Better-Than-Feared February Jobs Report Points to No-Go on First-Half Rate Cuts

Plus, here's why Jerome Powell’s comments Friday could remove a life preserver for the market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

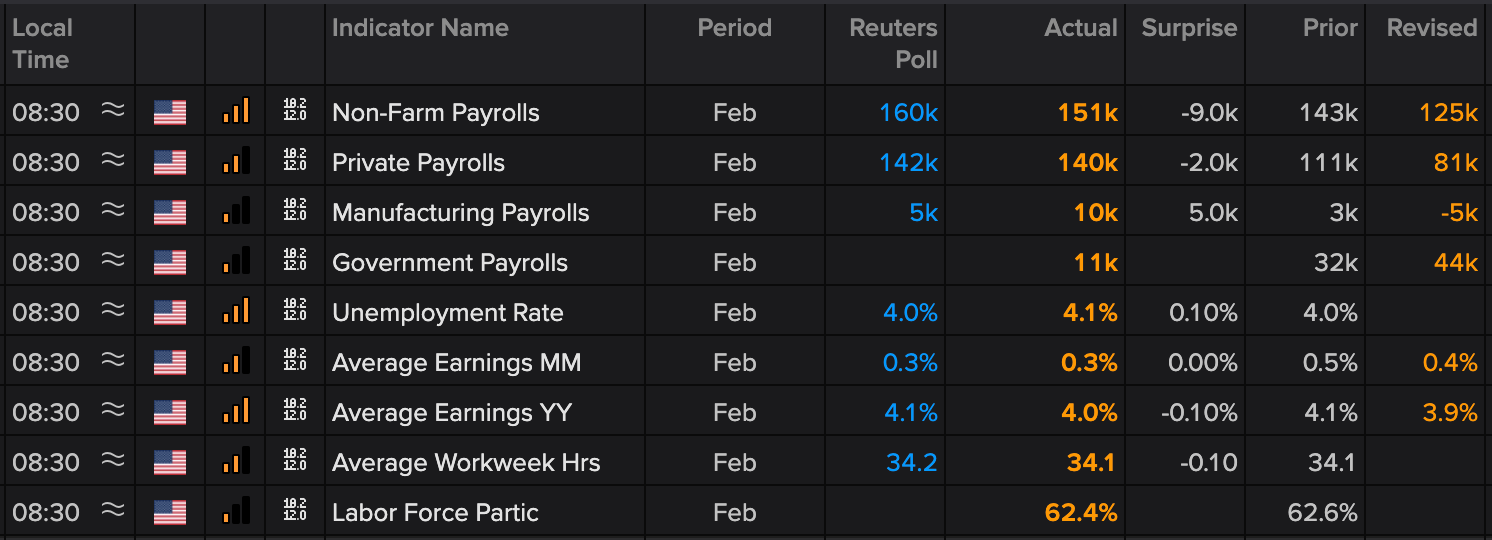

We saw a better-than-feared February Employment Report Friday morning, which showed 151,000 jobs added during the month, up from the downwardly revised January figure of 125,000. Granted, the February figure missed the 160,000 market consensus estimate, but following Thursday’s eye-popping surge in the February Challenger Job Cuts report to 172,017, the market will give a pass to the February jobs miss.

While that is relatively good news for the economy, that level of job growth is not going to push the Fed into rate-cutting action anytime soon, especially following the surges in February ISM pricing data. In other words, the combination of Friday’s jobs report and ISM’s February PMI pricing data does not support the two rate cuts by July expected by the market, per the CME Fed Watch Tool.

Earlier Friday morning, Atlanta Fed President Raphael Bostic said a pause in rate cuts could be in place until summer 2025. Based on recent data, we see that as very probable and suspect the timing could be even longer. Odds are that will be the message from other Fed heads today, including Chair Jerome Powell. With tariff uncertainties still in the air, we expect Powell will reiterate the Fed being data dependent.

We too will continue to follow the data, in part because we recognize the potential delayed impact of private sector job cuts captured in the February Challenger report and federal job cuts being found in the data. However, that same PMI pricing data suggest we aren’t likely to see any meaningful improvement in next week’s CPI and PPI data for February. This leads us to think midday comments from Powell are likely to toss some cold water on market rate cut hopes later Friday, effectively removing a potential life preserver for the market.

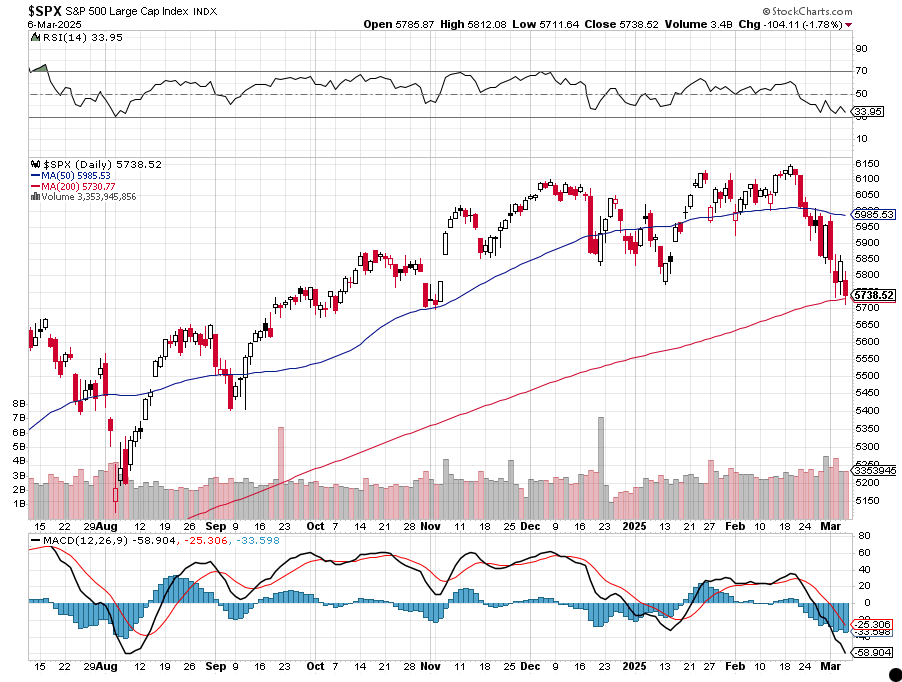

Factor in comments from President Trump Friday morning that tariffs could go up as time goes on, and Mexico expected to reveal its response to recent Trump tariffs over the weekend, and barring the market becoming deeply oversold Friday we’re inclined to remain on the sidelines as we close out the week. We will keep a close watch on the S&P 500 relative to its 200-day moving average near 5731 as well as other technical indicators for that market barometer. Market oscillators are oversold but based on the past there is room for them to become even more so and that could pressure the market to 5600-5650.

To us that means we will need to be even more prudent than usual, carefully choosing our spots to put capital to work. We suspect there will be a point in time to we will want to trade in our inverse ETFs and put more cash to work, but for now, we’ll let both do their jobs while we continue to work on refreshing the Bullpen.