ADP’s Big June Jobs Miss to Spur More Calls for Rate Cut

Now let's brace for June jobs report and ISM’s services data for more clues about possible Fed action; Also employment woes could be tailwind for Amazon, Costco and TJX.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Coming into this week, we knew June employment data and hints about inflation ahead of the consumer price index and producer price index reports would be a big focus. The market, after all, would love to see the Fed start delivering on rate cuts. So far it appears that September could be when the Fed makes its next rate cut, but the probability for such action would hinge on June, July, and August data.

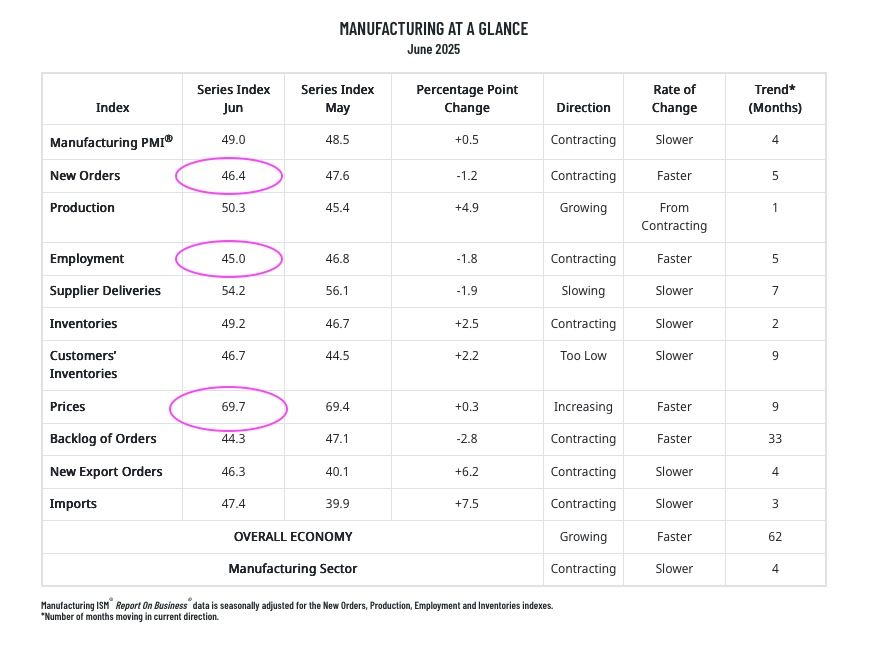

Yesterday, we discussed the first part of that data stream, ISM’s June Manufacturing PMI, and how it showed further weakness in job creation but also inflation pressure moving higher than the market expected. To that, we can add this morning’s surprising miss for ADP’s June Employment Report, which showed 33,000 jobs were lost, well below the expected rebound to 90,000 from May’s disappointing revised figure of 29,000 jobs.

Not only is this another miss in ADP’s data, but add in the “contracting, faster” jobs comment found in ISM’s June Manufacturing PMI, and the market is going to take notice. To be fair, the correlation between ADP’s monthly jobs report and the Labor Department’s monthly employment report is not the best. In addition to the June employment report tomorrow morning, we’ll also get the Challenger Job Cuts report for June and the June ISM Services PMI data.

Aggregating all of those reports will give us a much better sense of how the jobs market fared in June. In addition to judging that figure on its own, we’ll also want to consider its vector and velocity.

To the extent that aggregate data points to June job losses, the more likely we’re going to see folks ramp up calls for the Fed to start cutting rates. Because of the inflation data figures so far for June, odds are the Fed isn’t inclined to cut rates sooner than expected unless we see pain in the jobs market.

If, however, the aggregate June jobs data is one of net job growth, even if it is more modest than the 105,000 jobs expected to be shown in the June employment report, we should expect Fed heads making the rounds to reiterate the need to see more data to gauge the fuller impact of Trump’s tariffs.

Remember, too, a few quarters ago, Fed Chair Powell warned there could be some pain involved to get inflation back to the Fed’s 2% target. While a slower but still growing jobs market may feel like pain, net job losses are more likely the kind of pain that could lead the Fed to reconsider how restrictive it keeps monetary policy.

That means we could be in for the latest iteration of “bad news is good news” for the market. Whether that is the case will hinge on what we see in tomorrow’s data.

What we can say is that a slower-growing jobs market is likely to keep consumers selective in their spending, and it may even lead more than some to tighten their belts a bit further. That is likely to be a helpful tailwind for Amazon’s AMZN upcoming four-day 2025 Prime Day event next week, as well as our shares of Costco COST and the portfolio’s newest holding, TJX Companies TJX.

We would also share that following the market’s extended rally and overbought status coming into this week, today’s data and potentially tomorrow's could very well bring volatility back into the market. Even after our TJX trade yesterday, the Portfolio has more than 12% of its assets in cash – a nice buffer but also firepower to, depending on what we see, be opportunistic.

The Pro Portfolio is long AMZN, TJX and COST.