. In the trade Alert, we explained why we saw Netflix poised to walk away from its bid for Warner Bros. Discovery (WBD) , and likelihood that would drive the shares higher. That scenario played out in our favor, allowing us to capture a nice double-digit pop in NFLX to close out February. As you’ll read about below, we are adding a Two rating on the shares, and we’ll discuss our plans for the name later this week.

The net result of those moves left the Portfolio with ~7.2% of its assets in cash. That gives us some flexibility with the current line-up of holdings, but with our plans to increase the Portfolio’s exposure to the EPS Diplomats strategy several weeks from now, odds are we have to make a few choices. That could mean exiting a current holding, or slimming our exposure to a few of them in order to make some room.

The latter would be similar to the move we made in December to free up room to begin our position in Broadcom (AVGO) by slimming down exposure to our other chip holdings. That included shedding some Qualcomm (QCOM) shares at $177, and we ultimately closed out our remaining position in at $165.13 on January 15. Those shares closed February at $142.36. With expectations for smartphone volumes to fall double-digits this year, odds are it will be at least more than a few quarters before we seriously contemplate bringing that stock or even Universal Display (OLED) back into the starting line-up.

In terms of the Bullpen, we added shares of Idexx Labs (IDXX) to the fold as a potential play on the recession-resistant spending on pet care. It's to be determined if this stock graduates to the Portfolio, but we’ll have more to say on this in the coming days. As we move through the final month of the Q1 2026, we’ll keep our eyes open for other opportunities to make profits over the ensuing quarters.

This Week's Portfolio Videos

We cover a lot of ground during the week in our videos. If you happened to miss one or more of them, here are some helpful links:

Monday, February 23: 3 Holdings Prepare to Report as Uncertainty Grows

Tuesday, February 24: How Volatility Is Impacting Our AI Plays

Wednesday, February 25: Stocks & Markets Podcast: Going Hypersonic With Starfighters Space

Thursday, February 26: Our Roadmap for a Tech-Heavy Start to March

This Month’s Podcasts and Signals

Big discussions and insights are had during TheStreet Stocks & Markets Podcast, and with Signals we share the latest news for the Pro Portfolio’s strategies. Here are some quick links to those conversations conducted over the last several weeks:

February 5: Stocks & Markets Podcast: Inside the Market’s Next Move With Lindsey Bell

February 7: 23 Portfolio Signals Across 8 of Our Themes

February 11: Stocks & Markets Podcast: The Hidden Forces Driving the New Gold Rush

February 14: We're Eyeing 20 Signals Across 7 Pro Portfolio Investing Themes

February 21: Tracking 24 Portfolio Signals Across 9 of Our Investing Themes

February 25: Stocks & Markets Podcast: Going Hypersonic With Starfighters Space

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.

YouTube, Apple Podcasts, Spotify

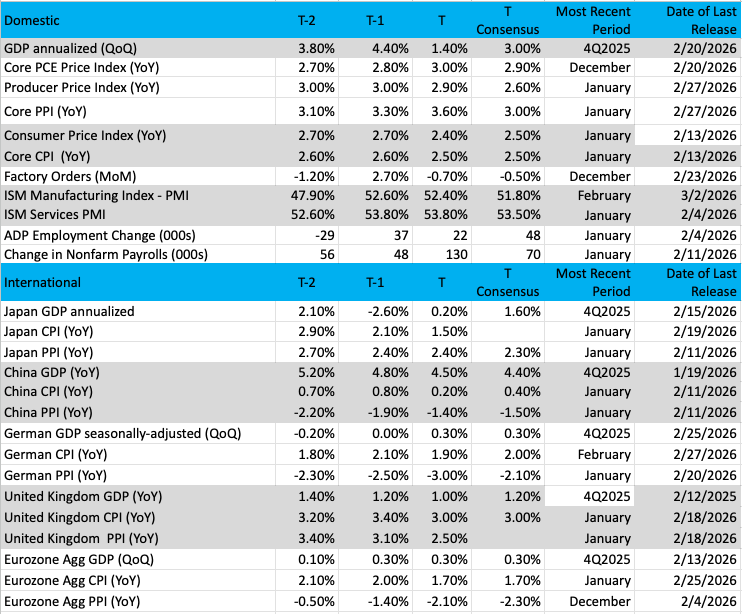

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

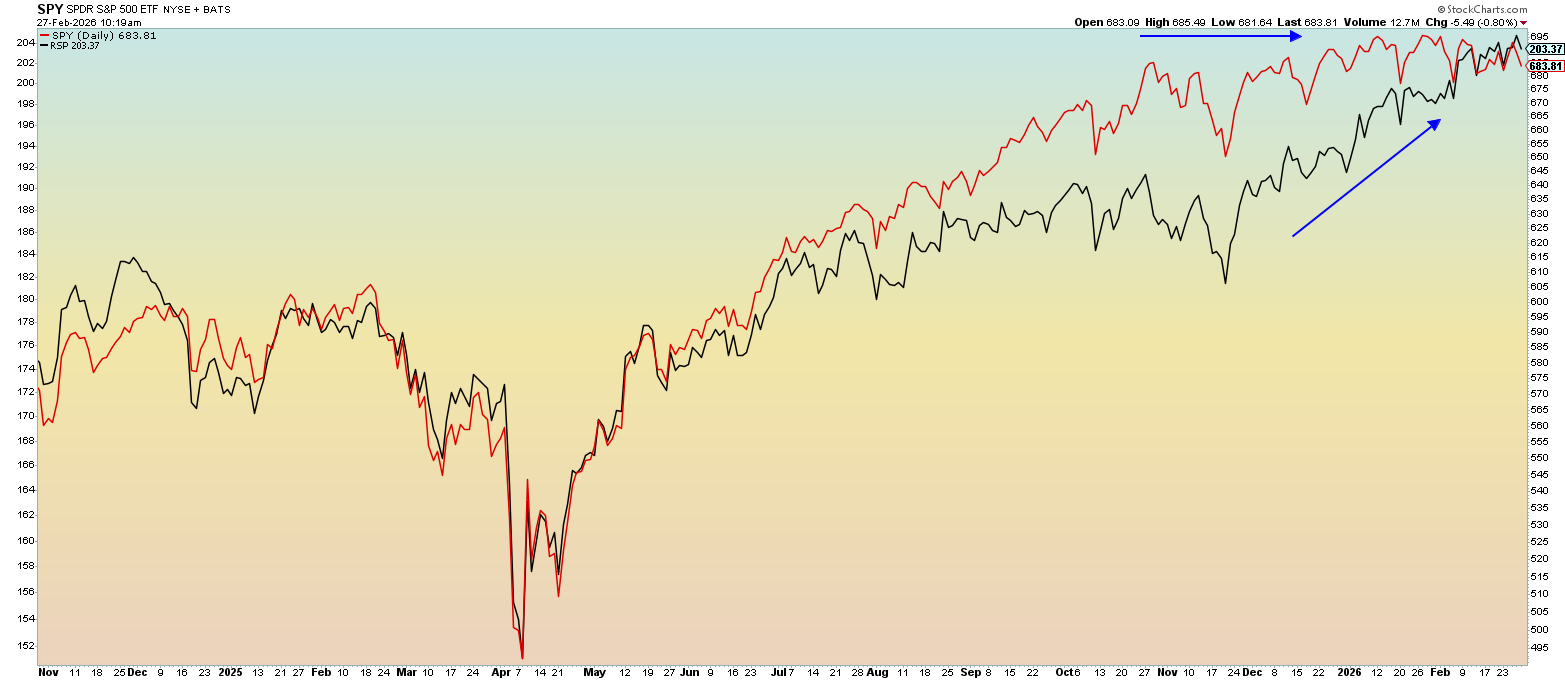

Chart of the Week: S&P 500 – Market Cap vs. Equal Weighted

We’ll take a look at the SPDR S&P 500 ETF (SPY) vs Invesco S&P 500 Equal Weight ETF (RSP) today in our monthly check in on these two important ETFs. As a refresher, the RSP is the equal-weighted S&P 500 index, which means every member of the index just gets "one vote." For example, Nvidia (NVDA) has the same weighting as Coinbase (COIN) , but of course their market capitalizations are vastly different. Contrarily, the SPY is a cap-weighted index that certainly has influence from the top of the list, which includes those mega-cap/trillion-dollar valuation companies.

