You Win Some (A Lot, Actually), Lose Some

Some of my favorite stocks got hit hard after giving me a great run. Now let's tackle the Fed chatter, chart the market, and prep for big earnings, including Nvidia.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

By week's end, the numbers weren't awful. That said, some of the stocks I most trade, and invest in and write about, were indeed taken out to the woodshed, at least on Thursday. Friday offered some support to those names, but nothing all that notable in the way of a rebound.

For those readers who feel the need to send anger-fueled hate-mail my way when stocks that I trade often are trading sharply lower, it must be tough. You didn't hear from me, because I am off from work for a family event, and because I do not run a daily blog.

But ... it's funny, I don't hear from those who sent hate mail when these same stocks go up 400%, 500% and 2,700% in share price. And traders should know that these high-beta growth stocks are a double-edged sword: They are by their very nature, high risk/ high reward propositions and they are not for everyone. It is imperative that all who enter the arena know their own tolerance for risk, both from a financial and personal ability perspective. You are responsible for your own trades.

Now? Better get ready, Nvidia (NVDA) reports this Wednesday.

The Deal

There were some positives last week. In fact, equity markets held their own, even rallying early on in the five-day period. The 43-day shutdown of the federal government finally came to an end, though the threat of another shutdown does loom as soon as late January. Pres. Trump signed orders exempting a number of agricultural products from reciprocal tariffs and another trade deal was announced, this time with Switzerland.

Unfortunately, for the net long crowd, a series of Fed officials spoke publicly last week and cast doubt upon the likelihood for a rate cut on Dec. 10. Cleveland Fed Pres. Beth Hammack, who has emerged as the Fed's leading hawk, and will speak again this week, led that charge. Hammack was joined by Atlanta Fed Pres Raphael Bostic and Boston Fed Pres. Susan Collins in sounding less dovish than the markets had priced in. This unleashed a barrage of profit taking activity by keyword-reading algorithms that targeted the AI focused and high-tech trades. This is where the profits are and this is where the extended valuations have been.

The Week That Was...

Last week, or rather last Thursday, was an ugly day. This damaged market-wide performance for the period, but at the headline-level, it was the small- to mid-caps that were hit the hardest. This is how it went...

- The S&P 500 lost just 0.05% on Friday but gained just 0.08% for the week.

- The Nasdaq Composite gained just 0.13% but lost 0.45% for the week.

- The Nasdaq 100 gained just 0.06% on Friday and lost just 0.21% for the week.

- The Russell 2000 gained 0.22% on Friday but took a 1.83% hit for the week.

- The S&P Smallcap 600 lost 0.13% on Friday and 1% for the week.

- The S&P Midcap 400 surrendered 0.26% and a gnarly 1.17% for the week.

- The Dow Transports gave up 0.28% on Friday and 0.84% for the week.

- The Philly Semis surrendered just 0.11% on Friday but hit for 1.96% on the week.

- The KBW Bank Index lost 0.69% on Friday and 0.79% on the week.

On Friday, five of the 11 S&P sector SPDR ETFs closed out the session in the green, easily led by Energy (XLE) . The losers were led by the Financials (XLF) and the Materials (XLB) . For the week, just four of the 11 S&P sector SPDR ETFs traded higher with Health Care (XLV) out in front followed by Energy. The Discretionaries (XLY) were the big losers. Technology (XLK) for all of its obvious troubles last week, closed out the five-day period precisely flat from the week prior.

