All Signs So Far Point to Softening Jobs Market

ADP and Manufacturing PMI reports tell us why margins will be a key topic in the upcoming quarter earnings season.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The September Employment Change report from ADP confirms that the jobs market weakened further. Meanwhile, the September Manufacturing PMI reports from both S&P Global and ISM, pointed to a slowdown in that part of the economy -- the section responsible for 10%-15% of gross domestic product. The takeaway: Job growth is contracting and inflation pressures are still on the rise, but a tad slower than the last few months.

Driving those inflation pressures are tariffs. New order growth for this part of the economy also softened, and coupled with growing competitive pressures, that weighed on company pricing power. But companies are having a tougher time passing on those rising costs. Per S&P Global’s findings:

“Regarding manufacturers’ own selling prices, these rose at a noticeably slower pace in September as competitive pressures and slower demand growth weighed on company pricing power. Although still rising at a historically strong pace, output price inflation softened in September to its lowest level since January.”

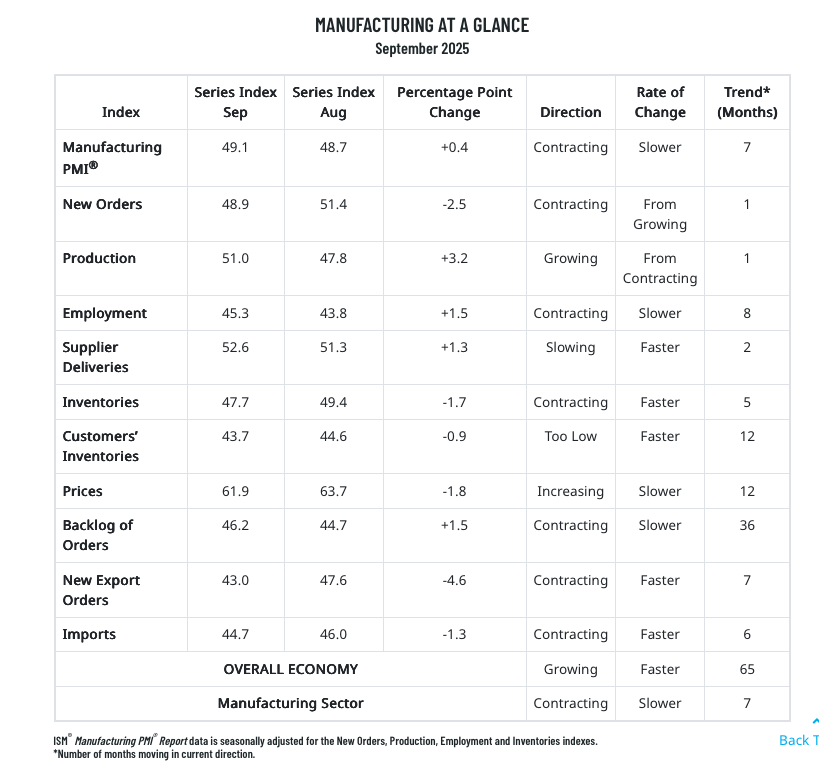

How We See It

It’s pretty clear in the above table from ISM that the manufacturing economy is slowing, and based on new order data, it will likely start the current quarter off on an even softer footing. The findings on the jobs front from both Manufacturing PMI reports will back up the employment contraction found in ADP’s data from this morning.

At a minimum, that combo will lift expectations for an additional quarter-percentage point rate cut by the Fed later this month. Tempering the call for the Fed to do more later this month, at least until we see the findings of the September Service PMI reports on Friday, are ongoing inflation pressures.

Reading between the trends in input and output prices, margins, and corporate guidance for them will not be a minor issue in the quickly approaching September-quarter earnings season. As we game things out, subject to the duration of the government shutdown and what it means for consumer spending and other sectors, those margin pressures may take a greater toll on certain companies that could be an impediment to consensus earnings per share expectations for the second half of 2025.

More reason for us to be selective with the Portfolio, and continue to follow where companies, consumers, and other entities are spending and heed the multitude of signals we continue to collect. We will also heed what we see in Friday’s September Service PMI reports, especially since it captures what is unfolding in a much wider part of the economy.

At the time of publication, the Pro Portfolio had no position in any security mentioned.