We like to take a snapshot and compare both the SPY and RSP each month to see where the power lies in the markets. Jus analyzing the SPY, which is the most heavily traded and liquid ETF in the world, doesn't tell the full story. The RSP is a much broader interpretation, and when this ETF is performing better (going up) than SPY we can deduce the market is rallying with broader participation from many groups, not just the top-heavy names. In other words, not just technology, chips, AI-related names.

Our findings over the last couple months tell us the RSP has far outperformed the SPY. We can see this view on the chart, since a major separation last fall the RSP has been playing catch up. Currently, the two are on a similar path, mostly sideways, but seeing the RSP (black line) make up the difference between the two ETFs is impressive.

For 2026, the RSP is up a strong 6% while the SPY is only up about 1%. The arrows show the SPY moving sideways and the RSP moving higher, helped by gains in industrials, metals, energy, discretionary, retail and homebuilders. Technology has done OK, but is not overwhelming. It's a sharp divergence, one that could be very bullish for markets, as we often see when these two ETFs converge and start moving together.

Other charts we shared with you this past week were:

Monday, February 23: S&P 500 - 14 Weeks of Stability as Seasonal Patterns Turn Bearish

Monday, February 23: (AXON) - Axon's 'Day' Has Come

Tuesday, February 24: Equinox Gold (EQX) - My Favorite Diplomat

Wednesday, February 25: Nvidia (NVDA) - Can Nvidia Break Free With 'Game Changer' Report?

Thursday, February 26: TJX (TJX) - TJX Frustrates, But This Price Could Trigger More Buying

The Week Ahead

In the Portfolio video for Friday, February 27, we laid out the key items we’ll be focusing on this week, including the start of February economic data and what it says about the speed of the economy, inflation pressures and job creation. We also discuss what we expect from Apple’s new product announcements this week, what we’ll be listening for during the Morgan Stanley Tech conference, and quarterly results from Broadcom (AVGO) and Marvell (MRVL) . We also have quarterly results from Costco (COST) this week, and while we’ve already received its monthly comp sales figures, which were very impressive, we’ll be focusing on that high-margin membership fee revenue stream, membership renewals, and plans for new warehouse locations.

Here's a closer look at the economic data coming at us this week:

U.S.

Monday, March 2

S&P Global Manufacturing PMI – February (9:45 AM ET)

ISM Manufacturing Index – February (10:00 AM ET)

Tuesday, March 3

RCM/TIPP Economic Optimism Index – March (10:10 AM ET)

Wednesday, March 4

MBA Mortgage Applications Index – Weekly (7:00 AM ET)

ADP Employment Change Report – February (8:15 AM ET)

S&P Global Services PMI Report (Final) – February (9:45 AM ET)

ISM Non-Manufacturing PMI Report – February (10:00 AM ET)

EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Fed Beige Book (2 PM ET)

Thursday, March 5

Challenger Job Cuts Report – February (7:30 AM ET)

Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

Imports/Exports – January (8:30 AM ET)

EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, March 6

Employment Report – February (8:30 AM ET)

Used Car Prices – February (9:00 AM ET)

Consumer Credit – January (3 PM ET)

International

Monday, March 2

Japan: S&P Global Manufacturing PMI - February

China: RatingDog Services PMI – February

Eurozone: HCOB Manufacturing PMI – February

UK: Bank of England Consumer Credit – January

UK: S&P Global Manufacturing PMI - February

Tuesday, March 3

Eurozone: Inflation Rate (Flash) - February

Wednesday, March 4

Japan: S&P Global Services PMI (Final) – February

China: NBS Manufacturing & Non-Manufacturing Index – February

China: RatingDog Services PMI – February

Eurozone: HCOB Services PMI (Final) – February

Eurozone: Unemployment Rate, Producer Price Index - January

UK: S&P Global Services PMI (Final) – February

Thursday, March 5

Eurozone: Retail Sales - January

Friday, March 6

Eurozone: GDP, Employment Change – Q4 2025

Germany: New Car Registrations - February

Here's a closer look at the earnings reports coming at us this week:

Monday, March 2

· Open: Norwegian Cruise Line (NCLH), Sealed Air (SEE)

· Close: Credo Technology (CRDI), Lending Tree (TREE), MongoDB (MDB)

Tuesday, March 3

· Open: AutoZone (AZO), Best Buy (BBY)

· Close: Box (BOX), CrowdStrike (CRWV)

Wednesday, March 4

· Open: Abercrombie & Fitch (ANF), Brown-Forman (BF.B), Dycom (DY)

· Close: American Eagle (AEO), Broadcom (AVGO), Okta (OKTA)

Thursday, March 5

· Open: BJ’s Wholesale (BJ), Ciena (CIEN), Kroger (KR), Victoria’s Secret (VSCO)

· Close: Cooper (COO), Costco (COST), Gap (GAP), Marvell (MRVL)

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

· Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

ONES

Amazon AMZN; $210.00; 881 shares; 3.46%; Sector: Consumer Discretionary

UPDATE: After rising more than 3% in January, shares of Amazon (AMZN) tumbled double digits in February, leaving them down more than 10% year to date. The culprit wasn’t Amazon’s December quarter that it reported in early February, but rather three other factors. One is the significant step higher in its capex plan for this year, which will reach $200 billion, $50 billion more than Wall Street was expecting. Second, as it continues to invest in AWS and other areas, management guided operating income for the current quarter of $16.5 billion to $21.5 billion, which is below the $22.2 billion market consensus. That, in particular, as well as the lofty capex spending, triggered multiple price target cuts for AMZN shares shortly after. Even as we joined that effort, dialing back our target to $275 from $310, we pointed out what will be key for Amazon is for it to convert the AWS capacity it is adding into not only revenue but also delivering better margins over time. In recent quarters, we’ve seen that Amazon is adept at doing that with digital shopping and AWS, but it didn’t go unnoticed by us that AWS’s 2025 operating margin dipped to 35.4% from about 37% in 2024 at a time when, per CEO Andy Jassy, AWS added more data center capacity than any other company in the world. Similar to Microsoft and Azure, and other “show me” stories these days, the market will want to see margins at AWS rebound as the bulk of the oncoming spending is digested. Based on what we’re seeing in AI adoption and usage, we can be patient. Meanwhile, recent signals have pointed to consumers not only pivoting more to digital shopping, but also increasingly to grocery, an area of focus for Amazon. It drives not only more repeat visits but also potentially greater attach rates for other items. And we see Amazon’s effort to expand same-day and next-day delivery narrowing the gap even further between reasons to shop online versus in person. And as we’ve pointed out, lending a helping hand is the growing advertising business, which grew 22% year over year in the December quarter to $21 billion. In 2025, that high-margin advertising business generated more than $68 billion in revenue, and we see more ahead as Amazon continues to focus on that effort. Outside of the company’s core businesses, per recent 13F-HR filings, Amazon holds a stake of 158.36 million shares in Rivian, 225,428 shares in Marvell, as well as positions in other companies. In mid-December, Amazon was reportedly in talks with OpenAI for an investment, a move that would likely include OpenAI using AWS and Amazon’s Trainium chips, a positive for our Marvell and Broadcom shares. We will be following that closely, given reports that OpenAI is pursuing a Q4 2026 IPO. We’ll also monitor developments for Amazon’s autonomous vehicle effort, known as Zoox.

February Price Change: -12.2%; Yield: 0.00%

INVESTMENT THESIS: We believe that upside will result from Amazon's continued e-commerce dominance, AWS's continued leadership in the public cloud space, and the ongoing growth of the company's advertising revenue stream, which feeds off Amazon's e-commerce business. Additionally, we think profitability will continue to improve as AWS and advertising account for a larger portion of total sales, as both these segments sport higher margins than the eCommerce operation. While we believe the increasing share of the revenue from these higher-margin businesses will be key to driving profitability longer-term, we think margins on eCommerce stand to improve as the company's infrastructure is further built out and economies of scale further kick in. The embedded call option is that management is always looking to enter a new space and generate new revenue streams.

