All Eyes Back on AI Trade as Shutdown Showdown Ends ... For Now

Let's map out the reopening and where we're going in the great AI adoption trade.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Before we get started today, let’s take a moment to remember our veterans and the freedoms they safeguarded.

The deal to reopen the government is a welcome event. The measure would keep most of the government open through Jan. 30 and some agencies through Sept. 30. It would also pay all federal workers who were denied a check during the government's closure and forbid any federal layoffs through Jan. 30. We would characterize this as a good development, not a great one, as it kicks the can down the road by just a few months.

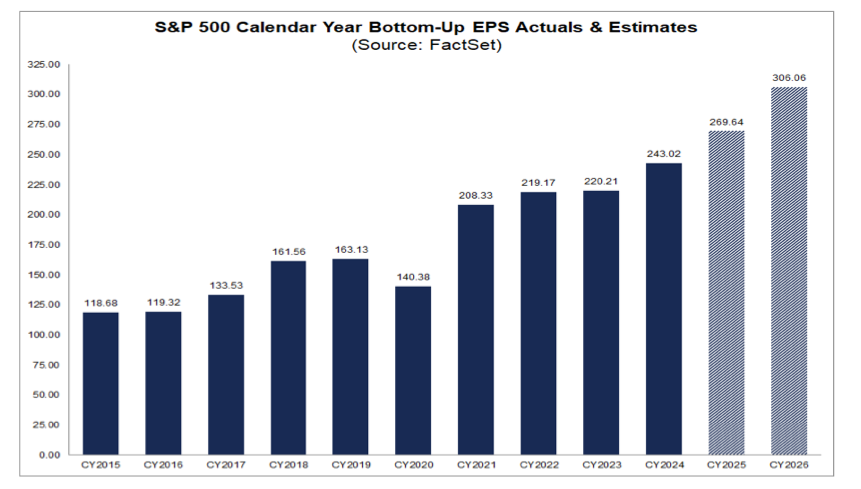

Now, the holidays are coming soon, but the shutdown could be back in focus come January, when companies report their December-ending quarter results and issue their outlook for 2026. Per data from FactSet, the market sees annual earnings per share growth of more than 13% next year, up from around 11% in 2025.

Peering into that by the 11-sector categories used by S&P, we find the strongest level of such growth for the Info Technology sector. That’s the one that houses Nvidia (NVDA) , Apple (AAPL) , Microsoft (MSFT) , Broadcom (AVGO) , Oracle (ORCL) , AMD (AMD) , Cisco (CSCO) , Salesforce (CRM) , and others tagged as part of the “AI trade”. The consensus data tabulated by FactSet shows the Info Technology sector is expected to grow its 2026 earnings per share by 22.8%, up from 21.2% on Sept. 30, and 17.5% at the end of March. That, along with the percentage those stocks comprise of the S&P 500 and the Nasdaq Composite, goes a long way to explaining why folks are focused on what has been labeled the “AI trade.”

AI adoption is being seen across companies, consumers, and other entities. Over the weekend, we told you a signal captured from consulting firm McKinsey that gives us a pretty good sense that while we are not in the very early innings of AI adoption, it is far from slowing down:

Our latest survey shows a larger share of respondents reporting AI use by their organizations, though most have yet to scale the technologies. The share of respondents saying their organizations are using AI in at least one business function has increased since our research last year: 88 percent report regular AI use in at least one business function, compared with 78 percent a year ago. But at the enterprise level, the majority are still in the experimenting or piloting stages, with approximately one-third reporting that their companies have begun to scale their AI programs.

While we concede the intercompany relationships that are being called a “money shuffle” between the likes of OpenAI, Nvidia, and Oracle are something to keep a watchful eye on, it’s the adoption and expanded usage of AI that should be in focus. As we’ve seen before, rising adoption and usage drives initial demand, and as that demand increases, the infrastructure to support it becomes capacity-constrained, resulting in rising capital levels to address such bottlenecks. It’s when that adoption and usage rate plateaus that we see the risk of excess capacity become a concern.

That is why we are closely watching AI adoption and usage metrics. Sticking with the often-used baseball analogy, those figures we are still in the relatively early innings of AI adoption and usage, call it the 3rd or maybe at most the 4th inning. Now, we want to watch for the 7th or 8th innings of AI adoption, when we start to see the incremental adoption rate begin to slow.

Against that, we’ll measure backlog levels from the likes of Eaton (ETN) , Arista Networks (ANET) , and others, including CoreWeave (CRWV) , which hit $55.6 billion exiting the September quarter vs. the $1.4 billion in revenue posted for the September 2025 quarter and the $12.23 billion consensus for 2026.

Those companies and others, including chip companies like our own Nvidia and Marvell (MRVL) , are benefiting from the digital infrastructure buildout to support AI, but also the continued shift to streaming and digital advertising, as well as internet adoption across the globe.

Earlier this year, data from Nielsen showed that U.S. streaming topped cable and broadcast TV consumption for the first time, accounting for 44.8% of total TV consumed during May 2025. The latest data from Nielsen’s The Gauge puts that figure at 45.2% for September, which tells us there is more market share for streaming to eat. And that’s only in the U.S.

When we look at global digital advertising, data from Statista puts it at 70% of global ad investments, up from around 50% in 2025, and expectations are that by 2029, it will account for around 80% of total ad spend.

Tallying those figures suggests those tailwinds have more room to go as well. Putting it all together, we continue to see further gains ahead as those adoption figures climb further. And while we reap those benefits, given the famed quote by former Intel (INTC) CEO Andy Grove that “only the paranoid survive,” we will continue to follow adoption and usage metrics, watching to see when those growth rates start to slow and then stall.

The Pro Portfolio is long NVIDA, INTC, MRVL, CRWV, ANET, AAPL, MSFT, ORCL, EATN, AMD, CRM, CSCO.