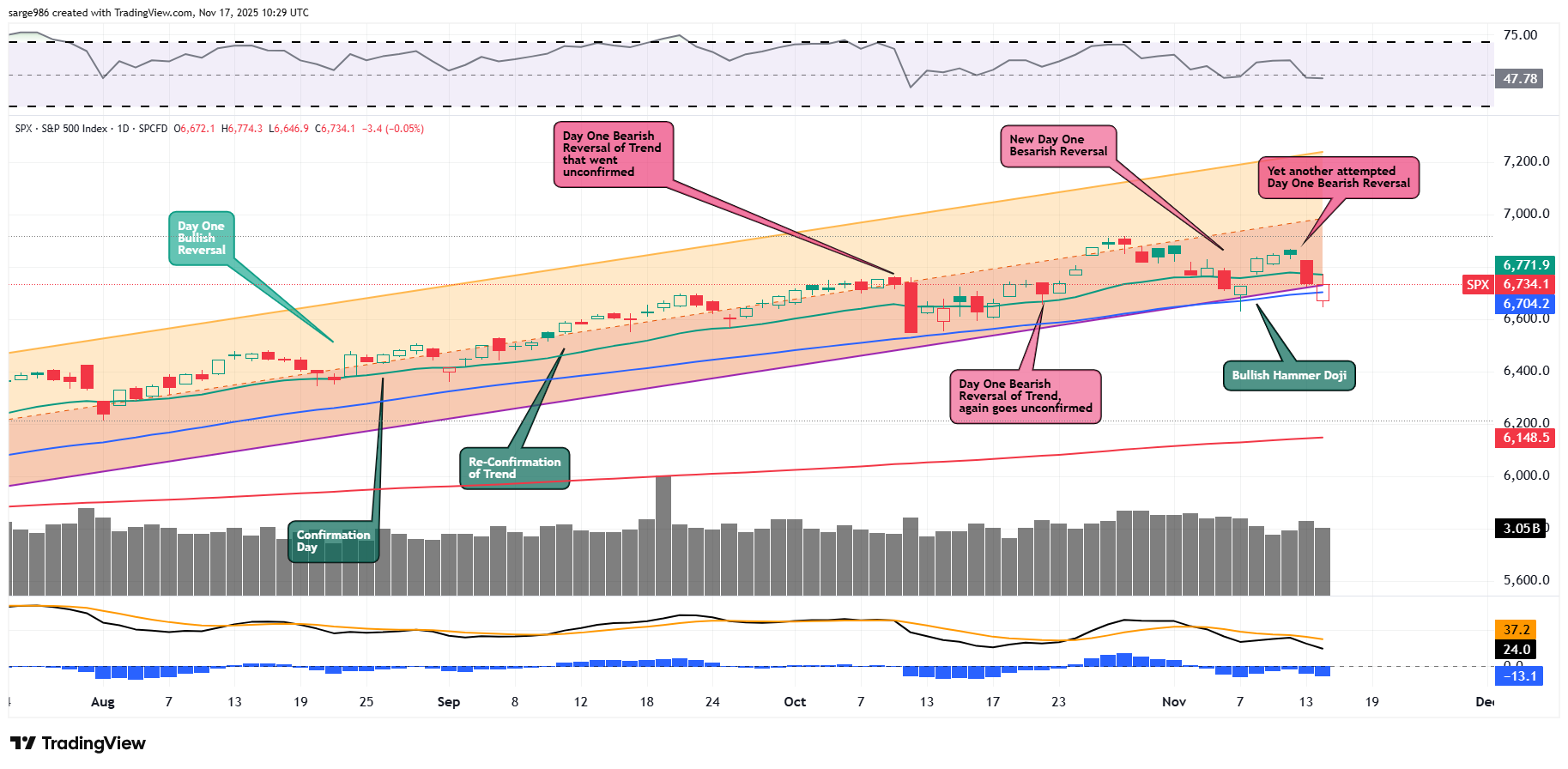

The Chart...

Readers will see that the S&P 500 did indeed put a Day One bearish reversal of trend on higher trading volume to the tape on Thursday. There needs to be a pause of at least one day in between a Day One and a Day of Confirmation. It does appear that for the most part, there was at least the start of a pause on Friday as markets waffled on lower volume. It is still the middle of the night for most people, so hard to take anything away from equity index futures markets right now, but they do seem to be trying to rally.

As far as the indicators are concerned, Relative Strength remains closer to a neutral reading than anything else as it has been since late October. Below the chart, we still have a pretty bearish daily Moving Average Convergence Divergence, which is something I warned about going into last week. The histogram of the 9-day exponential moving average has moved deeper into negative territory, while the 12-day EMA has moved further below the 26-day EMA. While this is a short-term to medium-term bearish set-up, the fact that both the 12-day and 26-day lines remain in positive territory does fly in the face of such negativity.

Earnings

According to FactSet, for the third quarter, with 92% of the S&P 500 having reported, 82% of those companies have pleasantly surprised on earnings (in-line with last week) while 76% of those companies (down from 77%) have surprised in the right direction on revenue generation.

The impressive performance this earnings season and increased guidance in general, has boosted the blend of Q3 earnings results / expectations for the S&P 500 all the way to growth of 13.1% from 10.7% a couple of weeks ago and from just 8% several weeks ago.

Revenue growth expectations now stand at 8.3%, in-line with last week and up from 6.3% several weeks ago. For the full calendar year of 2025, Wall Street now sees S&P 500 earnings growth at 11.7% (up from 11.6%) on revenue growth of 6.8%, which is in line with last week.

Back to the quarter, Technology, the Financials, the Utilities and the Materials have all been outperformers with blended earning growth of 20% or more. Just two sectors are still running at a year over year earnings contraction led to the downside by Communication Services. That Staples have shifted from a net earnings contraction to a very slight gain.

Valuation

Still using data provided by FactSet, aided by still improving forward looking guidance, but damaged by last week's selloff, the S&P 500 ended last week trading at 22.4-times 12 months' forward-looking earnings, down from 22.7-times a week ago and 22.9-times two weeks ago. This is still well above the five-year average of 20.0 times for the index as well as its 10-year average of 18.7 times.