Target Price: Reiterate $275; Rating: One

Panic Point: $200

RISKS: High valuation exposes the stock to volatile swings, e-commerce has exposure to slower consumer spending and competition, potential headwinds resulting from new e-commerce regulation in India, and management is not scared to invest aggressively for growth, which can at times cause volatile reactions as near-term concerns arise relating to the impact on margins.

Arista Networks ANET; $133.50; 1,325 shares; 3.31%; Sector: Technology

UPDATE: Following a more than 8% rise in January, shares of Arista Networks (ANET) gave some of that back in February, leaving them up just under 2% for the first two months of the year. While you might think that move lower came after the company’s Q4 2025 earnings report, we’d refer you to our note analyzing those results, the same one in which we reiterated our $180 price target. Remember, our thinking has been that rising spending on AI and data center buildouts and increasing data traffic from AI, streaming, and other connected devices would drive demand for Arista. The company’s ~29% year-over-year revenue increase in Q4 2025 speaks to that, and so does the ~8% sequential one. To that, we add the jump in Arista’s total deferred revenue to $5.4 billion exiting 2025 from $4.7 billion at the end of September. As impressive as that 15% increase is, however, keep in mind we should see total deferred revenue move higher as the significant step up in hyperscaler capital spending for 2026 happens. One of the bigger increases was at Meta, which is a key customer for Arista, as is Microsoft. Spending also remains strong across Arista’s other customer sectors, which include Enterprise and Financials (32% of revenue) and AI and Specialty providers (20% of revenue, including Apple, Oracle (ORCL), and other neoclouds). That led the Arista management team to suggest we could see one or two more 10% customers in 2026. Despite those positive developments, which fueled a post earnings rebound near $145, ANET shares gave that move back following news that existing Nvidia customer Meta agreed to a multiyear deal to use its chips. The concern for Arista is Nvidia may encroach on its relationship with Meta but given such pronounced capital spending levels for AI and data center, we see ample room for Arista to grow its revenue. A late February tie up between Meta and AMD, and the comment from Meta’s head of infrastructure, Santosh Janardhan, solidified that view for us. With support at the 200-day moving average, we look forward to Arista’s presentation at the Morgan Stanley Tech Conference on March 3. We’ll be paying close attention to comments about order and deferred revenue activity and reaffirming comments are a potential catalyst for us to get even more involved in the shares.

February Price Change: -5.9%; Yield: 0.00%

INVESTMENT THESIS: Arista Networks engages in the development, marketing, and sale of data-driven, client-to-cloud networking solutions for AI, data center, campus, and routing environments in the Americas, Europe, the Middle East, Africa, and the Asia-Pacific. Its cloud networking solutions consist of Extensible Operating System (EOS), a publish-subscribe state-sharing networking operating system offered in combination with a set of network applications. The company offers data center, cloud, and AI networking, cognitive adjacencies, and cognitive network software and services. It also provides post-contract customer support services, such as technical support, hardware repair, and replacement parts beyond standard warranty, bug fixes, patches, and upgrade services. The company serves a range of industries comprising internet companies, cloud service providers, financial services organizations, government agencies, media and entertainment, healthcare, oil and gas, education, manufacturing, industrial, and others. Two of Arista’s largest customers in the last few years are two Portfolio holdings you’ll quickly recognize — Microsoft and Meta. Per Arista’s 10-K filings, both Meta and Microsoft each account for more than 10% of revenue. Other named customers include Amazon’s AWS, Google Cloud, Anthropic, Canva, SAP, Shopify, Apple, Oracle, Bank of America, and Accenture.

Target Price: $180; Rating: One

Panic Point: $110

RISKS: Economic, customer, supply chain, and competition risks.

Axon Enterprise AXON; $542.40; 395 shares; 4.01%; Sector: Aerospace & Defense

UPDATE: Following the harsh slide in the second half of January, shares of Axon (AXON) traded sideways until the company reported blowout December-quarter results. The company's future contracted bookings stood at $14.4 billion exiting 2025, up from $11.4 billion at the end of the September quarter and $10.1 billion at the end of 2024. To be fair, given the timing of the government shutdown, Axon’s December-ending quarter bookings surged more than 50%, but that likely represents some catch-up spending. Bookings outside of U.S. state and local law enforcement surpassed the $2 billion mark with more than $1 billion coming from markets outside the U.S. All in all, we would say the bookings and related figures put up by Axon should put to rest concerns over shifting market shares and AI headwinds that weight on AXON shares since late January. Those same bookings give ample coverage for Axon’s 2026 top-line guidance of $3.53 billion-$3.61 billion, up around 28% at the midpoint and nicely ahead of the $3.44 billion market consensus. While we reduced our Axon target to $700 from $800 to account for slower margin gains as the company continues to invest in new products, tariffs and higher component costs are be a bit of a headwind. While Axon may once again be conservative with its guidance, as margins rebound, and the mix shift toward software and services accelerates, due in part of further AI adoption, we can revisit our target price as needed. Following the post-earnings surge, one that popped our position in AXON shares past a 4.5% position size, we trimmed our position for a more-than-respectable gain on February 26. Subsequent to that move, AXON shares traded off but still managed to soar 25% higher in the final week of February, leaving them up double-digits for the month. That places the shares just above the 50-day moving average near $539, and we will look to see if that becomes new level of support. Upcoming catalysts include Axon management presenting at the Morgan Stanely Technology Conference on March 3 and the Bank of America Global Industrials Conference on March 19. We’ll also continue to monitor signals for body camera and AI adoption in the public safety sector.

February Price Change: 12.2%; Yield: 0.00%

INVESTMENT THESIS: Axon Enterprise develops, manufactures, and sells conducted energy devices and cloud-based digital evidence management software designed for use by law enforcement, corrections, military forces, private security personnel, and private individuals for personal defense. The company operates in two segments: Taser (recently renamed Connected Devices) and Software & Sensors (recently renamed Software & Services). Taser develops and sells CEDs used for protecting users and virtual reality training. Software & Sensors manufactures fully integrated hardware and cloud-based software solutions such as body cameras, automated license plate reading, and digital evidence management systems. Axon delivers its products worldwide and gets most of its revenue from the United States. According to Mordor Intelligence, the wearable and body-worn cameras market on its own was valued at $1.62 billion in 2020 and is expected to reach $424.63 billion by 2026. Public safety organizations are increasingly adopting cloud solutions, leading to significant spending in this area. The digital spending in public safety is projected to reach $201 billion by 2027.

Target Price: Reiterate $700; Rating: One

Panic Point: $400

RISKS: Manufacturing and supply chain, competitive factors, government regulation, and technology change.

First Trust Nasdaq Cybersecurity ETF CIBR; $62.91; 2,730 shares; 3.21%; Sector: Cybersecurity

UPDATE: After a decline in January in concert with a larger move lower in tech and software stocks, the ETF's drop continued in February as (CIBR) constituents, like Palo Alto Networks (PANW) and CrowdStrike (CRWD) were under pressure amid concerns over potential AI disruption. This despite prospects for cybersecurity spending to remain on an upward climb in the coming quarters. As we saw during Anthropic’s February 24 Enterprise Agents livestream, it is working with software and other companies to improve their tools and services. In terms of cybersecurity, Anthropic partnered with CIBR constituent Infosys (INFY) to deliver enterprise AI solutions across telecommunications, financial services, manufacturing, and software development. We should see similar announcements as Anthropic works with other cybersecurity companies to leverage AI into more robust cybersecurity offerings. Cybersecurity Ventures predicts that global spending on cybersecurity products and services will exceed $520 billion annually by 2026, up from $260 billion in 2021. Also like us, Cybersecurity Ventures sees cybersecurity and cybercrime prevention as a growth industry. The research firm sees the imperative to protect increasingly digitized businesses, governments, schools, Internet of Things devices, and industrial control systems (ICS), as well as semiconductors, medical devices, gaming systems, cars, ships, planes, drones, trains, ATMs, and consumers from cybercrime propelling global spending on cybersecurity products and services to $1 trillion annually by 2031. That double-digit compound annual growth rate keeps us bullish on cybersecurity spending and the diverse exposure captured by owning CIBR shares. Like our January comments for enterprise software companies, we see the move lower in CIBR shares as an overreaction to AI related fears. That also means cybersecurity companies will need to deliver continued growth in key metrics, like RPOs and backlogs. The next set of known catalysts for CIBR shares will be quarterly results from CrowdStrike and Broadcom (AVGO) on March 3 and 4, respectively.

