6 Charts Show We Could Be in for a Rude Energy Price Awakening

The longer the U.S.-Iran conflict lasts, the greater the mismatch between these two market sectors will become.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Oil Prices Drill Down Energy Sector, Not Jobs Report

Oil Prices Drill Down Energy Sector, Not Jobs Report

In my opening comments on Monday, I noted that, with the U.S.-Iran war entering its third week, we haven’t really seen any major revisions to consensus EPS expectations for the S&P 500 or some of its sectors for 1H 2026.

Some in the Wall Street community may be taking a wait-and-see approach when it comes to the duration of conflict, but at least for now it appears it is poised to continue. We say that based on fresh attacks by Iran across the Persian Gulf, which are disrupting UAE shipments from a key oil hub, and the denial that it is seeking ceasefire talks.

Other reports indicate some vessels are getting through the Strait of Hormuz, but they also indicate that U.S. allies have deflected President Trump’s demands to help reopen the strait, lest they get pulled into the war in Iran.

With Trump planning to hold a press conference later on Monday, odds are that the topic of Iran will come up one way or another.

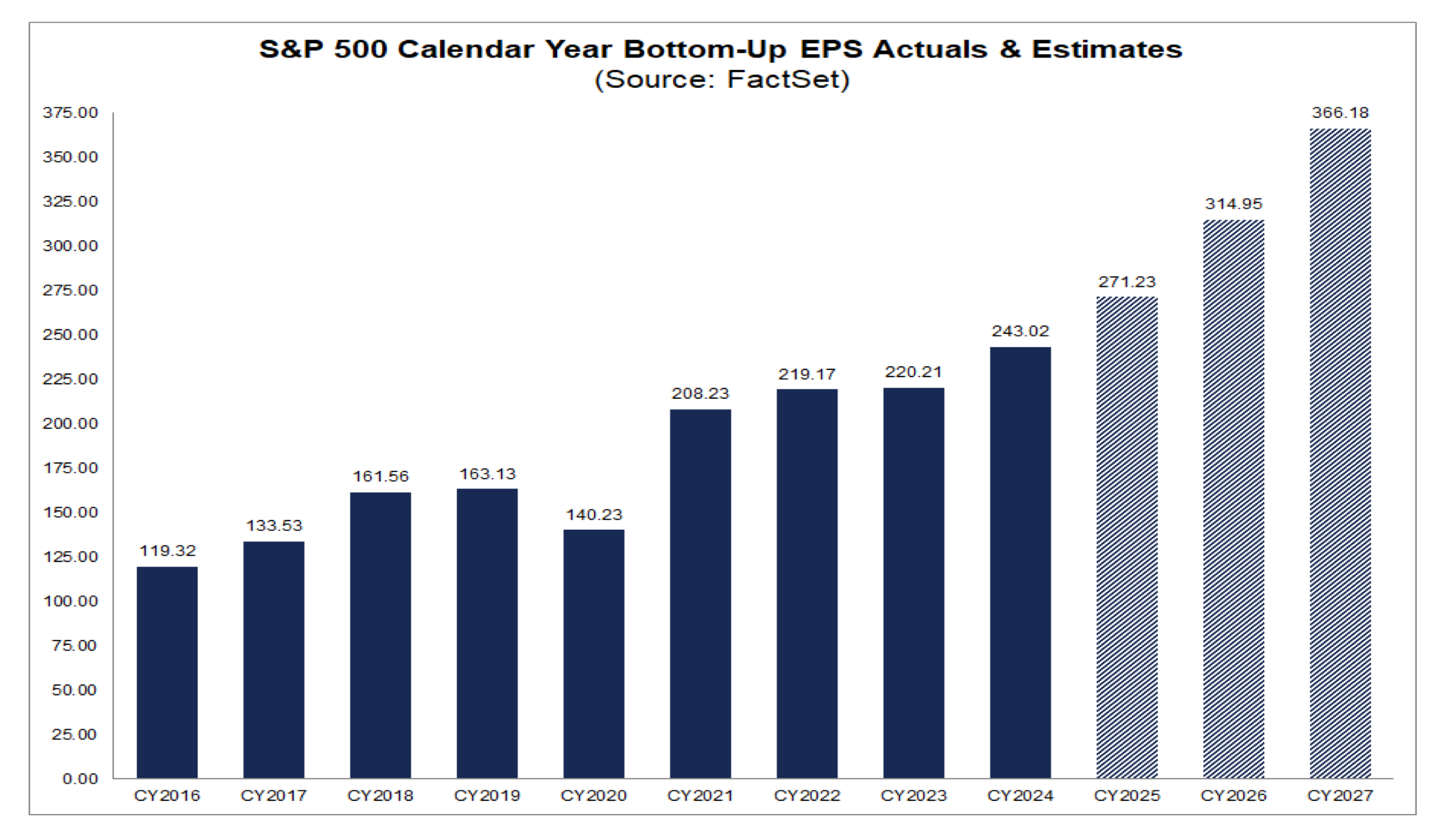

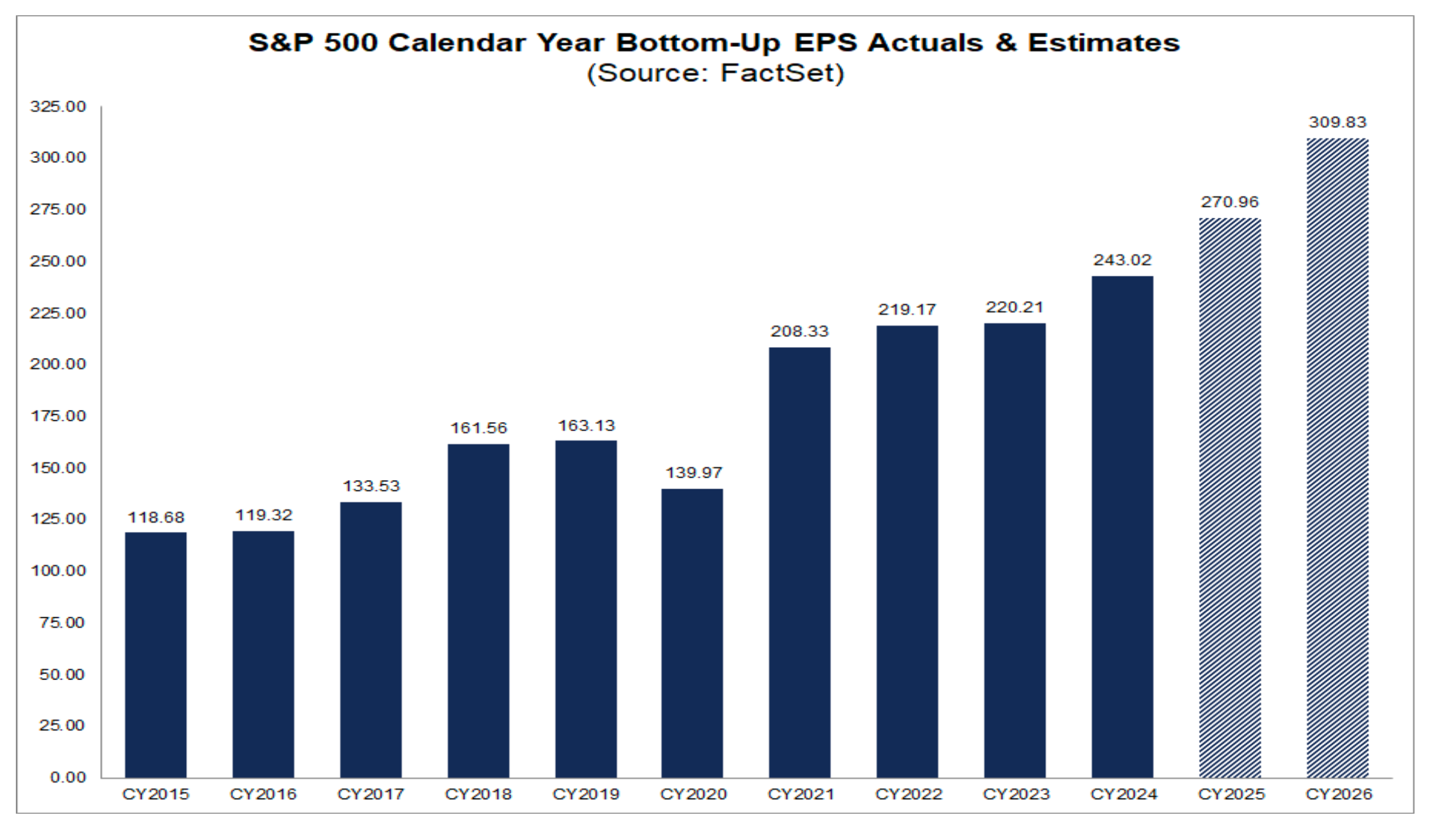

