We're Downgrading This 'Dead Money' Name, Making Exit Plan as Headwinds Intensify

Fresh inflation and mortgage data points to a lengthening road to a housing rebound and bad news for this holding.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

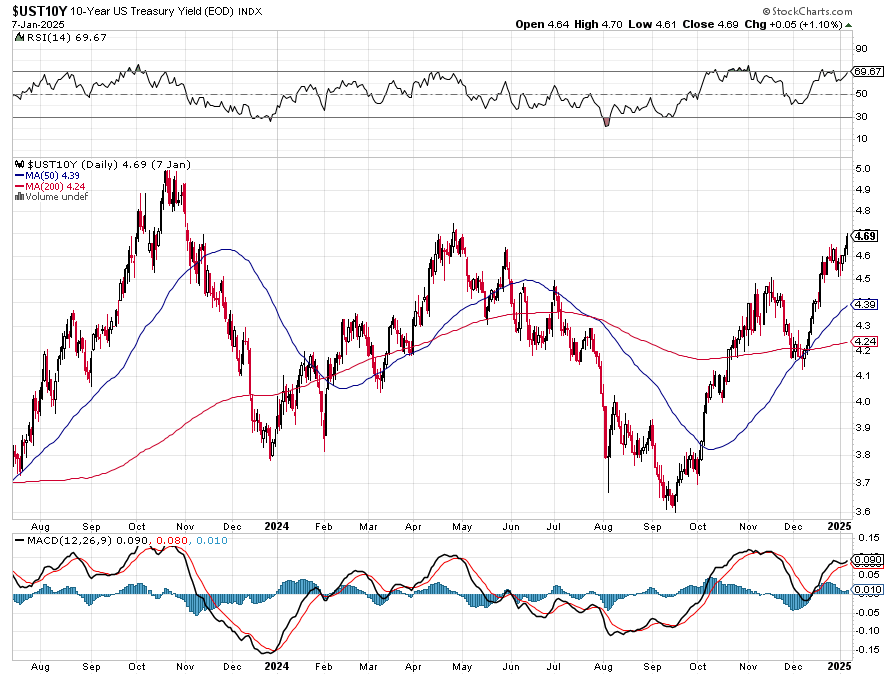

Following up on our comments regarding ADP’s December Employment Report, inflation and the Fed from earlier on Wednesday, we have seen the 10-year treasury yield inch up further, hitting its highest level since April.

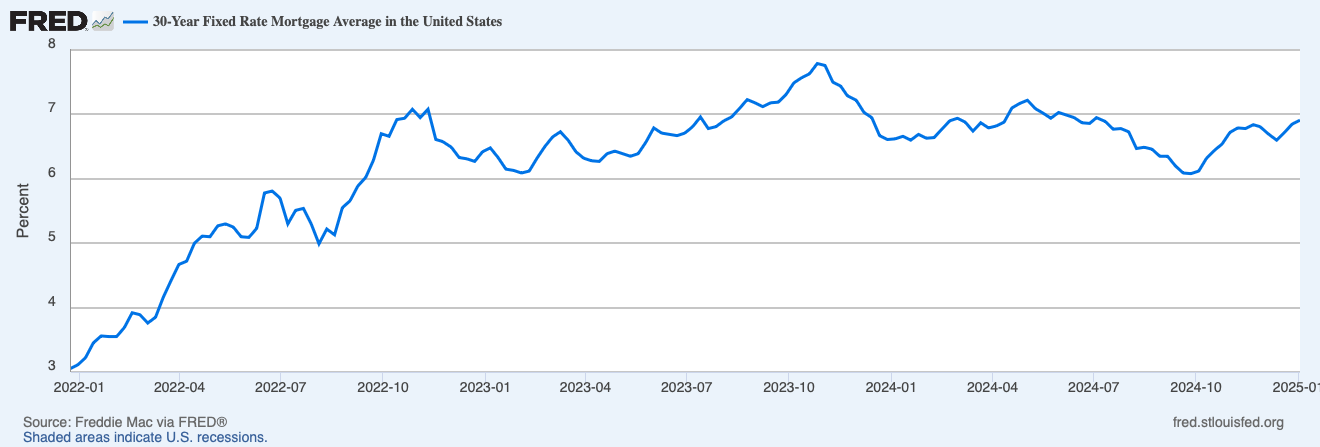

That climb has led to a similar move up in 30-year fixed mortgage rates, which are now back just above 7%, much higher than where they were in late September-early October.