February Price Change: -8.9%; Yield: 0.48%

INVESTMENT THESIS: The First Trust Nasdaq Cybersecurity ETF seeks investment results that correspond generally to the price and yield (before the fund's fees and expenses) of an equity index called the Nasdaq CTA Cybersecurity Index. The Nasdaq CTA Cybersecurity Index is designed to track the performance of companies engaged in the cybersecurity segment of the technology and industrial sectors. It includes companies primarily involved in the building, implementation, and management of security protocols applied to private and public networks, computers, and mobile devices to protect the integrity of data and network operations. To be included in the index, a security must be listed on an index-eligible global stock exchange and classified as a cybersecurity company as determined by the Consumer Technology Association. Each security must have a worldwide market capitalization of $250 million, have a minimum three-month average daily dollar trading volume of $1 million, and have a minimum free float of 20%.

Target Price: Reiterate $85; Rating: One

Panic Point: $68

RISKS: Cybersecurity spending, technology and product development, the timing of the product sales cycle, new products, and services in response to rapid technological changes and market developments, as well as evolving security threats.

Costco Wholesale COST; $1,010.79; 215 shares; 4.07%; Sector: Consumer Staples

UPDATE: Shares of Costco (COST) put in another good month for the Portfolio, building on their January gains to close February just over 17% higher quarter to date. We can trace the continued climb to three distinct events in February. First, strong January comp sales that were made all the more impressive when one realizes the very difficult comparisons they lapped. Second, between the January PMI and Flash February PMI reports, and other inflation data showing those pressures trekked higher in recent months, we continue to see signs consumers are looking for ways to stretch the disposable income dollars. For its January quarter, Walmart reported U.S. comp sales of 4.6%, less than the average adjusted comp sales figure of 6.3% posted by Costco over the November 2025 -January 2026 period. There are multiple questions about the repaying of collected tariffs, and we will look to see how that plays out and the degree to which Costco may benefit. However, renewed tariff uncertainty and Trump stepping up global tariffs to 15% from 10% could keep inflation tailwinds blowing, a tailwind for Costco’s business and our shares. Subject to what we learn when Costco reports its quarterly results on March 5, we’ll revisit our current $1,100 price target as needed. During that earnings call, we’ll keep our ears open for any comments about a potential special dividend later this year.

February Price Change: 7.5%; Yield: 0.51%

INVESTMENT THESIS: We like Costco's long-term prospects, driven by a club-based operating model that focuses on volumes, not margins, and therefore offers its customers a value proposition of everyday low prices. The strength of this model has created an incredibly loyal customer base with low churn and continued share gains in both brick-and-mortar and e-commerce. This is a global concept, evidenced by the strength of sales both in the U.S. and abroad, which includes an emerging China opportunity. We see the company's membership model as a key differentiator versus other retailers, and its plans to open additional warehouse locations in the coming quarters should drive retail volumes and the higher-margin membership fee income as well. We also appreciate management's approach to capital returns and their willingness to return cash.

Target Price: Reiterate $1,100; Rating: One

Panic Point: $825

RISKS: Inability to pass through higher costs, fuel prices, weaker consumer, and membership churn.

Dutch Bros BROS; $53.61; 3,678 shares; 3.69%; Sector: Consumer Cyclical

UPDATE: While shares of Dutch Bros (BROS) rallied back hard at the end of February, they still closed the month down just over 1%, keeping them a drag on the Portfolio’s year-to-date performance. Revenue for Dutch’s Q4 soared more than 29% year over year to $443.61 million, easily clearing the $424.8 million consensus. That figure benefited from the one-two punch of impressive comp sales and the 5.4% increase in transaction growth, but we also have to factor in the greater shop count year over year as well. Entering Q4 2025, Dutch had 1,081 open locations, almost 14% higher year over year, and it ended the quarter with 1,136 open shops vs. 982 exiting 2024. Parsing those figures, we see the pace of new locations accelerated, and we continue to see more of that ahead for Dutch to hit its 2,029-shop count goal by 2029. For the coming year, Dutch expects to open at least 181 new shops, including the 20 recently acquired from Clutch Coffee Bar, a move that brings Dutch to the Carolinas. We would not be surprised to see similar moves in the coming quarters, as it would help break into new states, but also leapfrog its shop count efforts. Assuming Dutch delivers 181 new locations this year, it would need to average 237 in 2027, 2028, and 2029 to hit its 2029 goal. That resonates with a key reason why we added BROS shares to the Portfolio. During the earnings call, Dutch management shared that based on historical inventory turns, sustained changes in coffee prices tend to show up two or three quarters later in its income statement. While that means higher coffee prices will remain a headwind in the first half of 2026, if the recent drop is sustained, it could become a tailwind in the second half of 2026, when combined with 2025 and 2026 pricing action taken by Dutch. As we monitor the coffee market, we’ll do the same on dairy and sugar, which are also key inputs for Dutch’s coffee and energy drinks. Sustained year-over-year improvement in coffee, dairy, and sugar prices could lead to Dutch’s profit guidance being conservative, especially in the second half of 2026. Given the flow-through timing discussed above, should we see that unfold, it would be a reason for us to revisit our BROS price target. Near-term, BROS shares could be restrained by questions over consumer spending and job creation, but so long as it continues to put up significant comp sales figures, we’re inclined to be patient, especially as it begins rolling out its updated food menu across its entire footprint.

February Price Change: -1.3%; Yield: 0.00%

INVESTMENT THESIS: Dutch Bros is an operator and franchisor of drive-thru shops that focus on serving high-quality, hand-crafted beverages with unparalleled speed and superior service. Coffee-based beverages make up about 50% of the menu mix, and about 25% of the menu mix is based on the company’s proprietary Blue Rebel energy drink, which is highly customizable with flavors and modifiers and can be served blended or over ice. The energy platform helps unlock the afternoon day part and broadens the company’s appeal. The remaining 25% of the menu mix is a wide variety of teas, lemonades, sodas, and smoothies. The company’s west-to-east expansion is a time-tested strategy that should drive revenue and EPS growth over the next several years. Leveraging that footprint expansion and low-single-digit comp sales growth, management reiterated its long-term guidance of around 20% annual revenue growth. Helping support that guidance, the company confirmed it will introduce an expanded food menu in 2026. Dutch Bros is slated to enter the consumer-packaged goods (CPG) space in a deal with Trilliant Food & Nutrition.

Target Price: Reiterate $75; Rating: One

Panic Point: $52

RISKS: Commodity risks, labor costs, interest rate risk, and inflation.

Marvell Technology MRVL; $81.69; 2,145 shares; 3.28%; Sector: Technology

UPDATE: After declining in the mid-single digits in January, shares of Marvell Technology (MRVL) rallied back in February, rising more than 3% as multiple data points confirmed the robust outlook for AI and data center ships. That includes capacity constraints that are fostering adoption of custom AI and data center chips from Marvell customers like Google, Amazon, and others. Meanwhile, as we suspected would be the case, rising AI adoption and usage, and other forms of data creation and consumption, are fueling a pickup in enterprise and carrier infrastructure spending. The most recent confirmation point was Dell’s AI server guidance for the coming year. Outlooks like that keep us bullish on Marvell’s business and our shares. When the company reports its quarterly results on March 5, we’ll be revisiting its previously shared guidance for fiscal 2027, which ends in January 2027. That initial guidance calls for Data Center segment revenue to grow by more than 25% and the Communications & Other revenue to be up 10%. Some back-of-the-napkin math implies around $10 billion in revenue during fiscal 2027, compared to the $5.8 billion delivered in fiscal 2025. Fueling that expected increase is the quickly growing interconnect business, which should grow faster than overall cloud capital spending next year, and the continued ramp in Marvell’s custom AI silicon business, which on its own should be up ~20% in fiscal 2027. Marvell signaled that, based on its program wins, it already sees its Data Center revenue growth accelerating above fiscal 2027’s 25% growth target. For a company that typically guides one quarter at a time, Marvell is shared far more than usual, an indication that suggests its program visibility has improved. In late 2025, Marvell announced its acquisition of Celestial AI, the creator of Photonic Fabric, an optical interconnect technology platform for AI computing systems that is expected to accelerate Marvell’s connectivity strategy for next-generation AI and cloud data centers. Based on Celestial's current customer line-up and program wins, Marvell said it sees meaningful revenue contributions from Celestial AI beginning in the second half of fiscal 2028, reaching a $500 million annualized run rate in the fourth quarter of fiscal 2028, doubling to a $1 billion run rate by the fourth quarter of fiscal 2029. Over the last several weeks, MRVL shares have been rangebound between their 50-day and 200-day moving averages. In addition to Marvell’s earnings this week, other know catalyst for the stock include quarterly results from Broadcom as well as Morgan Stanley’s Technology conference. We’ll also be on the lookout for February revenue reports from Taiwan Semiconductor and Foxconn.

