We're Downgrading This Holding as Consumer Confidence Wanes

Plus, Oracle’s earnings, NFIB’s Uncertainty Index and airlines dial back expectations.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

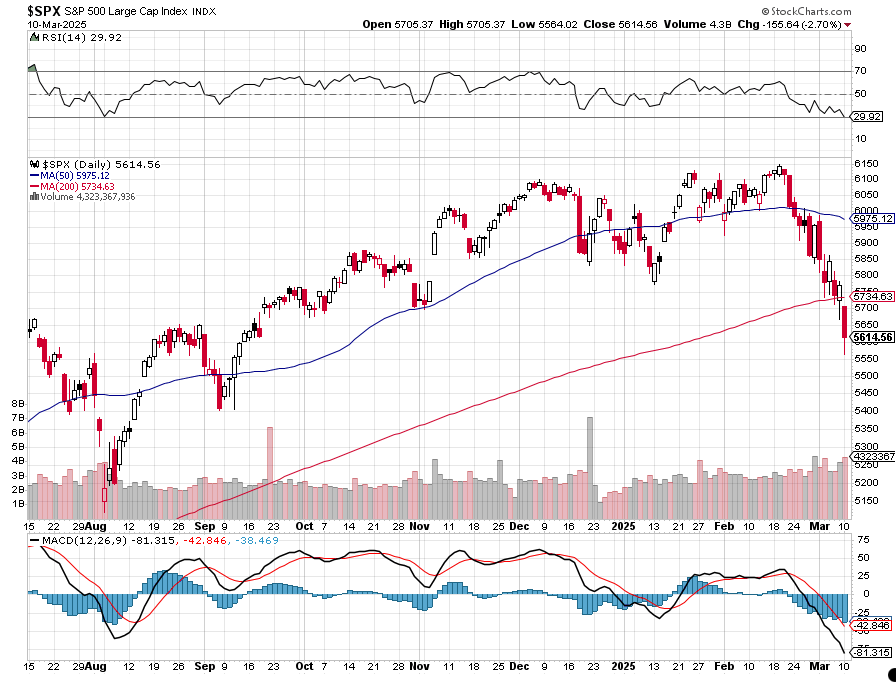

On Monday, the S&P 500 approached oversold territory, and the Nasdaq Composite closed firmly in that camp. That suggests we could see a market rebound emerge, but the question is how sustainable it will be given prospects for additional tariffs and a growing list of companies delivering weaker-than-expected outlooks.

The former will keep inflation concerns going while the latter raises more questions about S&P 500 EPS growth prospects and the market multiple.

In Monday's video, we discussed the decline in 1H 2025 EPS expectations for the S&P 500 as well as the increased ones for 2H 2025, which as of Friday were expected to climb 14% versus 1H 2025. That’s up from 10% earlier this year and based on what we’re seeing of late it seems aggressive.

Oracle Misses but Brings Support for Four Holdings

In that camp, we can include Oracle ORCL, which not only missed consensus expectations for its February quarter, but its guidance for the current one also came up short of market forecasts.

Granted, the market was likely more focused on Oracle’s Remaining Performance Obligations topping $130 billion, but the reality is that the company came up short for the near term. As it relates to our Nvidia NVDA and Marvell MRVL holdings, Oracle reaffirmed it is “on schedule to double our data center capacity this calendar year.”

Oracle also shared that “customer demand is at record levels” and it is seeing “enormous demand” for AI. Those comments keep us bullish on ServiceNow NOW and Elastic ESTC.

More Concerns About the Consumer

Last night and this morning we saw Delta Air Lines DAL, American Airlines AAL, JetBlue Airways JBLU and Southwest Airlines LUV all dial back expectations for the current quarter. As part of its comments, Delta called out “recent reductions in consumer and corporate confidence caused by increased macro uncertainty, driving weakness in Domestic demand.”

What stood out to us was Delta’s comment that its Premium and International revenue growth trends are tracking as expected.

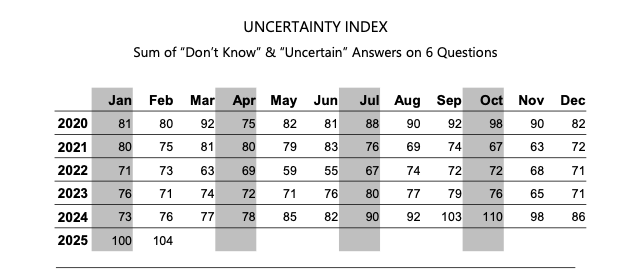

Supporting that view, on Tuesday morning the Uncertainty Index level in the February Small Business Optimism Index rose to 104, marking the second-highest recorded reading. It’s pretty safe to say that, when companies are facing an uncertain outlook, they tend to restrain their spending and hiring. That helps explain the pop we saw in last week’s Challenger Job Cuts report to 172,014 layoffs as well as the roughly 108,000 layoffs not associated with the impact of DOGE.

We’ve also seen an array of retailers in recent days deliver downside guidance, and to that on Tuesday morning we can add Kohl’s KSS and Dick’s Sporting Goods DKS. While Kohl’s delivered an EPS beat for its January quarter, comp sales for the period fell 6.7% and its guidance for the coming year sees continued comp sales declines in the range of 4% to 6%. That was a key factor in the company guiding its fiscal 2026 EPS to $0.10 to $0.60, well below the $1.18 market forecast.

Downgrading Mastercard to a Three

All of this is leading us to downgrade the shares of Mastercard MA to a Three rating from Two. If we see a market rally emerge, we may elect to trim back the Portfolio’s exposure to MA shares. A dramatic increase in jobless claims could be another catalyst for that as well.

As we make that adjustment, we suspect we’ll get questions about American Express AXP shares. While many folks associate Amex and Mastercard, let’s remember their revenue models are quite different because Amex derives 65% of its pre-tax income from net card fees.

More Pressure Now for Trump Tax Cuts

One potential wild card we are watching is Trump's tax cuts.

Reports have indicated a July target, but we are hearing rumblings that we could see something by late May. That could be the “pick me up” the economy needs, but that’s at least two-plus months away at the earliest. The potential timing would support stronger EPS growth in 2H 2025, but we would still need to get past March quarter reporting and June quarter guidance.

More Pro Portfolio

- We're Adding More Shares of These 5 Portfolio Holdings

- Weekly Roundup: Here's Our Game Plan as We Focus on Our Updated Shopping List

- Big Spenders Vs. Cash-Strapped Shoppers, AI, Hacks and Other News for Investing

At the time of publication, TheStreet Pro Portfolio was long NVDA, MRVL, NOW, ESTC, MA and AXP.