As Trump Wrestles Over Trade, Market Gets Thrown for a Loop

Let's digest the latest tariff news and Samsung’s Q2 profit drop.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

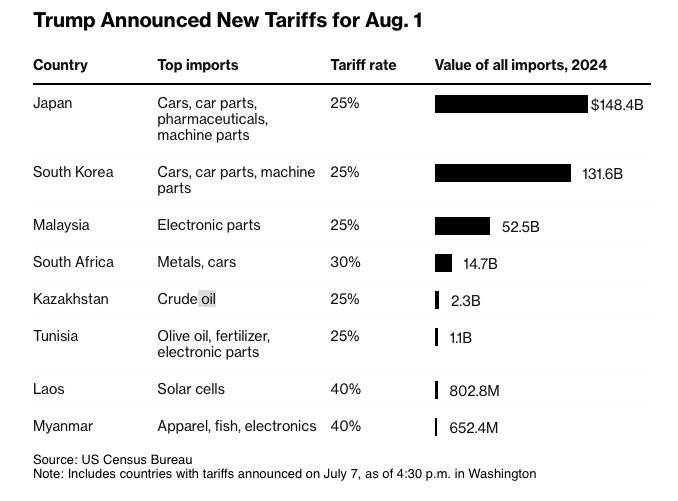

The market is digesting the 14 letters sent by the White House that raise tariffs on Aug. 1, and as we discussed yesterday, they are doing the same with the revelation that now U.S. tariffs will return to April 2 levels on Aug. 1 if there is no progress on trade deals with the U.S.

We continue to see that move by Pres. Trump as an attempt to jump-start trade talks as timetables for those conversations, especially with the eurozone and China, were going to miss the Trump-imposed July 9 deadline. According to Trump, "we're not going to be unfair" and the administration would look favorably on countries continuing to offer additional concessions, as he suggested he was still open to negotiations.

Trump also faces a mid-August deadline with Beijing, where tariffs on Chinese goods could snap back to 145%. Unsurprisingly, this morning, China warned the Trump administration against reigniting trade tensions by reinstating tariffs on its goods in August and threatened to retaliate against nations that strike deals with the United States to exclude China from their supply chains. How this plays out following the June deal between the U.S. and China that set U.S. tariffs on Chinese imports at 55% and Chinese tariffs on American imports at 10% has yet to be determined.

We are also waiting to see what is announced on the trade-deal front following comments yesterday from Treasury Sec. Scott Bessent that the Trump administration will make “several” trade-related announcements in the next 48 hours. While we will keep an open mind and focus on the details of what is announced, we continue to think that, absent a surprise agreement with the eurozone or China, which we view as very unlikely, odds are the market will be underwhelmed by what is announced.

What we do know is we have another round of uncertainty injected into the market, and as we’ve mentioned ample times to you before, that increases the potential for companies to be conservative when they update their outlook for the current quarter and second-half of 2025 in the coming weeks. This means more so than usual, we will be collecting comments as the volume of quarterly earnings grows louder, as well as gauging the market reaction to what is shared.

Currently, the Fear & Greed Index is flashing “Extreme Greed,” and the Volatility Index (VIX) at 17.79 doesn’t scream complacency. That suggests market sentiment is likely overly bullish given what could unfold in the coming days. For that reason, we will tread carefully but remain on watch for opportunities to tap our shopping list or bring new contenders into the Bullpen.

Samsung delivers a profit miss

As we wait for the June-ending quarter earnings season to hit with full force next week, we and others across Wall Street will be mindful of earnings pre-announcements, good and bad. We have one of the latter ones this morning from Samsung SSNLF, which now sees a 56% drop in its second-quarter 2025 profit due to the combination of inventory value adjustments and the impact of U.S. restrictions on advanced AI chips for China.

While this may raise an eyebrow, Samsung is viewed to be losing share to SK Hynix and Micron MU in high-bandwidth memory (HBM) chips. Recall that for its May quarter, Micron reported a nearly 50% sequential growth in HBM revenue as its data center revenue more than doubled year-over-year, hitting a quarterly record. Micron sees that strength continuing.

Lending support to that outlook, yesterday Foxconn FXCOF said it saw record second-quarter revenue driven by strong demand for AI products and expects its Cloud and Networking segment to continue to benefit from AI products demand and maintain a strong growth trend in the current quarter. We see those comments as very supportive of our positions in Nvidia NVDA, Marvell MRVL, Eaton ETN and others in the Portfolio.

The Pro Portfolio is long NVDA, MRVL and ETN.