February Price Change: 3.5%; Yield: 0.29%

INVESTMENT THESIS: Marvell is a fabless supplier of high-performance standard and semi-custom infrastructure semiconductor solutions. These solutions power the data economy, enabling the data center, carrier infrastructure, enterprise networking, consumer, and automotive/industrial end markets. With roughly 75% to 80% of Marvell's revenue stream tied to digital infrastructure, we see it continuing to benefit from rising content consumption and creation. Pointing to that rising demand that necessitates network densification and the build of digital infrastructure, Ericsson sees global monthly average usage per smartphone reach 46 gigabytes (GB) by the end of 2028, versus 19 GB in 2023 and 15 GB in 2022.

Target Price: Reiterate $140; Rating: One

Panic Point: $75

RISKS: Technology risk, customer risk, competition risk, reliance on manufacturing partners, and supply chain constraints.

Meta Platforms META; $648.18; 337 shares; 4.08%; Sector: Communication Services

UPDATE: After a wild swing in January that ended with Meta (META) rising more than 8%, the shares gave that back and more during February. During February, Meta announced multi-year deals with Google, Nvidia and AMD to secure chip capacity similar to the one it announced with Corning in January. We see those moves as Meta ensuring it has sufficient capacity to execute its capital spending plans for this year and beyond. While that effort will continue to influence the market’s perception of Meta, we’ll continue to focus on the business — and Meta’s emphasis on serving more ads and using AI to do so. During the December quarter, we saw the company’s family's average revenue per person (ARPP) jump 14.5% quarter over quarter to $16.56. Given seasonality factors in the December quarter, the year-over-year jump from $14.25 is even more impressive when we account for the 2024 presidential election. While Meta did not share revenue guidance for the full year, trends in the ARPP should translate into meaningful revenue growth in the coming quarters. 2026 will also be a full year of greater monetization on Threads and WhatsApp, and we have to wonder how long until Meta implements video on Threads, a move that, based on what we’re seeing with Instagram and Facebook, should drive even greater engagement and monetization. During the December quarter, Meta showed clear results of leveraging AI in its business, but it is also demonstrating how that effort is driving average revenue per person and operating cash flow higher, even as the company’s AI-related investments jump higher in 2026. We will remain sizable owners of META shares as upcoming investments aim to spin the advertising flywheel faster while the increasingly AI-laced ad business drives interaction and monetization higher. The next known catalyst for META shares will be the company’s presentation at the Morgan Stanley Tech conference on March 4.

February Price Change: -9.5%; Yield: 0.32%

INVESTMENT THESIS: Meta segments its business between Family of App Products, which includes Facebook, Instagram, Messenger, Threads, and WhatsApp, and Reality Labs Products, which includes its metaverse and investments and future product R&D. Family of Apps accounts for about 99% of the company's revenue and 100% of the company's operating profits. Substantially all of Meta’s revenue is currently generated from advertising on Facebook and Instagram. Family daily active people (DAP) were ~3.6 billion on average for the December 2025 quarter. Meta expects to spend $162 billion-$169 billion on capex in 2026, a significant increase year over year, with most of this spending focused on AI infrastructure and initiatives. Meta is positioned to benefit from the ongoing shift toward digital advertising and the adoption of AI across its entire product offering. We recognize Meta is ramping up capital spending as part of the current AI arms race, but we see that as an investment that should drive productivity in its core advertising business. As the company harvests that investment, we could see a step up in margins, much like we saw in 2023.

Target Price: $850; Rating: One

Panic Point: $560

RISKS: Ability to add and retain users and user engagement; marketing spend; new products or changes to existing ones; competitive risk, geopolitical risk.

Nvidia Corp. NVDA; $177.19; 970 shares; 3.21%; Sector: Technology

UPDATE: Shares of Nvidia (NVDA) slumped in late February following the company’s January-quarter earnings release, leading to a decline of more than 7% for the month, a move that erased their January gain. January-quarter results handily beat expectations and guidance pointed to accelerating AI and data center growth ahead. The culprit? Whisper guidance expectations that called for current quarter revenue to be as high at $80 billion. For the current quarter, Nvidia guided its top line to $76.44 billion-$79.56 billion, considerably ahead of the expected $72.93 billion, and implying year-over-year gains of more than 70% as well as another sequential step up. Given the mix of revenue that skews more than heavily toward AI and data center, it’s fair to assume that will be the big driver of the top line. That meshes with the upsized hyperscaler capex figures for this year and coming ones, as well as recent Nvidia wins, including one with Meta. Tracking the progress on that revenue guidance means we must continue to pay attention to monthly revenue figures and earnings from Taiwan Semiconductor, Foxconn, HP Enterprise, Dell, Super Micro Computer, and others. While we have ample room to maintain our One rating given our $250 price target. Others on Wall Street are lifting their targets from somewhere near our target to $275-$300, but let’s first see if NVDA holds support at the $185-$186 level before making any near-term buying decisions. We'd also note NVDA shares broke through support levels between $185-$186 and the next layer of support shows up near $175 or the 200-day moving average. With CEO Jensen Huang participating in a fireside chat at the Morgan Stanley TMT Conference on March 4, giving a keynote at GTC on March 16, and monthly revenue reports from TSM and Foxconn in between those two events, we’ll have ample time and data we can use to revisit the shares and our NVDA price target.

February Price Change: -7.3%; Yield: 0.02%

INVESTMENT THESIS: Nvidia is well-positioned to benefit from ramping AI and data center spending. The company pioneered accelerated computing to help solve the most challenging computational problems. Nvidia is now a full-stack computing infrastructure company with data-center-scale offerings that are reshaping the industry. The company's full stack includes the foundational CUDA programming model that runs on all Nvidia GPUs, as well as hundreds of domain-specific software libraries, software development kits, or SDKs, and Application Programming Interfaces, or APIs. This deep and broad software stack accelerates the performance and eases the deployment of Nvidia accelerated computing for computationally intensive workloads such as artificial intelligence, model training and inference, data analytics, scientific computing, and 3D graphics, with vertical-specific optimizations to address industries ranging from healthcare and telecom to automotive and manufacturing. Nvidia reports in two business segments: Compute & Networking and Graphics. The Compute & Networking segment (78% of revenue, 85% of operating income) is comprised of Data Center accelerated computing platforms and end-to-end networking platforms, including Quantum for InfiniBand and Spectrum for Ethernet; NVIDIA DRIVE automated-driving platform and automotive development agreements; Jetson robotics and other embedded platforms; Nvidia AI Enterprise and other software; and DGX Cloud software and services. The Graphics segment (22% of revenue, 15% of operating income) includes GeForce GPUs for gaming and PCs, the GeForce NOW game streaming service and related infrastructure; Quadro/NVIDIA RTX GPUs for enterprise workstation graphics; virtual GPU, or vGPU, software for cloud-based visual and virtual computing; automotive platforms for infotainment systems; and Omniverse Enterprise software for building and operating metaverse and 3D internet applications.

Target Price: $250; Rating One

Panic Point: $160

RISKS: Market and interest rate risk, credit risk, country risk, and operational risk, including cybersecurity.

