Breaking Down Wall Street's Rising S&P 500 Price Targets for 2026

Is hitting these targets realistic? Here's what it will likely hinge on.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

As we get ready to gear up for a busy Wednesday, one that includes the Fed’s policy decision and updated set of economic projections, the Barclays 23rd Annual Global Technology Conference, and quarterly results from Oracle (ORCL) and Adobe (ADBE) , we’re seeing a string of rising price targets for the S&P 500.

UBS sees the index rising some 10% by the end of next year to 7500.

RBC Capital Markets? 7750.

Morgan Stanley’s target for the S&P 500 over the next 12 months is 7800.

Deutsche Bank is at 8000.

And the most bullish? Oppenheimer with its 2026 target at 8100, and its year-end 2025 target of 7100.

At the heart of Oppenheimer’s uber-bullish outlook?

"At the core of what lies ahead for our 2026 target price to be achieved lies monetary policy, fiscal policy, and the continuing progress of innovation and corporate earnings growth, all of which have been supportive of stock prices and are key to growing earnings and revenues in the year ahead."

Pretty much the usual factors and forces.

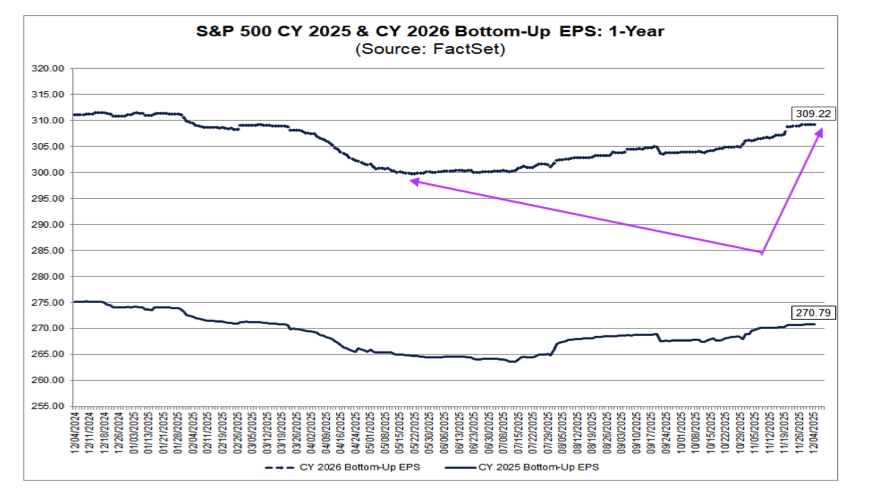

The chart below shows the rising expectations for S&P 500 EPS levels next year.

What we can observe is that, based on the current 2026 consensus EPS figure tallied by FactSet, those clustered S&P 500 targets between 7750 and 8100 imply a P/E multiple in the range of 25.1x-26.2x. And for those wondering, as we write this, the S&P 500 is trading at 25.3x expected 2025 EPS of $270.79. This means the bulk of the expected gain in those S&P 500 forecasts is tied far more to EPS growth than multiple expansion.

As we move into 2026 and companies start to issue their initial outlooks for the year, the aggregate guidance and supporting industry data will need to support the implied 14% EPS growth compared to 2025. Except for 2021, which benefited from the pandemic re-opening, that 14% figure would be the fastest rate of annual EPS growth since 2018’s 21% figure, which was backed by the Trump tax cuts.

Typically, the economy, the strength of a company’s particular end market, company-specific positioning, pricing power, and input costs are key factors that influence revenue and EPS expectations. However, next year, corporations will be able to claim 100% bonus depreciation on qualifying property due to the passage of the "One Big Beautiful Bill Act" this year, which made the deduction permanent. The thinking is that while this would reduce net profit and table income, it should be a positive for cash flow that would help fund investment spending. It could also be used to foster larger stock buyback programs.

To the extent companies take advantage of this accelerated deduction, it could be a reason to think that the 14% expected EPS growth rate for the S&P 500 next year is a tad aggressive. We’ll want to parse corporate guidance carefully to understand the puts and takes here and its implications for bottom-line expectations. But we can say that our focus on companies poised to deliver faster EPS growth than the S&P 500 remains in place.