Absent the September Jobs Report, the Market Will Lean on These Numbers

New reports Friday could shape Fed rate-cut expectations as the ongoing government shutdown limits new data.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

As we get ready to close out the week, the government shutdown continues, and expectations for it to last longer than the average of eight days are growing. Prediction market Kalshi sees the shutdown lasting 14.4 days, up from 12.9 days on Thursday, while Polymarket sees the odds of the shutdown lasting between 10 and 29 days at 61%. Odds of more than 30 days were at 19%.

Could we see some weekend progress that could end the shutdown?

Possibly, and that means we’ll be following the developments and most likely tuning into a few of the Sunday morning talk shows.

We continue to watch for those “massive layoffs” the Trump administration has been bandying about to see if they occur, and if so, assess the implications to consumer spending and other parts of the economy. As we discussed yesterday, it’s that potential announcement that is keeping us in the wings with Costco (COST) and Dutch Bros (BROS) shares. If you missed that discussion, you can find it here alongside the big gains we booked by taking some Marvell (MRVL) shares off the board.

Another reason for our waiting to see what unfolds is the simple fact that the Nasdaq Composite is back in an overbought condition, and the S&P 500 is quickly approaching one. While the Volatility Index (VIX) isn’t screaming complacency, when paired with those respective RSI levels for the Nasdaq and S&P 500, its level indicates caution is warranted.

No September Employment Report Means Greater September Service PMI Focus

Due to the government closure, we will be without the September nonfarm payrolls report today, and, as you know, the data it would have presented would have been instrumental in assessing the labor market. We (and the Fed) will have to make due with the data we do get, and that means today’s September Service PMI reports will be scrutinized more than usual for what they reveal about job creation and inflation in September.

