China Faces New Pressure on Trump Trade Negotiations

The latest economic data out of China suggests the country could be losing some leverage.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Equity futures point to a down open later on Tuesday morning as trade tensions remain in the air. Late on Monday, in a bid to speed up negotiations with multiple partners ahead of a self-imposed deadline just five weeks away, the Trump administration urged countries to submit their best trade offers by Wednesday. That move follows President Trump accusing China of violating a temporary trade agreement, while China accused the U.S. of doing the same.

Meanwhile, the Caixin China General Manufacturing PMI unexpectedly declined to 48.3 in May, down from April’s 50.4 and below the market consensus of 50. This marked the first contraction in eight months and represents the steepest decline since September 2022. Looking below the headline figure, we find output shrank for the first time in 19 months and at the fastest pace since November 2022, while new orders contracted at the sharpest rate since 2022. Going one layer deeper, we find foreign sales fell to their lowest level since July 2023 given the current trade environment.

Adding to those trade pressures, as we discussed on Monday, last week Trump said he planned to increase tariffs on imported steel and aluminum to 50% from 25%, ratcheting up pressure on global steel producers and deepening his trade war. The European Union, which is currently negotiating with the White House to avoid the delayed tariff increase now set for July 9, warned that this “undermines” negotiations.

Our sense on all the above is that the Trump administration is looking to put some needed wins on the board and is drawing on Trump’s usual playbook: keeping opponents off balance is a key tactic for gaining an advantage in negotiations. Being unpredictable and sometimes assertive helps create leverage and can lead to more favorable outcomes. While that may work when negotiating with one or two countries, time will soon tell how fruitful that strategy is when negotiating with a much wider swath of countries.

On Monday, we shared that we are back in the realm of the market trading day to day based on the latest headlines. That means we expect volatility to remain with us near-term and that keeps us in a cautious stance as we look to tap our near-term shopping list that includes Elastic ESTC and Marvell MRVL shares.

Following the Data

It also means now more than ever we will continue to follow the data and other signals to blunt the market noise and focus on where opportunities lie. With that in mind, we’ll continue to connect the dots as Dollar General DG, CrowdStrike CRWD, Hewlett Packard Enterprise HP, Dollar Tree DLRT, Sprinklr CXM, Five Below FIVE and PVH PVH have to say when they report quarterly results on Tuesday and Wednesday.

Following the data also means heeding the newest forecast from World Semiconductor Trade Statistics (WSTS), which calls for the global semiconductor market to grow by 11.2% in 2025, reaching a total value of $700.9 billion. The forecast sees double-digit gains in the logic and memory segments supported by sustained demand in areas such as artificial intelligence, cloud infrastructure and advanced consumer electronics. Supporting that outlook, at its annual shareholder meeting earlier on Tuesday, Taiwan Semiconductor TSM said that U.S. tariffs were having some impact on its business, and demand for AI continues to remain strong and outpaces supply. Nice support for our positions in Nvidia NVDA and Marvell.

TSM CEO C.C. Wei also weighed in on tariff and inflation saying, “…tariffs can lead to slightly higher prices, and when prices go up, demand may go down.”

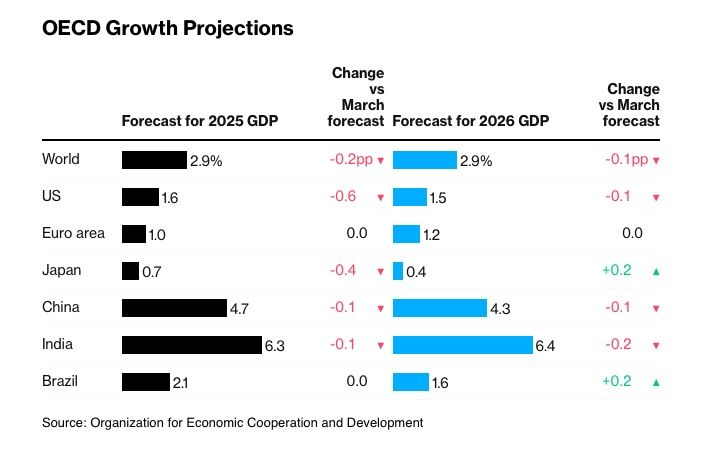

That comment helps explain why the OECD slashed its global forecasts for the second time this year, citing the impact of President Trump’s tariffs. Per the OECD, the combination of trade barriers and uncertainty is hitting confidence and holding back investment while also warning that protectionism is adding to inflationary pressures. The OECD now forecasts global economic growth to slow to 2.9% this year from 3.3% in 2024. It expects the rate of expansion in the U.S. will tumble further, to 1.6% from 2.8%. The OECD also sees Inflation in the U.S. moving higher this year, making it likely that the Federal Reserve will not resume easing policy until 2026.