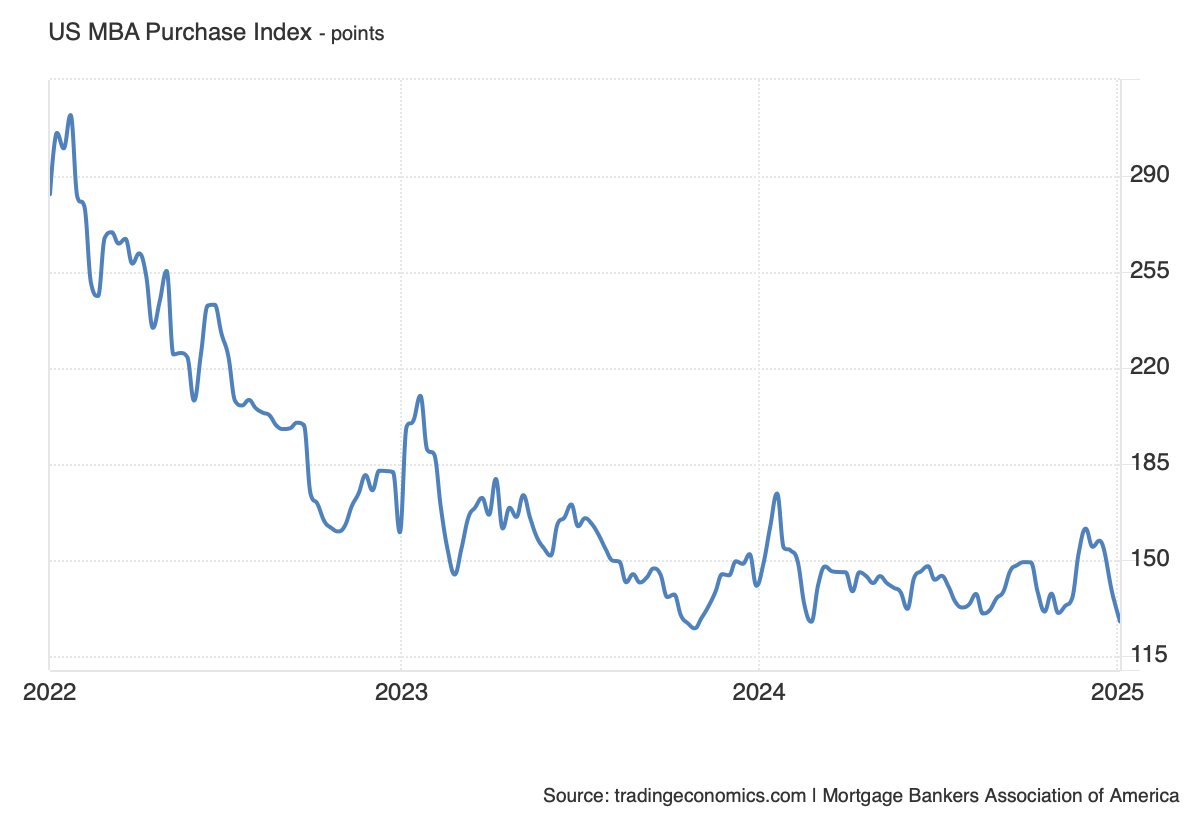

That rebound in mortgage rates, especially during the last month of 2024, led the Mortgage Bankers Association’s Purchase Index to rollover in December, suggests the expected rebound in housing demand isn’t going to unfold as quickly as some had hoped. This week’s inflation data and other economic figures that now put Q4 2024 GDP at 2.7% increase the probability that it will be some time until the Fed delivers its next rate cut.

While stocks can be beaten down and arguably cheap relative to the long-term potential, they can also become dead money as headwinds emerge pushing out the timetable for a potential rebound.

That’s what we’re seeing unfold with the shares of Builders FirstSource BLDR.

As we discussed on Tuesday, BLDR shares remain oversold, but they have also crossed below our panic point and the outlook for the housing market becomes, shall we say, less appetizing. With a lack of positive catalysts on the horizon so long as inflation remains sticky and the Fed’s composition become incrementally less dovish, odds are BLDR shares will be dead money for the next several months.

That means we will want to put the capital tied up in BLDR shares to better use.

The confluence of factors laid out above are also likely to lead to a rash of price target cuts, which could also keep a lid on the shares. In fact, we’re seeing some price targets cuts on Tuesday and Wednesday for some homebuilders, with UBS and Citi reducing price targets for Toll Brothers TOL and D.R. Horton DHI. As we look across other Wall Street price targets, we see a cluster for BLDR shares in the $220 to $230 range, many of which established or reiterated back in September, October and early November.

Finally, given what we described above regarding mortgage rates and housing prospects, the likelihood is high that new CEO Peter Jackson will reset Builder’s outlook. While we continue to think the company is well positioned long-term, slower housing volumes are going to weigh on its business and operating leverage. Much like those price targets we mentioned above, we have yet to see any major change in EPS expectations for the December 2024 or March 2025 quarter in the last 60 days.

Our Exit Plan as We Downgrade BLDR Shares

All of that, especially the far hotter-than-expected inflation reading from ISM this week, is leading us to downgrade BLDR shares to a Four rating, which also means we are rescinding our price target.

Similar to our recent exit with PepsiCo PEP shares, we will look to use a rebound in currently oversold BLDR shares to work our way out of the position. However, if Friday’s December Employment Report or next week’s December CPI and PPI data suggest further Fed rate cut timing recalibration is needed, we may not wait.

As we work our way out of this stock, we'll either re-arm our cash position or opportunistically put that returned capital to work in companies benefitting from tailwinds and poised to deliver better earnings growth prospects.

More Pro Portfolio

- Increasing AI Spending in 2025 Leads Us to Buy More Shares of This Holding

- Weekly Roundup: Off to a Good Start Despite Santa Arriving Too Late

- Large Language Models Eat Up Big Electricity -- and Other Stories That Speak to Our Portfolio

At the time of publication, TheStreet Pro Portfolio was long BLDR.