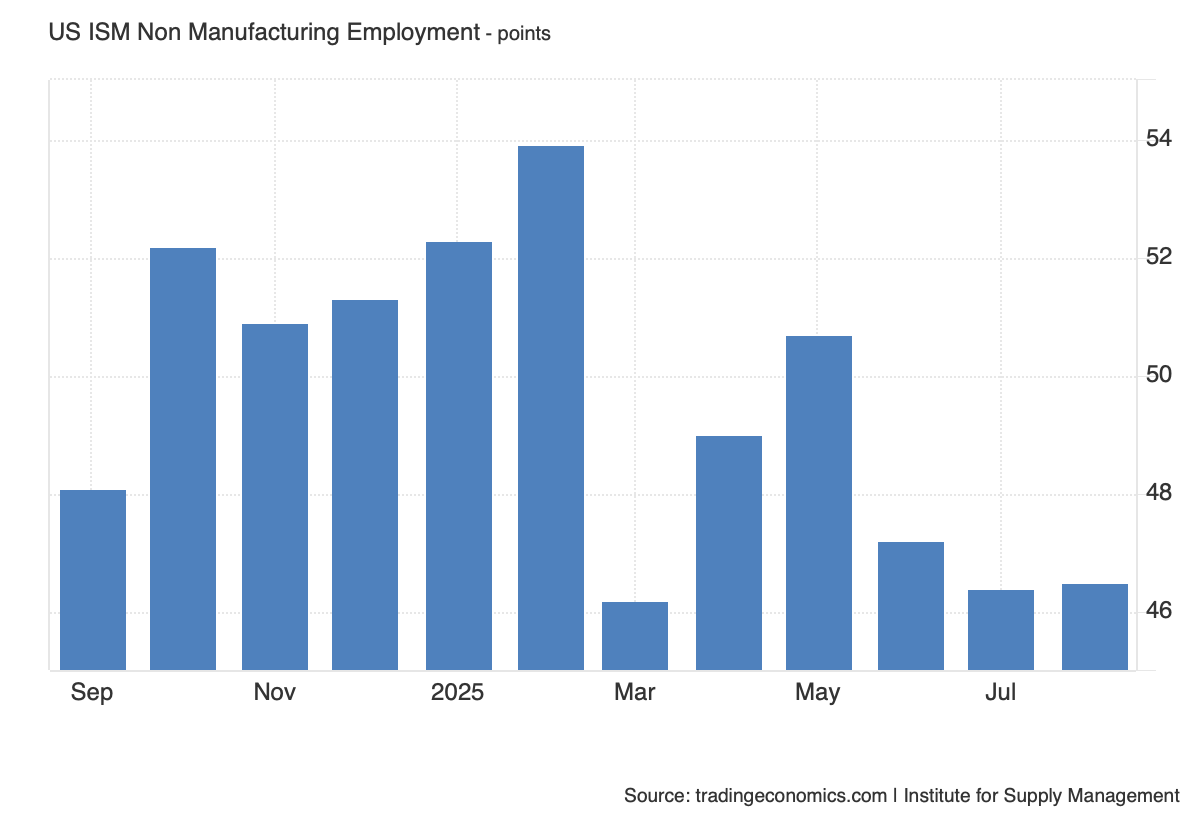

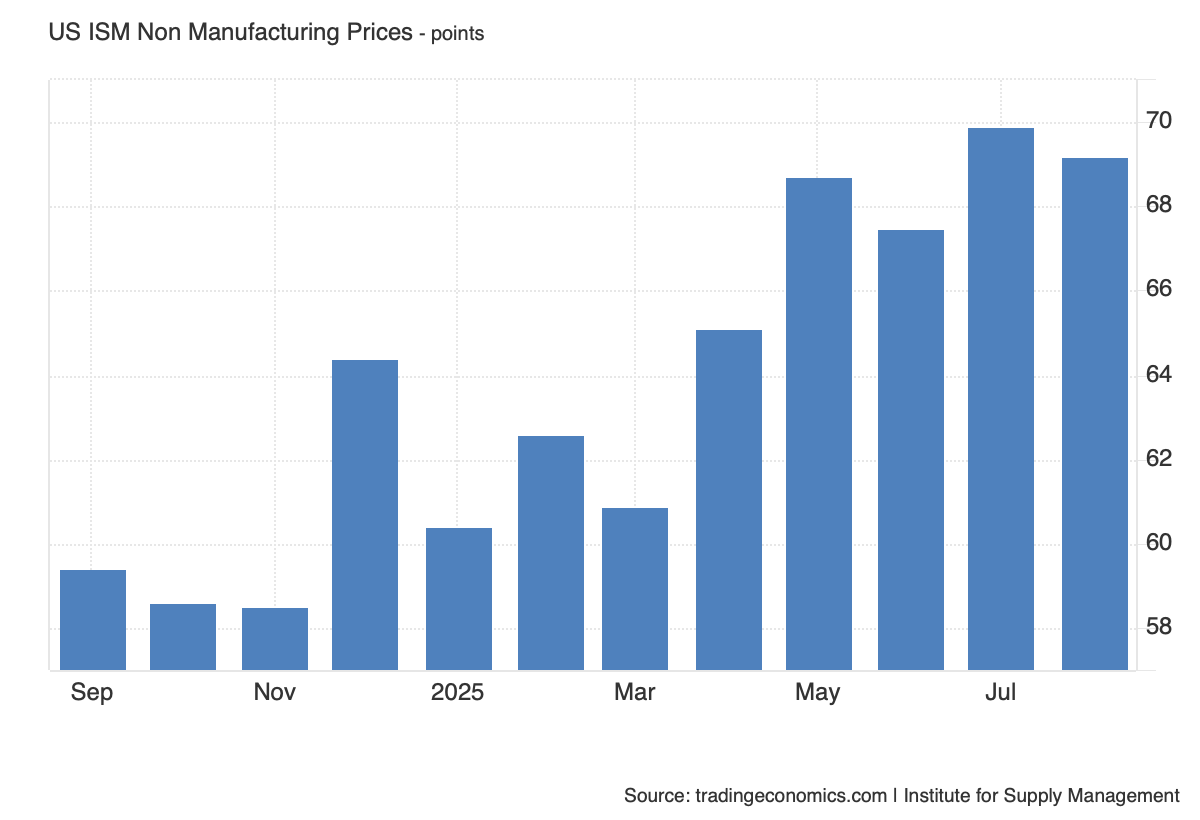

As we get ready for those numbers, here are the recent employment and pricing data from ISM for the Services part of the economy. As you look at those charts, remember the expansion/contraction line at 50, which means the larger a figure is above 50, the faster the rate of expansion. Similarly, the further below 50, the quicker the pace of contraction.

The last few months of Services PMI Non-Manufacturing Employment data echo the recent weakness in the overall employment market captured by recent monthly Employment Reports. If we see the September Non-Manufacturing Employment figure fall meaningfully from the August figure of 46.5, paired with the job losses reported by ADP earlier this week, that could lift market expectations for rate cuts.

What today’s data say about inflation pressure in the Services side of the economy, which accounts for 85%-90% of overall GDP, could temper such a call if the September figures are largely in line with those from the last few months.

S&P Global’s September Services PMI report is out at 9:45 AM ET and will be quickly followed by ISM’s at 10 AM ET. Let’s see what they have to say and go from there.

At the time of publication, TheStreet Pro Portfolio was long COST and BROS.