Don’t Get Distracted By All Those S&P 500 Price Targets

We’ll heed the underlying expectations but focus on the developing road ahead.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The market had two very strong back-to-back years in 2023-2024, with the S&P 500 rising more than 20% each year. Several factors contributed to those gains, ranging from stimulus policies out of Washington, AI adoption, and the Fed loosening monetary policy.

Expectations for further gains this year range from a low of 2% to the consensus of just over 11% to a high of 20% — and there are a wide range of assumptions behind those numbers, from further Fed rate cuts to the speed of the economy to tax reform. There are also many uncertainties, including the use of tariffs by the Trump White House, the corresponding impact on inflation, and what that could mean for monetary policy.

Those factors and uncertainties, and others like them, are all moving parts that make it challenging to deliver a price target for the S&P 500, which is why we don’t. We do, however, look at the thought process behind the projections shared by others to decipher what the market expects.

When we first look at those targets, we begin with expected earnings for the basket of stocks that comprise the S&P 500 and the implied P/E multiple, examining them against historical levels, especially those that approximate the environment we’re likely to face.

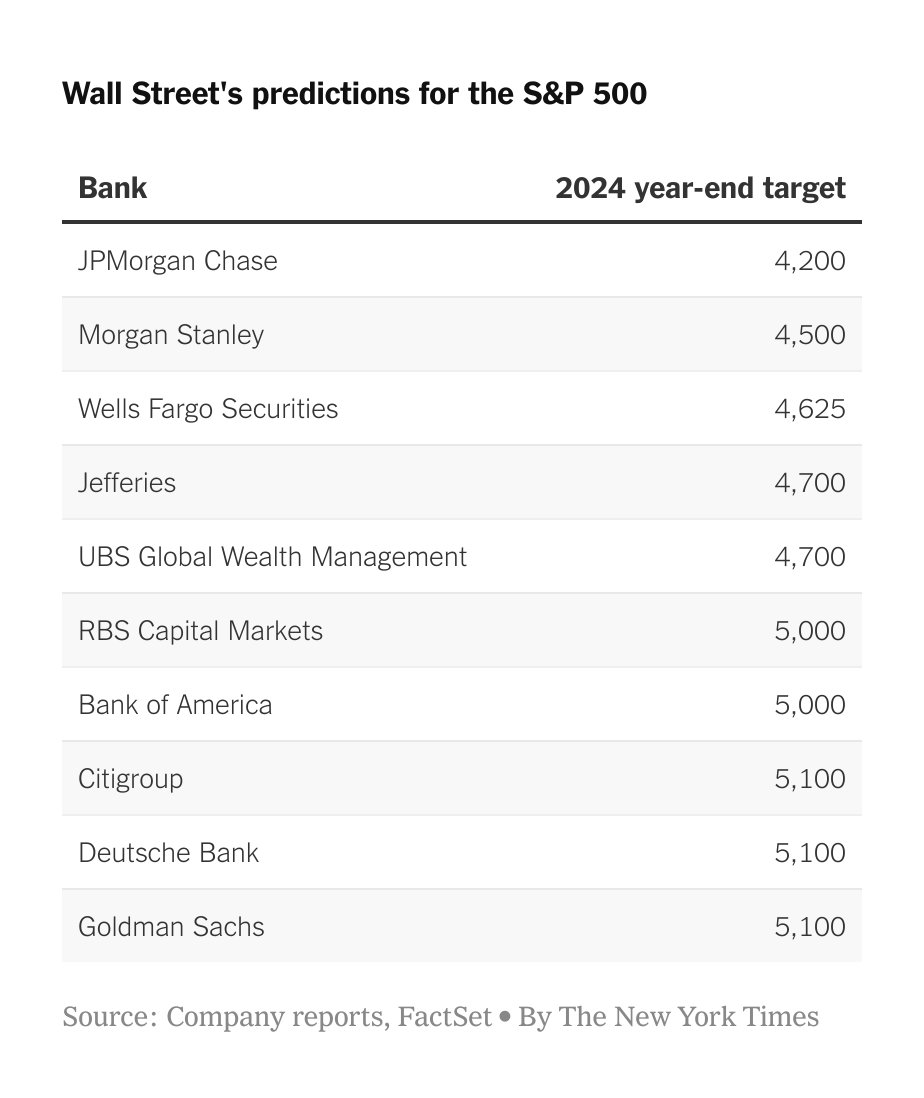

As you can imagine, as that path becomes clearer it means revisiting this analysis, usually multiple times. This should explain why we track consensus EPS and EPS growth for the S&P 500 as closely as we do. And that's why we don’t hold it against those who really missed the mark with their 2024 S&P 500 price targets presented at the end of 2023.

It also explains the wide range of S&P 500 price targets for 2025:

Oppenheimer: 7100

Wells Fargo: 7007

Deutsche Bank: 7000

SocGen: 6750

BMO: 6700

HSBC: 6700

BofA: 6666

Barclays: 6600

RBC: 6600

Citi: 6500

Goldman: 6500

JPMorgan: 6500

Morgan Stanley: 6500

UBS: 6400

BNP Paribas: 6300

Cantor: 6000

Do we expect the folks above to revise those targets at least a few times in the coming year? You bet, and odds are the first round of adjustments will come as we wind up the upcoming December 2024 earnings season, which brings with it the first hard look at company guidance for 2025. That of course assumes those companies offer full-year guidance, not just their take on the March 2025 quarter.

The next potential set of revisions could be fueled by a clearer understanding of tariff usage and its impact once President Trump is back in the White House. Knowing that one of Trump’s strategies is to keep his negotiating opponents off balance, we could face a bit of a roller-coaster ride until further clarity is achieved.

What We’re Going to Do

As we said above, we’ll be mindful of those projections, but because we do not “buy the market” we will continue to focus on companies whose businesses are benefiting from multi-year structural tailwinds, are poised to deliver superior earnings growth, and whose shares offer a favorable risk-to-reward entry point. In other words, remaining disciplined as well as prudent, continuing to manage the portfolio as we have.

As EPS expectations for the S&P 500 change, we’ll adjust our EPS hurdle rate for potential portfolio candidates.

We’ll also keep watch on the S&P 500’s market multiple and technicals so we know when things are stretched both for the market and also for stocks as measured by a relative P/E valuation to the market.

Do we expect the path forward to be an evolving one? Of course, which is why we will continue to follow the data and let it talk to us, course-correcting the portfolio as needed.