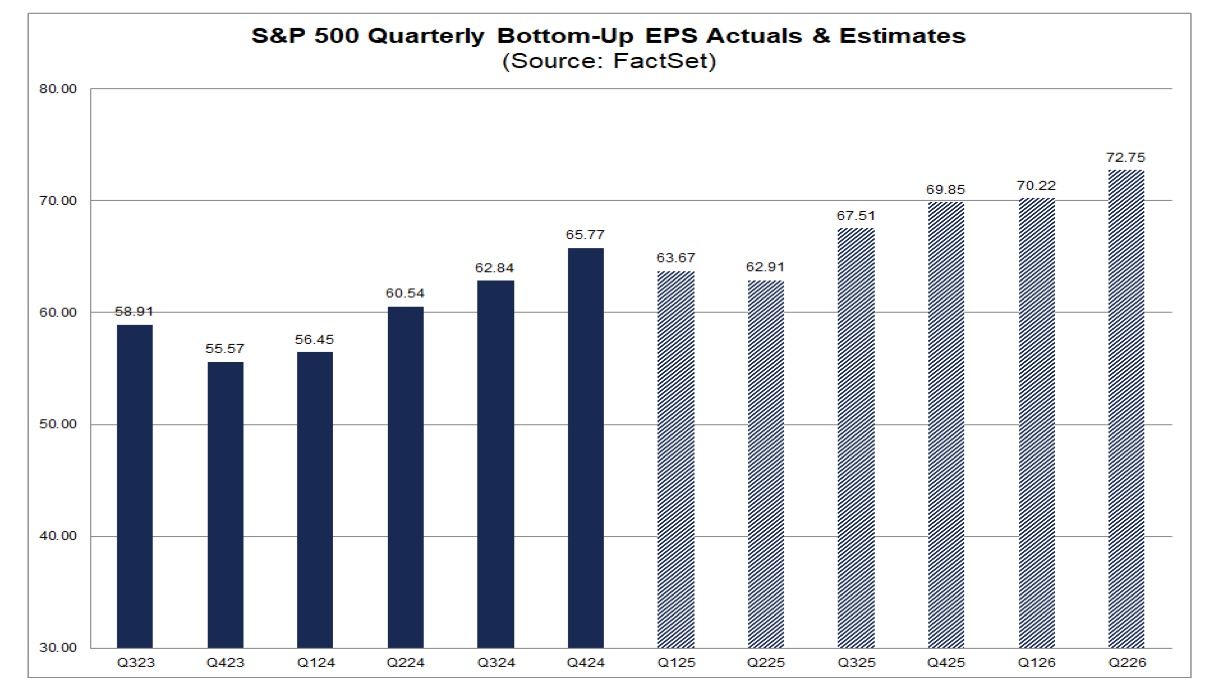

Against that backdrop, we’ll be particularly interested in company comments about the current quarter and 2H 2025 as the June investor conference season heats up. Data tallied by FactSet shows that during April and May, Wall Street analysts lowered EPS estimates by a larger margin than average. That led to lower 2025 EPS estimates for the S&P 500, which stood at $264.49 on May 29, down from $269.92 in late March and $272.67 in late January.

Despite those downward revisions, the market still expects S&P 500 EPS to grow 8.5% compared to 1H 2025, and almost 7% compared to 2H 2024. Our view has been the longer we go without formal trade deals and the details they bring, the more likely EPS expectations for the coming quarters will need to be revised lower.

As of now, we see no reason to amend that line of thought and it’s another reason why we will be heeding company management comments this week and next. That’s especially true for Axon Enterprise AXON as its shares have moved past our $750 price target and its management team presents on Tuesday and Thursday at the Baird 2025 Global Consumer, Technology and Services Conference and the William Blair 45th Annual Growth Stock Conference.

More Pro Portfolio

- We're Cashing Out of This Holding After a Big Move

- Monthly Roundup: A Good May for the Market. Even Better for the Portfolio.

- Apple Glasses, AI Travel Agents, Aging States and More News for Investing

At the time of publication, TheStreet Pro Portfolio was long MRVL, ESTC, NVDA and AXON.