You Are Free to Move About the Cabin, but Watch Out for the Air Pockets

Gaps up and gaps down at the same time that the indicators are making a change.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I have spent a great deal of time lately talking about air pockets in individual stocks. I know I have discussed them mostly on the downside, but I think we’d have to call that massive gap up in Oracle an air pocket as well. May as well throw Alibaba’s move on Wednesday into it.

As I put the pencil to the paper on Wednesday after the close, I saw an air pocket over the last two days in Air Products (APD). I had to stop myself from typing products when I mean pocket and vice versa!

But the air pockets from Wednesday that I want to highlight came in the asset or alternative asset managers. Ares and KKR got smacked on Wednesday. I didn’t even see a real reason, although we can probably think of many. I figure we’ll see some news in the next day or so, and then we can say ‘now we know’, which usually means the news is now priced in.

I know you thought I was going to highlight Freeport McMoRan (FCX) because that, too, had one heck of an air pocket Wednesday.

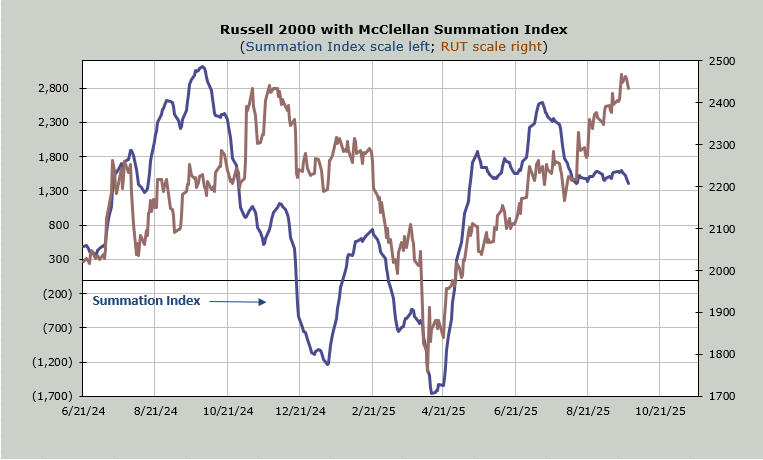

But there was also a little bit of movement in some of the indicators. The McClellan Summation Index turned down a smidge. It now needs a net differential of +1600 advancers minus decliners on the NYSE to halt the decline. So that’s new, and a change from the flat-lining it has done for the last six weeks.

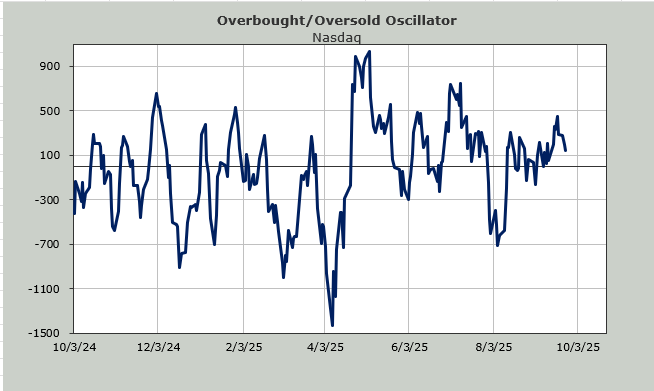

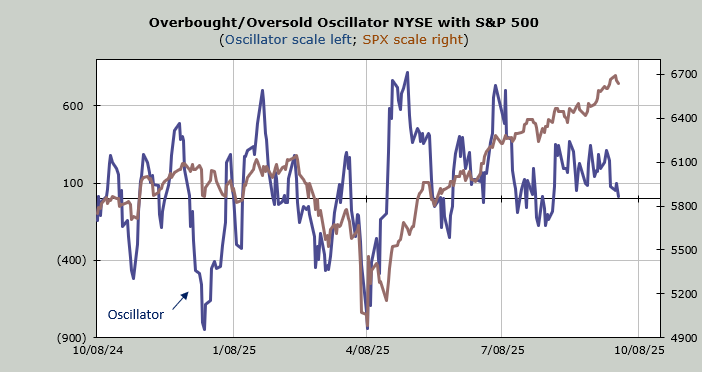

The Overbought/Oversold Oscillator tagged the zero line. What does it say about the market as a whole when this indicator, based on breadth, is at the zero line and the S&P is at the high? I think it tells us the group rotation has kept the S&P going, but there have been very few trends the last few weeks with the exception of the small cap tech names and some—only some—financials.

