Eyeing This Aging Population Play With Rate Cuts Ahead

Here’s our plan as we approach next week’s Fed policy decision and updated set of economic projections.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

If you’ve been reading our "Signals" pieces, and shame on you if you haven’t, you may remember that almost every one of those alerts has something for our Aging of the Population theme.

At the heart of that strategy is the demographic trend in which the population, both in the U.S. and other countries, is shifting to a larger portion of older individuals. In 2024, Americans over the age of 65 represented approximately 18% of the total U.S. population, numbering about 61 million to 62 million people. That figure is expected to climb to 22% by 2040. Over the next five years, more than 4 million boomers will hit age 80, and that’s in addition to the roughly 4% of the U.S. population that is 80-plus years old in 2024.

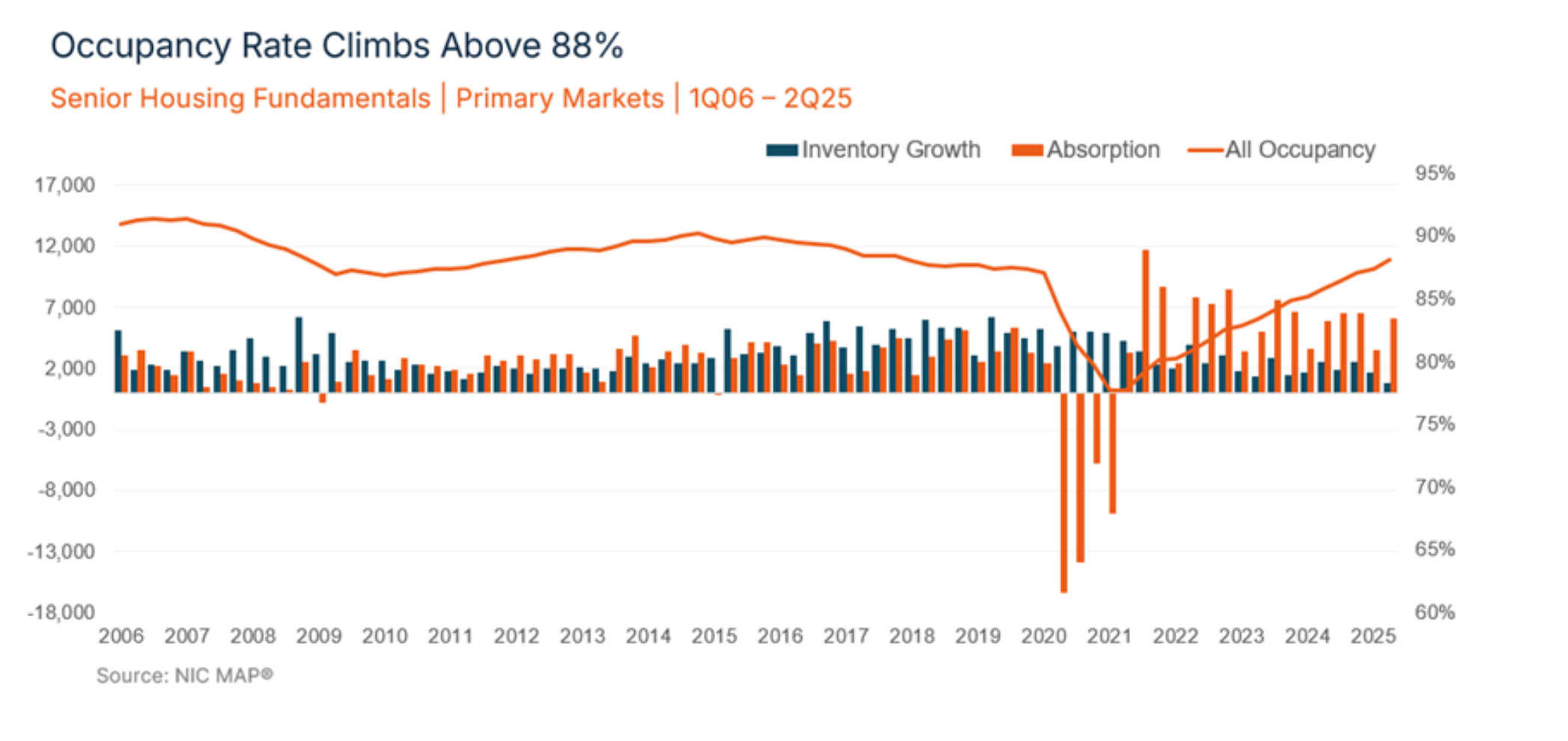

While it may not be as compelling as growth rates in AI and data centers, that demographic tailwind is still a powerful force. But what makes this even more attractive is the ensuing pain point that is the shortage of inventory for senior housing, which fell below 1% in Q2 2025, according to the National Investment Center for Seniors Housing & Care.

With that in mind and the likelihood that the Federal Reserve will start to move monetary policy out of restrictive territory, we’ve taken a fresh look at several companies in the senior housing market. Some of those names have been kicked around here like Ventas VTR, CareTrust (CTRE), American Healthcare (AHR), Bullpen resident Welltower WELL, and a few others. After examining expected EPS growth over the next two years, trading volumes and other factors, we narrowed the list down to three: Welltower, Ventas and American Healthcare.

We then cast off American Healthcare because of its relatively short dividend history — the company only started paying them in 1H 2024, compared to WellTower, which started in 2H 1989, and Ventas, which began paying regular dividends in late 2000. Both of these two remaining candidates offer ample double-digit EPS growth, but what gives WellTower the win by more than a nose is that it returned to being a dividend grower quicker than Ventas did. You see, leading up to 2020, both companies were steadily increasing their annual dividend, but then the pandemic hit, and the two companies both cut their dividends and then held those payouts steady for the next few years.

Entering 2024, Welltower was paying a quarterly dividend of $0.61 per share, and the quarterly dividend now stands at $0.74 per share after two increases. That 21% increase is multiples greater than the eventual 6.6% dividend increase enacted by Ventas this year to $0.48 per share per quarter.