Palantir Technologies PLTR; $137.19; 1,265 shares; 3.25%; Sector: Financial Services

UPDATE: Following the pounding they took in January, like many other software names, shares of Palantir (PLTR) moved lower in early February. PLTR shares vacillated between $126-$137 for the balance of the month, closing out at $137.19. That translates into a combined decline of more than 22% for the first two months of 2026. We view that as AI-worried investors ignoring the huge strides the company made during the December quarter with its U.S commercial revenue up 137% year over year and 28% sequentially, while its U.S. commercial total contract value (TCV) closed the quarter at $1.34 billion, up 67% year over year. Overall, TCV hit $4.26 billion, up 138% year over year. Subsequent to that quarterly earnings report, Palantir announced expanded relationships with Airbus and the Defense Information Systems Agency. That was followed with a partnership announcement between Palantir and Rackspace that will see Palantir’s software used in Rackspace’s Private Cloud and UK Sovereign data centers. The agreement will also extend Palantir’s reach into the enterprise community, leveraging Rackspace’s positioning when it comes to managing mission-critical enterprise workloads. Following that string of events, we picked up more shares for the Portfolio on February 18. We continue to see Palantir very well positioned to benefit from AI adoption and usage in the commercial and government sector, and view its pullback in the first two months of 2026 as an overreaction. As the company continues to announce new and expanded relationships, and grow its TCV, we’ll patiently wait for the market to realize the current opportunity in PLTR shares. Already UBS, Mizuho, and Freedom Capital have upgraded the shares.

February Price Change: -6.4%; Yield: 0.00%

INVESTMENT THESIS: Palantir Technologies specializes in big data analytics and builds software platforms that help organizations integrate, analyze, and make sense of vast amounts of data for both commercial and government clients. While much has been made about the company’s exposure to the federal government, its software is used across 90 industries, and the larger global government sector accounted for 55% of revenue last year. The balance was from the commercial sector. Exiting 2025, Palantir's U.S. Commercial remaining deal value (RDV) stood at $4.38 billion, up 145% year over year, and its Total Contract Value (TCV) stood at $10.8 billion, up 128% year over year. We will continue to monitor Palantir’s RDV and deferred revenue metrics. Key items to watch include continued diversification of its customer base across industries and increasing revenue per customer. Because we are still in the relatively early innings of AI adoption, we are inclined to be long-term owners of PLTR shares.

Target Price: $220; Rating: One

Panic Point: $125

RISKS: Economic and IT budget spending risk, technology risk, competition and competitive pressures, and customer acquisition risk.

ServiceNow NOW; $108.01; 1,435 shares; 2.90%; Sector: Technology

UPDATE: After getting pummeled along with other enterprise software stocks in January, shares of ServiceNow (NOW) and others in that category continued to trade off in early February. The shares found a bottom near $100 and bounced back and forth between that and the $110 level for the remainder of the month, leaving them down another 7.6% in February. The combined drop during January and February was more than 29%, more than a classic correction and one that suggests the drop is overdone. Adding to our thinking that that is the case, during Anthropic’s February 24 presentation, it discussed how it is working with enterprise software companies to build better tools to serve enterprise customers. This should help quell concerns about AI disruption, and let’s remember that ServiceNow has partnerships with Anthropic as well as OpenAI. Despite those AI disruption concerns, we saw Salesforce report sizable gains in its Agentforce annual recurring revenue and a more than 21% jump for its RPOs exiting January. Those figures add to the thinking that “SaaS-pocalypse” is likely overblown. Mid-February, many top executives at ServiceNow cancelled regularly scheduled stock sales via 10b5-1 plans, and CEO Bill McDermott shared plans to commit $3 million to buy NOW stock on February 27 at “prevailing market prices.” We fully suspect ServiceNow is leaning heavily into its $9.5 billion share repurchase plan. While we see those as nice moves, we continue to think an upbeat ServiceNow management presentation at an upcoming investor conference, quarterly update, or similar announcements would have a greater impact on investor sentiment and NOW shares. Based on the “revelation” shared by Anthropic, we will be patient with NOW and look to collect fresh data points as the March wave of investor conferences unfold. Our focus will be on what is said about AI adoption and usage across customers as we also look to see if RPOs, backlog levels, or total contract value figures rise on a quarter-over-quarter basis. If that is what we see, it will be those figures that help stoke investor appetite for select software stocks, including NOW shares.

February Price Change: -7.6%; Yield: 0.00%

INVESTMENT THESIS: The addition of ServiceNow adds exposure to the enterprise as it deploys AI-enabled solutions across its enterprise workflow platform. The company’s “Now Platform” is a cloud-based solution with embedded AI and machine learning (ML) capabilities that help unify and digitize workflows, driving productivity. At the heart of it, the company’s platform automates workflows across an entire enterprise by connecting disparate departments, systems, and silos in a seamless way to unlock productivity. ServiceNow counts more than 8,100 global customers, including 85% of the Fortune 500, with 97% of its revenue from subscriptions that have notched a 98% renewal rate. During the March 2025 quarter, ServiceNow also announced plans to acquire Moveworks, which offers front-end AI assistant and enterprise search technology, and Logik.ai, which provides AI-powered, and composable configure, price, and quote solutions for sales teams. We see these moves augmenting its offering and helping pave the way for further adoption of AI and subscription-based revenue.

Target Price: Reiterate $185; Rating: One

Panic Point: $118

RISKS: Industry and economic risk, competition and competitive pressures, and acquisition risk.

SuRo Capital SSSS; $9.38; 23,825 shares; 4.18%; Sector: Financial Services

UPDATE: Share of SuRo Capital (SSSS) closed February off its highs for the month, delivering a modest gain for the Portfolio. Fluctuations in SSSS’s share price during the month can be traced to a combination of rising market uncertainty but also questions over Open AI’s revenue and cash-burn prospects. On February 27, The ChatGPT-maker closed a $100 billion funding round that valued the company at $830 billion, with backing from tech giants Amazon, Nvidia, SoftBank, and Microsoft. That updated valuation should drive a meaningful upward revision to SuRo’s net asset value, which when last updated, reflected OpenAI’s Q3 2025 valuation near $300 million. As we discussed when SuRo shared its initial Q4 2025 portfolio update, SuRo exited December with a meaningful position in CoreWeave (CRWV) shares, but it also monetized more of that position during the December quarter. That move should fuel the company’s next dividend payment, but we also suspect the SuRo management team continued to unwind the position in CRWV, using their January rebound to do so. That should provide SuRo with additional dividend paying firepower for the coming quarters. While SuRo is closely associated with OpenAI and CoreWeave, let’s remember there are 33 other investments in its portfolio, with sizable ones in Whoop, Blink Health, as well as in Canva, Vast Data, and Plaid. Whoop CEO Will Ahmed has said that company could go public this year or next. Market expectations are that Canva will go public this year, and Plaid late this year or in 2027. When SuRo reports its December-quarter results in March, we will look to learn more about its TensorWave investment. Based on the updated NAV per share, we’ll revisit our price target as needed. We will also keep our eyes peeled for the next dividend announcement.

February Price Change: 0.4%; Yield: 5.33%

INVESTMENT THESIS: SuRo Capital is a business development company (BDC) that invests in high-growth, venture-backed private companies. As SuRo monetizes those portfolio investments through either IPO or M&A transactions, it must pay out most of its earnings to shareholders in the form of dividends. What’s important to factor into our thinking is that SuRo’s strategy isn’t to hold public company investments but rather to monetize them following the lock-up expiration. Sometimes this can be immediate, and sometimes it can be in stages, but when that monetization occurs, it triggers dividend payments. And because a BDC must pay out at least 90% of its taxable income through dividends to shareholders, there is the possibility of a special dividend to hit that qualifying threshold late in the year. As we think about this, it means that we should focus on total return with SSSS, which is defined as capital gains in the shares plus dividends received while owning them. What this means is even if we see SSSS shares trade sideways or move lower, depending on the size of the dividend payments in the coming quarters, the position’s total return could still be sizable for the Pro Portfolio. SuRo's portfolio holdings at the end of June included CoreWeave, ServiceTitan, OpenAI, Liquid Death, Whoop, and fintech company Plaid, as well as roughly 30 other holdings.

