Expect a Bumpy Ride for a Bit

Here's why we see a period of volatility and what's on our shopping list amid the shaky times.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Based on what we are seeing in early trading today, it looks like yesterday’s market rebound will lack follow-through. In other words, market volatility remains in play, even though Pres. Trump announced a partial rollback of tariffs against Canada and Mexico yesterday.

It's a relatively ho-hum day for economic data -- outside of the disappointing February Challenger Job Cuts report -- but the growing unease tied to Trump’s policies and growing questions over their impact on the economy and earnings are once again weighing on the market. That has folks bracing for tomorrow’s February employment report, which will be followed by mid-day comments from Fed Chair Powell.

Comparing the data in ISM’s Manufacturing and Service Purchasing Managers' Index reports for February with yesterday’s disappointing February Employment Change report from ADP sets the stage for tomorrow’s February Job report. Despite that cloudy picture and the initial impact of DOGE-related cost cuts, the market consensus still sees job creation picking up the gap in February to the tune of 160,000 non-farm jobs, up from January’s 143,000.

We see, however, ample room for the market to be disappointed. This morning’s February Challenger Job Cuts report showed a spike in layoffs to their highest level since 2020. Also, in the Job Cuts report, more than a third of the 172,017 layoffs were the result of federal government job cuts.

In the twisted logic that Wall Street is known for, such bad news would be viewed favorably. Why? The disappointing employment numbers could prompt the Fed into action. The CME FedWatch Tool shows three quarter-percentage point rate cuts for this year.

When we look at the price component data tucked inside ISM’s February Manufacturing and PMI reports, it jumped to its highest levels in the last several months. This combination should make for some very interesting comments from Fed Chair Powell on Friday. And, yes, the market will more than likely be hanging on those comments and what they mean for rate-cut expectations.

With inflation already perking up and more to come from expected tariffs, it’s hard to see Powell backing that market’s monetary policy outlook. Several quarters ago the Fed chair said there could be some pain involved in getting inflation back to the Fed’s 2% target. Should Powell reiterate those comments tomorrow, it would be the equivalent of Powell throwing some cold water on rate cut expectations.

All this means that market volatility is likely to persist at least through the end of the week and potentially longer. Remember, Mexico is expected to announce retaliatory tariffs over the weekend, and Trump targets April 2 for more widespread retaliatory tariffs.

Here's our plan and shopping list

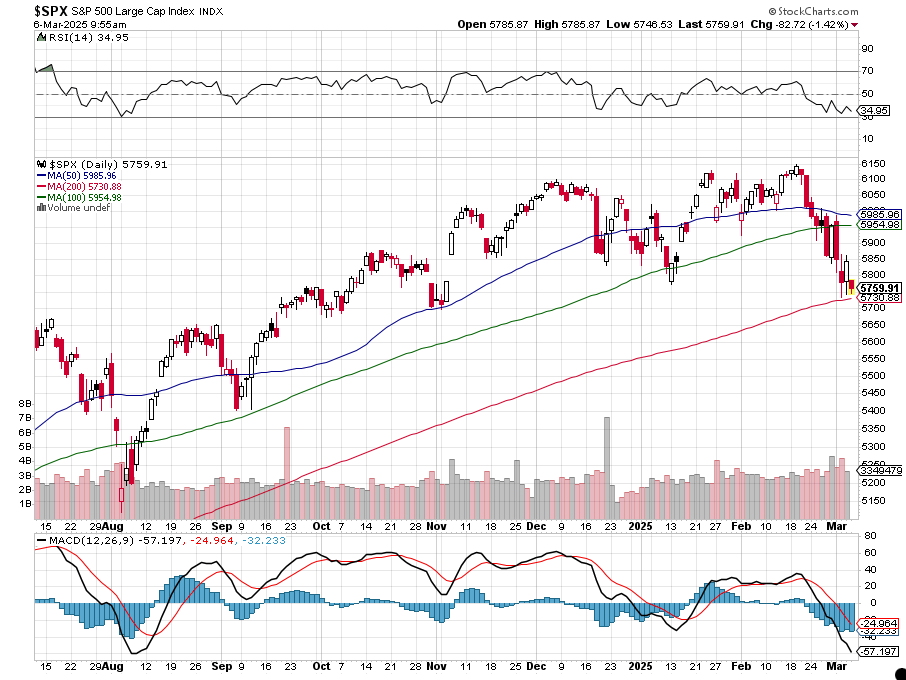

We will continue to be mindful of the market’s technical setup, especially as the Extreme Fear the Fear & Greed Index is flashing. We're watching key support levels and moving average convergence divergence trends, and also the S&P Short Range Oscillator. In the cart below, we can see the S&P 500 is closing in on its 200-day moving average, and its relative strength index is once again nearing oversold levels.

While we took advantage of some individual stock technical setups yesterday, caution is warranted at least until we get tomorrow’s February jobs report and Powell’s comments. Until then we’ll let our cash and inverse exchange-traded funds do their jobs. Companies that remain on our shopping list are the newly one-rated Marvel MRVL, Axon AXON and American Express AXP. At lower prices that expands to include Dutch Bros BROS. For folks that are underweight Eaton ETN, ServiceNow NOW, and Vulcan Materials VMC, those are ones to watch as well.

At the time of publication, the Pro Portfolio was long MRVL, AXON, AXP, BROS, ETN, NOW and VMC.