4 Changes in the Fed’s New Projections, Including a Rate Hike Forecast

The bulk of these changes were expected, except for one.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

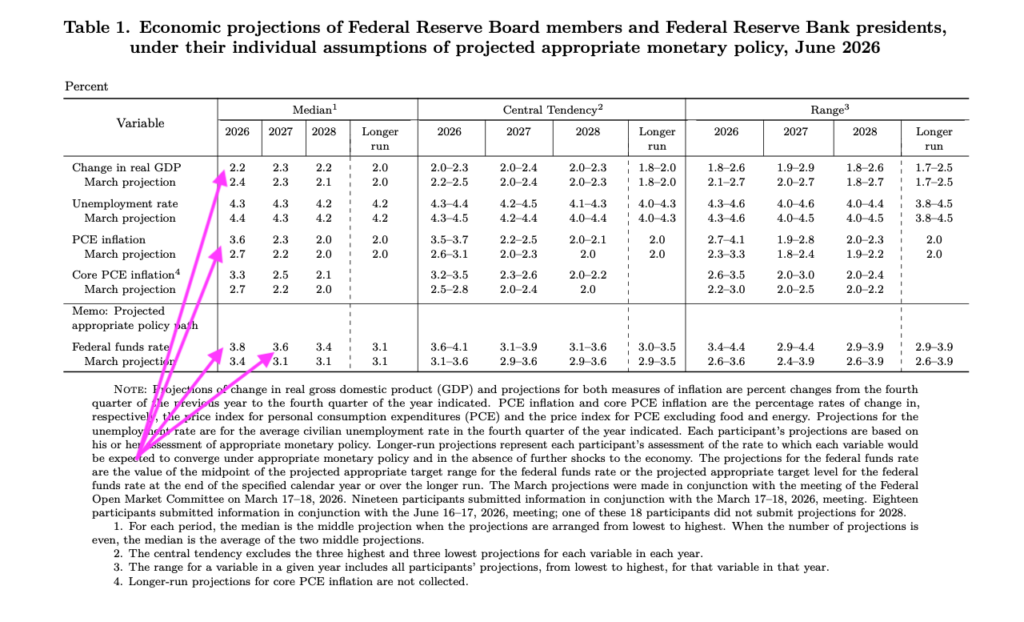

We have the Federal Reserve’s policy decision in hand, and as was widely expected, the Federal Open Market Committee made no changes to the federal funds rate. However, in looking at the updated Set of Economic Projections (SEP), we see a few changes for 2026 and 2027 compared to the March set of projections:

First, the fed funds rate indicates the expectation of a rate hike before the end of 2027. The good news on that front is that is what the market has been expecting, per the CME FedWatch Tool given renewed inflation pressures. Also, in line with the market’s thinking, the fed funds rate in 2027 will decline by one 25 basis-point cut. Timing on that will be TBD but let’s also remember these are annual expectations that are not tied to any one Fed policy meeting. And as we’ve seen many times before, the SEP as well as market expectations will change based on incoming data.

That change in fed funds rate projections reflects the second item we’ll point out, which is the jump in the Fed’s PCE and Core PCE inflation figure for 2026. The 2027 outlook shows a sharp ramp down in PCE inflation, which more than likely reflects the end of the U.S.-Iran war, return to normalized oil production levels and the winding down of supply chain issues associated with the Strait of Hormuz.

The other surprise given recent economic data, especially the latest batch of monthly PMI data from ISM, is the dialing down for GDP this year to 2.2% from 2.4% back in March. We’ll listen to Fed Chair Kevin Warsh’s comments on this but based on the recent 1.6% figure for Q1 2026 and the latest 2.7% to 3.0% figures from the NY Fed Nowcast and Atlanta Fed GDPNow models for Q2 2026, it suggests the Fed sees a somewhat slower pace of growth for the domestic economy in 2H 20216.

Finally, when looking the Fed policy statement issued following Wednesday’s policy decision, it is noticeably shorter than the ones the market has become accustomed to. How this translates into the level of insight Warsh is willing to share on the decision, what it would take to deliver a rate hike, and other thoughts on the economy, inflation and job creation will become clear in Wednesday afternoon’s presser.

We’ll be back with more comments once that event is over.