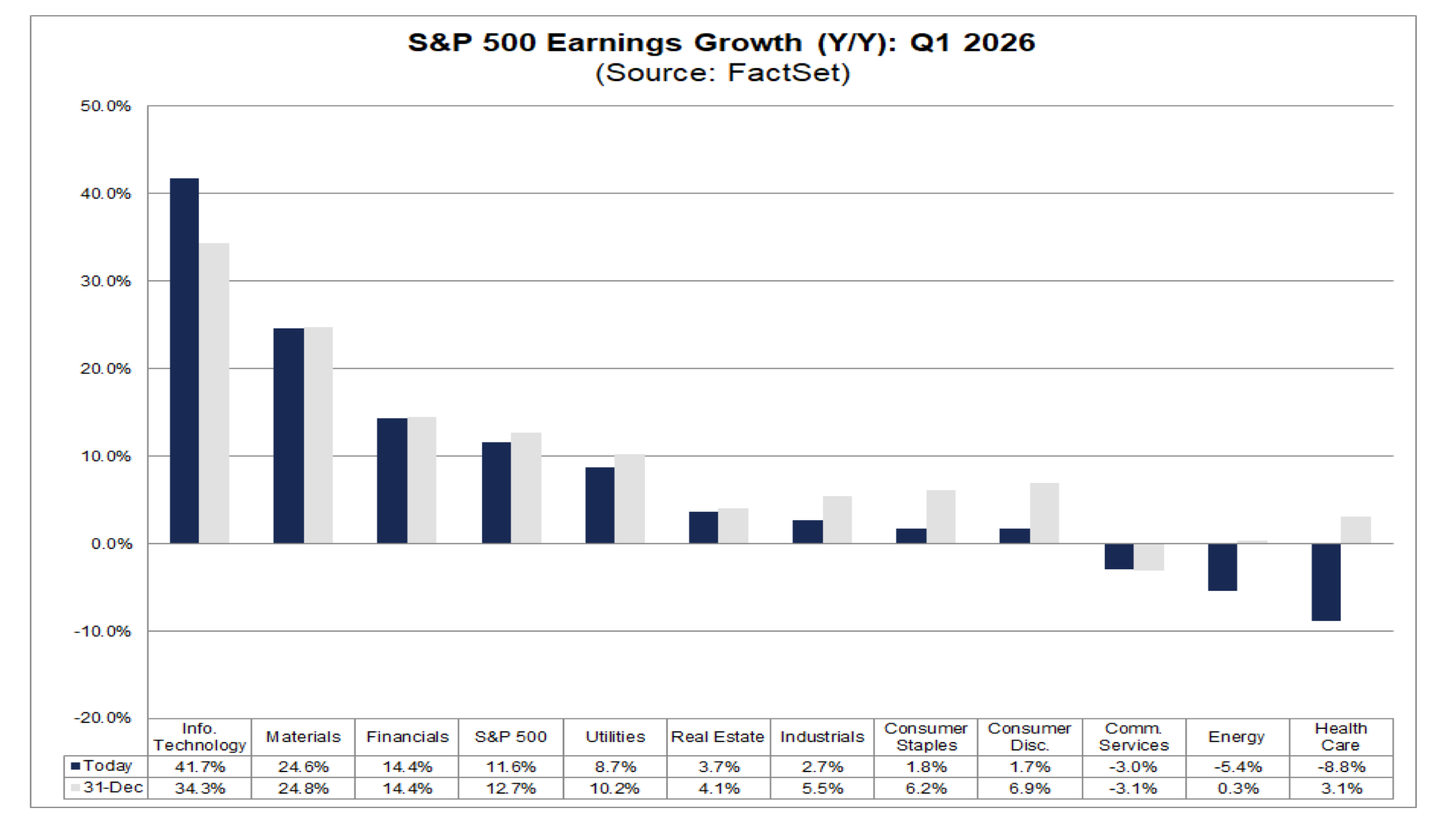

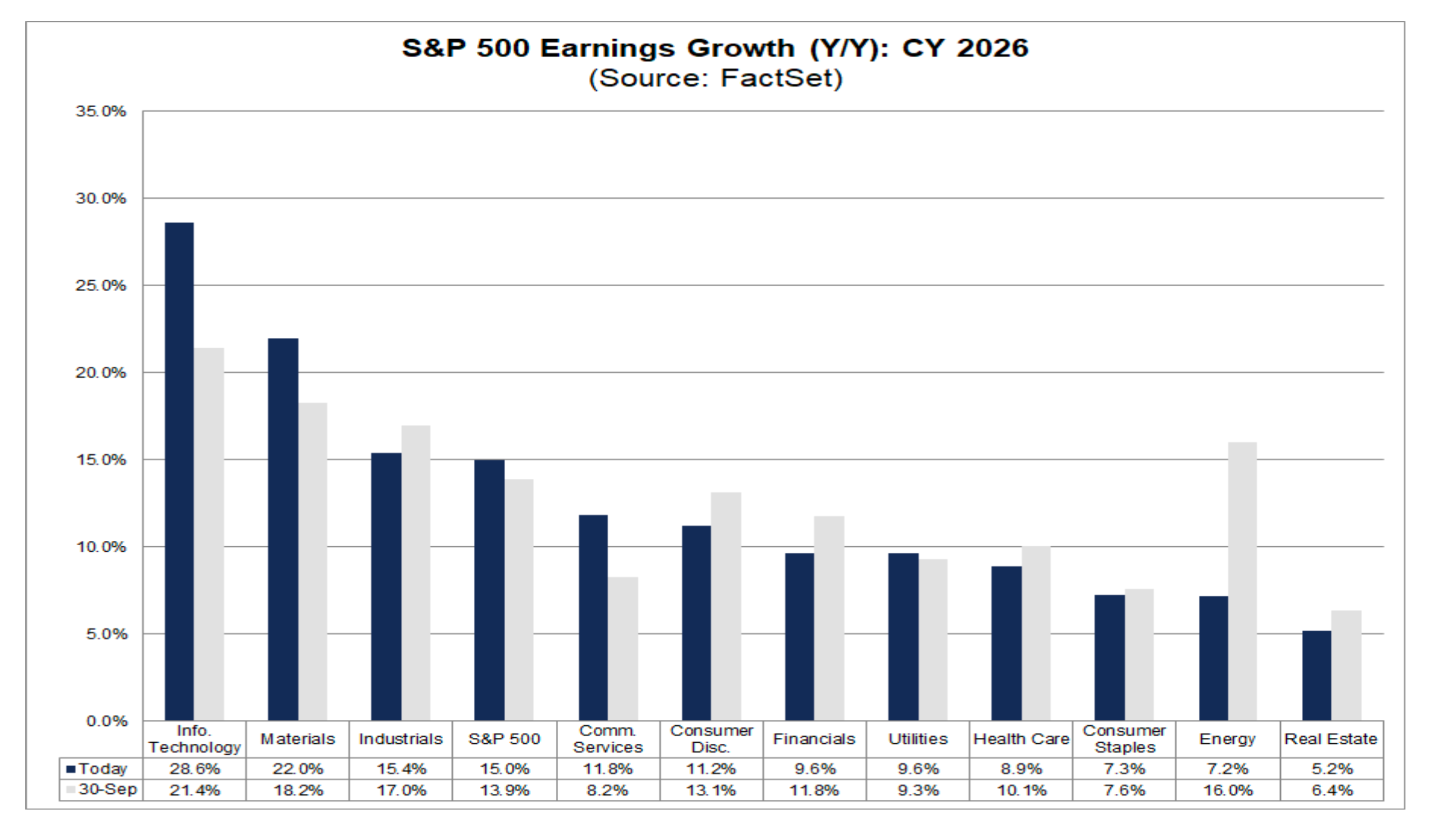

Getting back to consensus EPS expectations, as we can see in the two charts below, the consensus EPS figure for 2026 has moved up to $314.95 as of March 12, up from $309.83 in late December. What that means is EPS growth expectations have moved up to about 16% year over year in 2026 compared to just over 14% exiting 2025 and about 13.5% in September.