The S&P 500 also ended last week trading at 27.8-times trailing twelve months' earnings, down sharply from 29.0-times a week ago and 29.3-times two weeks ago. That also stands well above the five-year (25.0 times) and ten-year (22.8 times) averages for the index.

Ten of the 11 sectors are still trading above their five-year average valuations, led by Tech (29.4 times, down from 30.4) and the Consumer Discretionaries (28.3%). Only the REITs (17.4 times) are not historically overvalued relative to their five-year averages, even with last week's rotation.

The GDP Game

Last week, the Atlanta Fed actually left their GDPNow model for the third quarter unrevised at growth of 4.0% (q/q, SAAR). Among other regional central bank district branches running close to real-time GDP models, the New York Fed's estimate for Q3 growth was also left unrevised at growth of 2.31%. The Cleveland Fed's model for the third quarter was left unrevised as well at growth of 2.05%. Finally, the St. Louis Fed model remained unrevised at growth of 0.59%.

Obviously, these models have become close to meaningless, at least until the September data states rolling in. Then, we can start looking forward to modeling the fourth quarter, which has undoubtedly sustained serious damage thanks to the government shutdown. To use a Hedgeye term, we very likely are looking forward to some weak-ish "Quad-3" activity through Q4, which for the layfolk would amount to some stagflation.

Will that stagflationary environment be temporary or "transitory?" No, I am not afraid of using that word and yes, I believe it will be. Currently a slowdown in economic activity should not surprise in either very late 2025 or very early 2026. That said, some deflation will follow due to the lower taxes and deregulation promised by the "big, beautiful bill." That will re-accelerate activity. Should there be an unleashing of some kind of package aimed at juicing liquidity early in Q1, which is more possible than you think, inflation may reassert itself, but with that, so will asset prices.

Fed Funds Futures

Fed Funds futures trading in Chicago are now pricing in just a 45% probability for a quarter-point rate on Dec. 10, down from 65%, a week ago. This is what provoked last week's market fragility. At present, there are now three-quarter points worth of additional rate cuts fully priced in (67% chance) for all of calendar 2026. Though the rate cut in early December is now in doubt, that particular cut having been pushed out into January, the projected Fed Funds Rate at the end of 2026 remains unchanged from a week ago.

On The Docket...

There are not a lot of earnings releases scheduled for this week. That said, within the small group expected to report are some real headliners. How much macroeconomic data we see depends on how quickly federal workers, not generally known as a bunch of hard-charging fire-eaters, can get their collective tails in gear.

... The Fed will be out in force once again this week. Right now, I am tracking at least 14 public appearances to be made by Fed officials this week with five of those appearances set for later today (Monday). The headliners would be Fed Gov. Christopher Waller this afternoon and Cleveland Fed Pres Beth Hammack on Friday. New York Fed Pres John Williams, whom I find to be far less than capable in his position, will speak three times this week. The Federal Open Market Committee Minutes of the last policy meeting are due this Wednesday.

.... The macroeconomic calendar could remain light. Underrated though, this will likely change as the week develops. As raw data from September and October becomes available and then salted and peppered to taste, it will be released. There will likely be repetitive data-dumps over the next few weeks. The Bureau of Labor Statistics has already announced that Their Labor Market report for September will cross the tape this Thursday.

..... The earnings calendar will produce some big names this week. On Tuesday, Home Depot (HD) will report in the morning followed by Medtronic (MDT) in the afternoon. Wednesday morning brings numbers from Lowe's (LOW) , Target (TGT) and TJX (TJX) ahead of the opening bell. Nvidia and Palo Alto Networks (PANW) will go to the tape after the close. On Thursday morning, we'll hear from Walmart (WMT) followed later in the day by Intuit (INTU) .

.... Other corporate events include Oracle's (ORCL) annual meeting on Tuesday. Microsoft (MSFT) will also hold its annual conference for IT professionals on Wednesday. CEO Satya Nadella is expected to speak at the event. In addition, Moderna (MRNA) will hold an "Investor Day" on Wednesday.

Economics

(All Times Eastern)

08:30 - Empire State Manufacturing Index (Nov): Expecting 6.1, Last 10.7.

The Fed

(All Times Eastern)

09:00 - Speaker: New York Fed Pres. John Williams.

09:30 - Speaker: Federal Reserve Vice Chair Philip Jefferson.

1:00 p.m. - Speaker: Minneapolis Fed Pres. Neel Kashkari.

3:35 - Speaker: Reserve Board Gov. Christopher Waller.

7:55 - Speaker: Dallas Fed Pres. Lorie Logan.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: ARMK (.54)

After the Close: TCOM (7.98)

At the time of publication, Guilfoyle was long TJX, NVDA, PANW, MSFT equity.