Target Price: $12; Rating: One

Panic Point: $8.00

RISKS: Industry and economic risk, competition and competitive pressures, and acquisition risk.

Waste Management WM; $240.84; 900 shares; 4.05%; Sector: Industrials

UPDATE: After proactively locking in some sizable gains in Waste Management (WM) at $231.77 on January 28, the shares subsequently traded off to a low of near $220 following WM’s December-quarter earnings report but rallied back to close the first two months of 2026 up more than 9%. Looking past that modest miss relative to consensus expectations, after reading between the lines of that report and digesting the company’s guidance, we reiterated our $255 price target. For us, the core story of inelastic pricing power and leveraging the combination of automation and cost containment at the core Waste business remains in place. WM management is also delivering on growing the "Healthcare Solutions" business, which posted a more than 50% increase in net operating revenue in the most recent quarter compared to year-ago levels. We continue to like the long-term prospects for that business as management continues to pull costs out of it. We could see further improvement in margins and opex leverage at the legacy WM business as management targets a price increase between 5.4%-5.8% for that business. And an average price increase of 3% is also targeted for the Healthcare Solutions business. That suggests we should continue to see robust operating cash flow and free cash flow. But that isn’t much of a surprise, because WM previously announced it would increase its 2026 quarterly dividend per share by 14.5% to $0.945 and restart its share-repurchase program to the tune of $2 billion in 2026. Should WM shares remain near the $240 level on a sustained basis, it would leave less than 10% upside to our current price target. That could lead us to revisit our current One rating on the shares in the coming days.

February Price Change: 8.4%; Yield: 1.57%

INVESTMENT THESIS: Waste Management’s core business is the inelastic waste removal business for residential, enterprise, and other customers. The company has built its footprint through a series of acquisitions and excelled at wringing costs out of them, driving free cash flow, dividends, and funding incremental acquisition activity. While the residential business is sticky, the commercial business should continue to benefit from non-residential construction activity. Margins should continue to inch higher due to disciplined pricing and increasing use of automation. We are in the early days of WM Healthcare Solutions, but we see the business growing as management integrates and cross-sells against its core business and flexes the ability to integrate nip-and-tuck acquisitions as it has at the core waste business. Here, too, we see room to consolidate a fragmented industry, which makes this a natural fit for Waste Management.

Target Price: $255; Rating: One

Panic Point: $190

RISKS: Industry and economic risk, competition and competitive pressures, and acquisition risk.

TWOS

Alphabet GOOGL; $311.76; 677 shares; 3.95%; Sector: Communication Services

UPDATE: Despite besting consensus expectations for its December-quarter earnings report in early February and landing a multi-billion dollar deal with Meta near the end of the month, shares of Alphabet (GOOGL) retreated enough to wipe out their January gains. What we saw in the December quarter mixed with its drivers led us to bump up our GOOGL target to $365 from $350. As we see further growth in margins at Google Cloud, we’ll revisit our target. So, what weighed on GOOGL shares? For some, it is the ginormous increase in capital spending to $175 billion-$185 billion, which was larger than the capital spending of the last three years combined. What is this money being spent on, you ask? Per the management team, it remains concentrated in technical infrastructure, with approximately 60% allocated to servers and 40% to data centers and networking. In our analysis of Google’s earnings, we discussed how it is aiming to benefit from accelerated depreciation associated with the One Big Beautiful Bill, a move that will reduce its taxable income but be a tailwind for cash flow. We also cited caution with the shares and based on the subsequent slump to below $312 from ~$340 heading into its earnings report on February 4. In late February, Google unveiled the latest update to its flagship Gemini artificial intelligence, showcasing Gemini 3.1 Pro. Exiting December, Google had surpassed 740 monthly active users for its Gemini models, a ringing endorsement for our call last year not to rule the company out of the AI race. Anat Ashkenazi, Senior Vice President and Chief Financial Officer of Alphabet, will present at the Morgan Stanley Tech conference on March 3, and what he discusses could give us a reason to become more bullish on the shares.

February Price Change: -7.8%; Yield: 0.27%

INVESTMENT THESIS: We believe that while search and digital ad dominance are what will carry the shares in the near-to mid-term, longer-term, it is the company's artificial intelligence "moat" that will provide for new avenues of growth. Exiting October 2025, Alphabet surpassed 300 million paid subscriptions across Google One and YouTube. AI is what has made the company's search, video, and targeted ad capabilities best-in-class and is the driving force behind the company's success in voice (Google Home) and autonomous driving (Waymo). Furthermore, we believe it is this AI expertise that will also make the company more prevalent in other industries, including healthcare via its subsidiary Verily, as AI and machine learning continue to disrupt operations across industries. As of late 2025, Google's Gemini app had over 650 million monthly active users. Adding to our positive view of the company's future opportunities, we believe that Alphabet's free cash flow generation and solid balance sheet set it apart and are what will allow the company to continue taking chances on far-out, ground-breaking, and potentially world-changing projects, as well as fund capital returns to shareholders. We will continue to monitor advertising spend as well as the competitive landscape for the company’s core Search and Advertising business. Should we see GOOGL shares pull back near the 50-day moving average, near $295, that incremental upside to our price target would give us sufficient reason to revisit our Two rating.

Target Price: Reiterate $365; Rating: Two

Panic Point: $263

RISKS: Regulatory risk (data privacy), competition, and macroeconomic slowdown impacting consumers and therefore ad buyer activity.

American Express AXP; $308.90; 640 shares; 3.70%; Sector: Financial Services

UPDATE: Shares of American Express (AXP) started February moving higher off their January finish, but in late February, they sold off leaving them to finish the month down more than 12%. Part of the pressure is the renewed AI-related concern for jobs that we discussed on February 27. We saw this same result a few days ago, but AXP shares and those for other credit card companies rebounded following Anthropic’s presentation. Our view on AXP shares continues to hinge on the Platinum Card refresh cycle — how that membership-driven business model benefits and the corresponding benefits more than offset the cost of the Platinum card. The AI-related pressure we’ve seen on AXP shares has put them back at levels we saw before Amex announced its Platinum Card refresh on September 18. We saw some improvement in net card fee revenue during the December quarter as the initial phase of that refresh cycle lifted average fee per card and the number of cards in force. Given the different benefits associated with the refresh effort, including monthly digital streaming credits and dining credits, among others, we should see a steady climb in both of those metrics we track closely. Remember: Those fuel Amex’s net card fee revenue, which drives more than 70% of its pre-tax income. Said a different way, AI-related concern over jobs is likely to have a greater impact on the transaction heavy business models at Mastercard and Visa than at Amex. For now, we’ll let the knee jerk market reaction to Block’s news wash over AXP shares and, based on what we see in the February jobs data and on the U.S.-Iran front, we may opt to scoop up some AXP shares. We will also be watching for the company’s upcoming dividend announcement, one that should reflect Amex’s decision to boost that 2026 payment to shareholders by 16% to $0.95 per share per quarter. As the benefits of the Platinum Card refresh come, we could see further dividend increases ahead.

February Price Change: -12.3%; Yield: 1.23%

INVESTMENT THESIS: American Express is a globally integrated, membership-driven payments company, providing customers with access to products, insights, and experiences that enrich lives and build business success. The company has four reportable operating segments: U.S. Consumer Services (USCS), Commercial Services (CS), International Card Services (ICS), and Global Merchant and Network Services (GMNS). American Express targets the premium consumer space by continuing to deliver membership benefits that span our customers’ everyday spending, borrowing, travel, and lifestyle needs, expanding its roster of business partners around the globe, and developing a range of experiences that attract high-spending customers. In 2025, the company’s net card fee revenue accounted for 72% of its pre-tax income, which we see providing a differentiated business model that should continue to grow as Amex wins new card members and drives its average fee per card higher.

Target Price: Reiterate $400; Rating: Two

Panic Point: $315

RISKS: Slowdown in consumer spending, competition, membership growth, merchant acceptance, and lack of new product innovation.