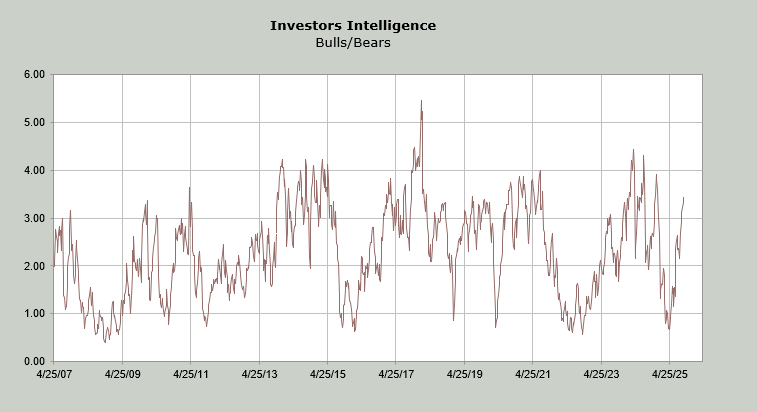

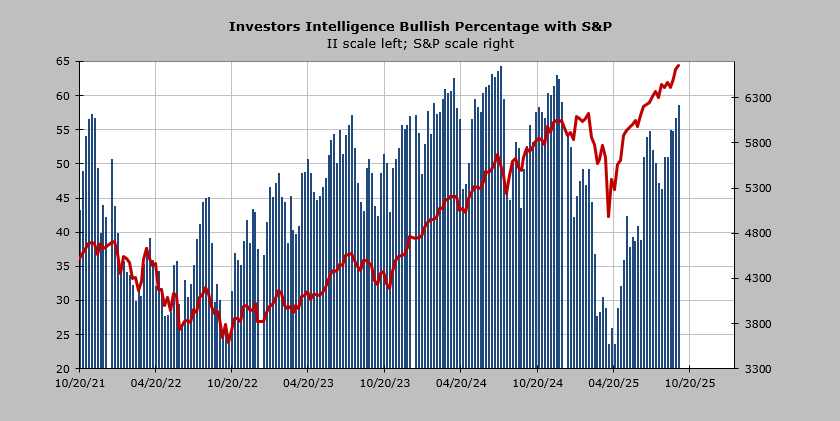

Then there is sentiment. This week’s Investors Intelligence bulls scooted up to 58.5% which is the highest reading since December. The bears remained constant at 17%. That makes the ratio 3.44, which I think leans high. An extreme reading is closer to 4.0. To get to 4.0, the bulls would need to be 60% and the bears 15% (that’s just the math), so we’re knocking on the door.

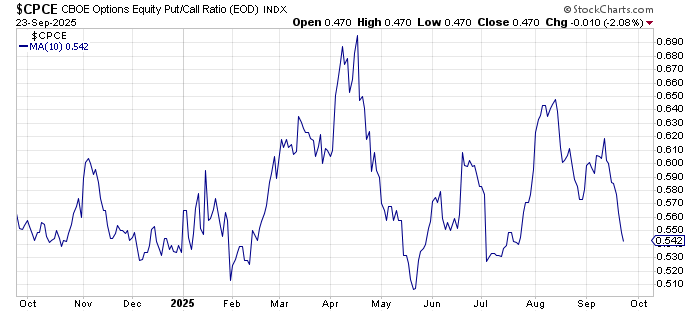

Finally, the equity put/call ratio has been under .50 for three straight days (as of this writing, I do not have Wednesday’s reading). That is the longest streak of sub .50 readings since mid-January. So there has been a marked change in sentiment since the Fed meeting last week.

Despite all of this, there wasn’t much selling in stocks on Wednesday. Most charts just milled around with the exception of the air pockets. And the VIX was red on the day.