CPI Shows Progress, but Far More Is Needed Before Next Rate Cut

The data isn’t going to move the Fed’s cautious stance on rate cuts just yet.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Much like Tuesday's sigh-of-relief data found in the December Producer Price Index, we are seeing the market rebound following Wednesday's December Consumer Price Index (CPI), which showed core CPI figures below the consensus forecast.

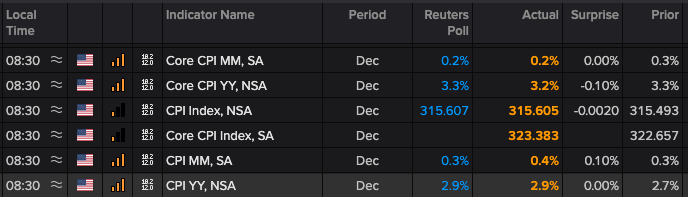

On a year-over-year basis, core CPI came in at 3.2% versus the expected 3.3% and the 3.3% reading for November. Shifting to a sequential basis, core CPI for December came in at 0.2%, matching the market forecast and inching down from November’s 0.3% reading.

What’s stoking the market mood is the December reading for supercore services, which rose just 0.21% on the month, the lowest reading since July. To be clear, supercore measures services inflation excluding food, energy and housing, or as we like to think, the things we utilize in our everyday lives.

At the same time, however, headline inflation ticked up compared to November on both a sequential and year-over-year basis. Much of that move higher came from a 2.6% gain in energy prices for the month, pushed higher by a 4.4% surge in gasoline. Food prices also rose, up 0.3% for the month.

Our Take

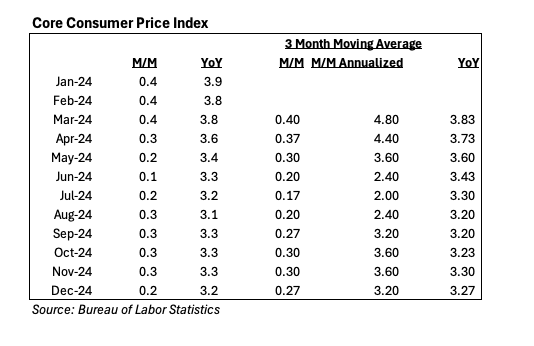

While there are some positives in the data, including the trailing three-month annualized core CPI reading falling to 3.2% in December versus 3.6% in November and October, the reality is that the year-over-year inflation figures are still quite a distance from the Federal Reserve’s 2% target. It’s going to take far more progress on a sustained basis to get the Fed more comfortable with delivering its next rate cut.

Still, the December core CPI data surprised the market in a good way and adds to the likelihood its markup in inflation expectations may have been overly aggressive following the December Service PMI data from ISM. This is helping stocks rebound following that ISM data and backs our decision to put some capital to work for the Portfolio on Tuesday.

Now the attention shifts to earnings season. Our initial take is positive on earnings this morning from JPMorgan Chase JPM, Goldman GS and others. We’ll have more in-depth thoughts coming once we digest their earnings calls and transcripts.