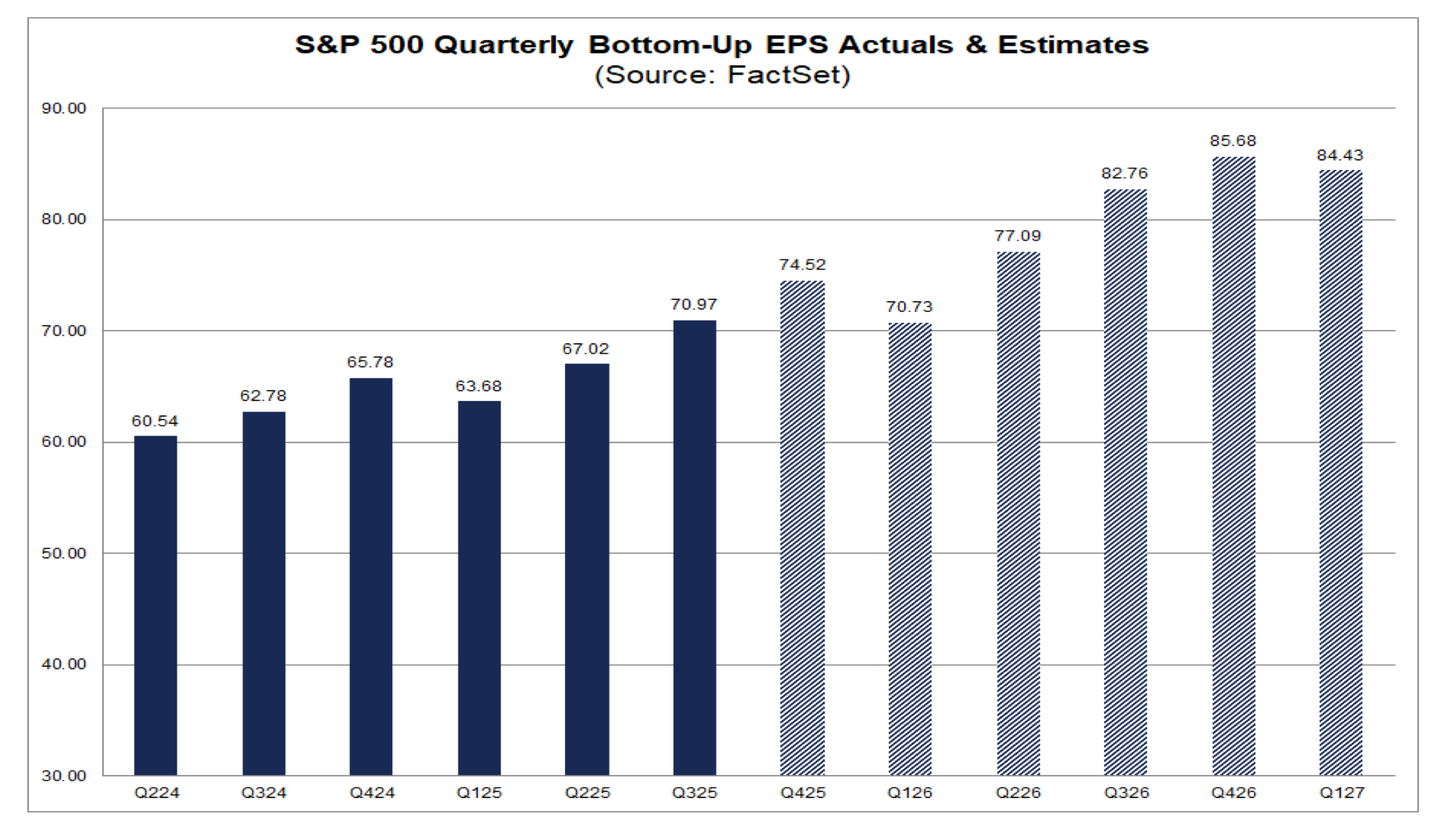

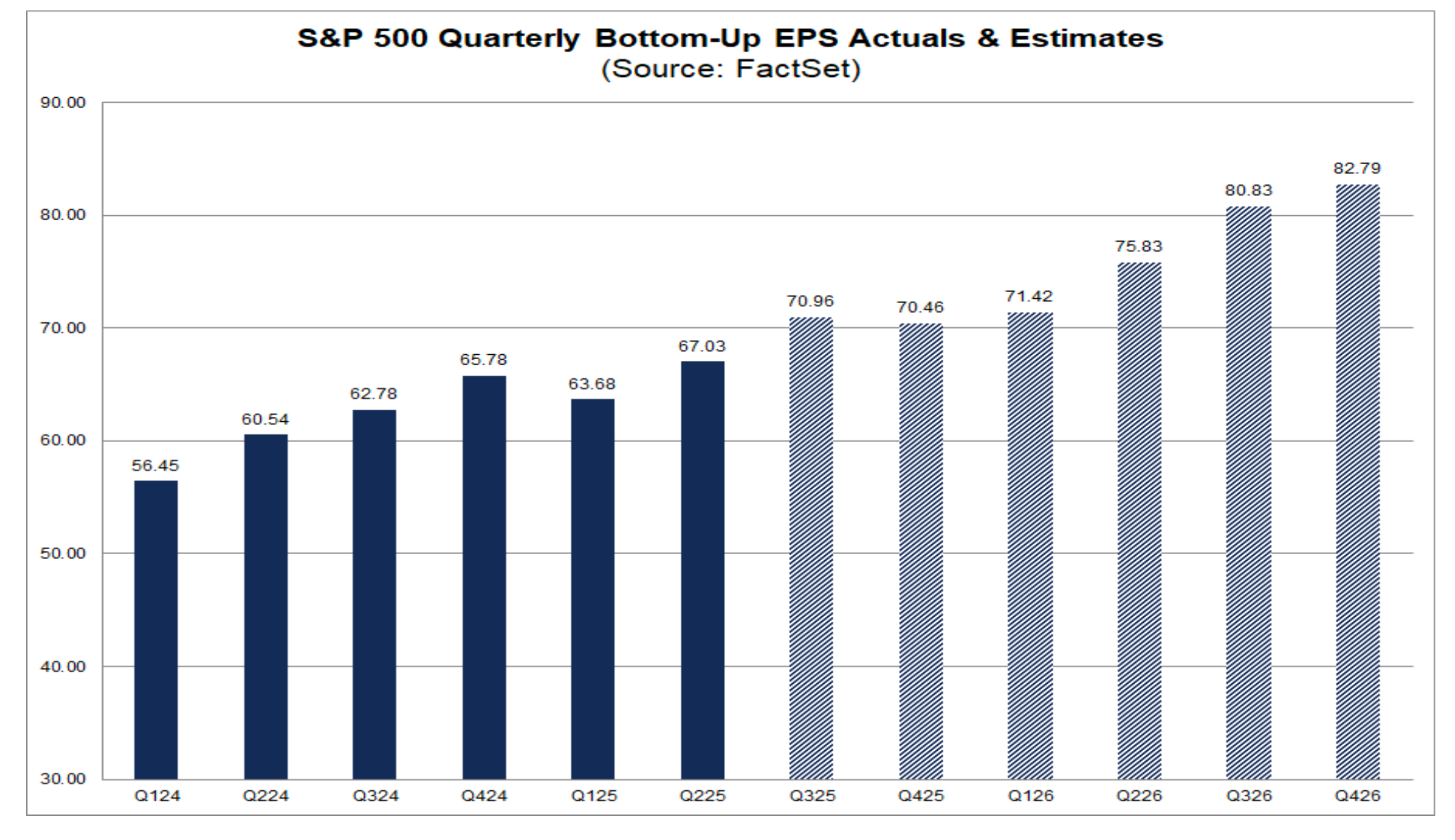

Examining the quarterly breakdown of those consensus figures, we can see the one for Q1 2026 was revised lower to $70.73 as of last week, down from $71.42 in late December. That was offset in part by the step up in consensus EPS expectations for Q2 2026, which was lifted to $77.09 from $75.83 near the end of 2025.

Putting those figures together, the S&P 500 is now expected to deliver 1H 2026 EPS of $147.82, up 13% from the $130.70 posted in 1H 2025. While some will point to the anniversary-ing of tariffs that's on the horizon, let’s also remember the step up in Trump’s global tariff to 15% started two weeks ago.

Looking at those figures, it’s also logical to say the impact of higher oil and gas prices has yet to make its way into those consensus EPS figures.

Turning to the S&P 500 sectors, we find consensus EPS expectations have grown considerably for the Info Technology sector (+33.5% year over year in 2026 versus +21.4% back in September) and upsized for the Materials sector. We’re well-positioned for that move in Info Tech, while our gold and silver exposure in the EPS Diplomats gives us some Materials exposure.

Consumer Discretionary continued to inch down quarter to date, but when we contrast that with the continued fall in EPS expectations for the Energy sector, it tells us the dots have yet to be connected, given the moves we and others have discussed in that part of the market over the last few weeks.

Cue our word for Q1 2026: duration. The longer the conflict goes on, the longer the Strait of Hormuz is bottlenecked and the longer it takes for oil producers to ramp up idled capacity, the greater the risk to consensus EPS expectations, especially for Consumer Discretionary companies.

Related: Former Intel Operatives Say Middle East Conflict Is Shifting Beyond Oil