Apple AAPL; $264.18; 825 shares; 4.08%; Sector: Technology

UPDATE: After finishing down more than 4% in January, Apple (AAPL) recovered some of that lost ground in February. Back in December, we discussed all the products Apple was expected to introduce in 2026, but we continue to think Apple delivering the long-awaited, revamped, AI-enabled Siri powered by Google is the next major catalyst for the shares. Our thinking continues to be that for Apple to accelerate the iPhone upgrade cycle, it will need to delight consumers with that upgraded experience. Mid-February, we learned of yet another setback for this upgrade. Our preference is for Apple to iron out the kinks before introducing the revamped AI-enabled Siri lest it risk an underwhelming consumer experience. That would be far more damaging, in our view. Could Apple unveil that beta software at its newly announced March 4 event? Quite possible, especially given the company’s choice of words. Apple describes the event as a “special Apple experience.” While the company is expected to unveil some of its newest hardware refreshes, including Macs and perhaps some iPads or the new entry-level iPhone 17e, those hardly qualify as an “experience.” Alongside that event announcement, Apple shared it is working on three new wearable products. While we love our Apple products, and we have many of them, we also realize the first iteration of new products is not always a "wow" out of the gate. We can easily say that about the Vision Pro, and remember it wasn’t until the Apple Watch had built-in cellular service with the third iteration that it started to really take off. When these products take off will hinge not only on when Apple brings these new devices to market, but also their price points and the user experience. Apple arguably flubbed that with the Vision Pro, but perhaps that lesson was learned. As we think about these new devices, and for them to work well and delight consumers, that brings us back to Apple having to nail AI-enabled Siri. So far, that is still to be determined, but we’ll be scouring upcoming beta software releases and report back our findings, including any first looks at the new Siri.

February Price Change: 1.8%; Yield: 0.39%

INVESTMENT THESIS: While we acknowledge that near-to-mid-term performance remains heavily influenced by iPhone sales, the dynamic is shifting as investors finally place greater emphasis on Services growth. We are bullish on the 5G upgrade cycle and believe longer-term upside will continue to come as Services revenue grows its share of overall sales. Services provide for a recurring revenue stream at higher margins, a factor that serves to reduce earnings volatility while allowing for a higher percentage of sales to fall to the bottom line; as a result, we believe that Services growth and the installed base are much more important than how many devices the company can sell in each 90-day period. In addition to improved profitability, we also believe the transparent nature of this revenue stream will demand an expanded price-to-earnings multiple as segment sales grow. Furthermore, we believe that Apple's desire to push deeper into the healthcare arena will help make its devices invaluable as more life-changing features are added and the company works to democratize health records.

Target Price: Reiterate $305; Rating: Two

Panic Point: $222

RISKS: Slowdown in consumer spending, competition, lack of new product innovation, elongated replacement cycles, and failure to execute on Services growth initiatives.

Bank of America Corp. BAC; $49.83; 4,000 shares; 3.73%; Sector: Financial Services

UPDATE: In early January, we bowed to our portfolio discipline and trimmed back our exposure to Bank of America (BAC) when the position size crossed above 4.5%. That of course meant we locked in a tremendous gain on January 5 when we sold that slug of shares at $57.21, roughly a 99% gain. At the Bank of America Financial Services Conference on February 10, BofA CEO Brian Moynihan reminded the company remains focused on expense control, leveraging technology, and further expanding the branch footprint as a springboard for other services, such as wealth management, above and beyond checking accounts and deposits to increasingly own more of the customer relationship. Those near-mid-quarter comments reaffirm the ones made in January for BofA targeting 200-basis points of operating leverage this year, and part of that includes its ongoing AI and digitization efforts as it aims to keep a lid on employee expansion. In mid-February, BofA shared it would put up $25 billion of its cash for private credit deals, originating the deals from its capital markets unit, part of its investment banking division. Exiting December BofA had ~$285 billion in cash on its balance sheet. Private credit concerns weighed on BAC shares as we closed out February, leading them to decline more than 6% for the month, with the bulk of that drop in the last week. In comments addressing that late February selloff, we noted we are in agreement with JPMorgan Chase CEO Jamie Dimon that for now those concerns seem to be overblown as recent private credit woes are isolated. However, we will not bury our heads in the sand, and that means following what develops between now and the RBC Capital Markets Global Financial Institutions Conference on March 10. In our Alert discussing Dimon’s comments, we shared that Bank of America will be one of the presenting companies at the RBC conference, and we view the event as required listening. Based on what we learn ahead of that and from BofA’s presentation, we may have reason to step further into the shares and revisit our rating, especially after locking in a triple-digit gain on a portion of the Portfolio’s position on January at $57.21. As we do that, this week, we’ll look to see if BAC shares deliver a positive test of support at the 200-day moving average near $50.

February Price Change: -6.4%; Yield: 2.25%

INVESTMENT THESIS: Bank of America is one of the world's leading financial institutions, serving individual consumers, small- and middle-market businesses, and large corporations with a full range of banking, investing, asset management, and other financial and risk management products and services. The company provides unmatched convenience in the United States, serving approximately 69 million consumers and small business clients with approximately 3,700 retail financial centers, approximately 15,000 ATMs, and award-winning digital banking with approximately 59 million verified digital users. Bank of America is a global leader in wealth management, corporate and investment banking, and trading across a broad range of asset classes, serving corporations, governments, institutions, and individuals around the world. Bank of America offers industry-leading support to approximately 3 million small business households through a suite of innovative, easy-to-use online products and services. The company serves clients through operations across the United States, its territories, and approximately 35 countries. From a reporting perspective, the company's business breaks down as follows: Net Interest Income breakdown: Consumer Banking 57%, Global Banking 23%, Global Wealth & Investment Management 14%, and Global Markets 6%; Income Before Tax breakdown: Consumer Banking 42%, Global Banking 27%, Global Wealth & Investment Management 16%, and Global Markets 15%. Bank of America pays a quarterly dividend of $0.28 per share, up from $0.18 a few years ago.

Target Price: $65; Rating: Two

Panic Point: $47

RISKS: Financial markets, fiscal, monetary, and regulatory policies, economic conditions, and credit ratings.

Broadcom Inc. AVGO; $319.55; 460 shares; 2.75%; Sector: Technology

UPDATE: Shares of Broadcom (AVGO) languished further in February, leading them to close the first two months of 2026 down more than 7%. That move comes despite ramping demand for AI and data center chips and signs Nvidia remains capacity constrained. That combination bodes extremely well for Broadcom’s custom AI and data center silicon business. As we see it, that brings ample support for the $73 billion in backlog Broadcom shared when it last report its quarterly results. That backlog is expected to ship over the ensuing six quarters, but it is also less than half of Broadcom’s overall $162 billion backlog exiting the October quarter. Remember that guidance was issued before the hyperscalers announced their 2026 spending plans, and before Meta and others announced agreements to shore up available chip capacity. When Broadcom reports this week, we expect a vibrant report and guidance that should support our bullish stance on the shares. We’ll be watching for further improvement in the company’s backlog levels, but even if that figure steps up quarter over quarter, it is possible AVGO shares suffer the same fate as Nvidia’s shares did. We’re of course referring to potentially sky-high whisper revenue guidance. Should that be the case, we have room to add further to the Portfolio’s AVGO position, and if the shares hold support near $320 following their earnings report, that could prompt us to do so.

February Price Change: -3.5%; Yield: 0.81%

INVESTMENT THESIS: We became shareholders in Broadcom to participate as the company benefits from the buildout of digital infrastructure, including AI, data center, and custom AI chips, as well as demand for its software and services segment, which includes private cloud, mainframe software, cybersecurity, and enterprise software. Broadcom reports its business in two segments – Semiconductor Solutions (58% of sales and 51% of operating income) and Infrastructure Software (42%, 49%). The Broadcom management team has developed a track record of delivering organic growth and growth by acquisition, with the latter positioning the company to better position itself to meet developing demands. More recent acquisitions include Brocade Communications, CA, Inc., Symantec Enterprise Security, and VMware.

Target Price: $445; Rating: Two

Panic Point: $290

RISKS: Economic, governmental regulations, geopolitical developments, cyclical, and investment risk.

Eaton Corp. ETN; $375.92; 545 shares; 3.83%; Sector: Industrials