As the Silver Tsunami picks up speed, odds are that both companies will continue to lift their dividends. However, we prefer Welltower over Ventas for a few reasons. First, Welltower derives a larger percentage of its revenue from Resident Fees and Services — 77% in 1H 2025 compared to 70% for Ventas. Second, Welltower’s incremental operating margins are superior to those at Ventas, which tells us Welltower is more adept at driving profits out of every incremental dollar of revenue. Third, Welltower’s financial ratios, including total debt to shareholder equity, total debt to EBITDA, EBITDA to interest expense, and free cash flow metrics, are stronger than those for Ventas.

That validates our thinking for adding WELL shares to the Bullpen, and as you’ve probably noticed, it was a big winner, and one that we unfortunately missed. The reason for that miss was our being correct in thinking the Fed was going to slow walk rate cuts in 2024 and 2025. However, the Welltower price chart reminds us we should pay as much, if not more, attention to our thematic strategy and the ensuing signals and data points.

Lesson learned.

With the Fed likely to deliver a rate cut at its policy meeting and set the table for future cuts, we are dusting off WELL shares, with an eye to calling them up to the Portfolio as a more direct play on our aging population theme. Given our comments on Thursday morning about a potential “buy the rumor, sell the news” event following next week’s monetary policy decision and because the S&P 500’s RSI is approaching a reading of 68 (remember, 70 is the overbought line), we’re going to hold off for now.

If the market does react poorly to next week’s policy decision, we would be inclined to revisit WELL shares over the ensuing days. Key support levels we’ll be watching along the way are the 50-day moving average at $162.70 and the 100-day moving average at $156.18.

The current consensus price target that Wall Street has for WELL shares is $182, and while we work on our own target some more, we’ll share that the average includes multiple price targets near $195 and a few below that average price target that haven’t been updated since December 2024. Crossing those out, we find the real average to be closer to $186. Add in the current dividend yield, and that’s a potential upside return of more than 15% from the 50-day moving average.

Again, as we get closer to the Fed’s policy decision and updated set of economic projections, we’ll work on our own WELL price target. Should we see something more compelling than many others out there, and we see a post-policy pullback, that would be a sweet combination for us.

Stay tuned.