With the Yen on the Move, Pay Attention to the Banks

They're over-loved but flat on the year. Here's what could happen.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

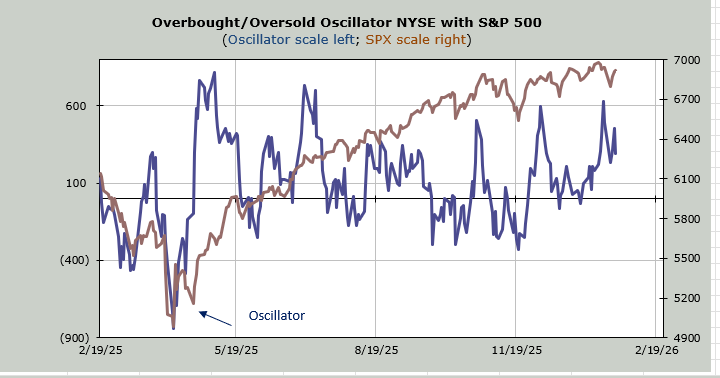

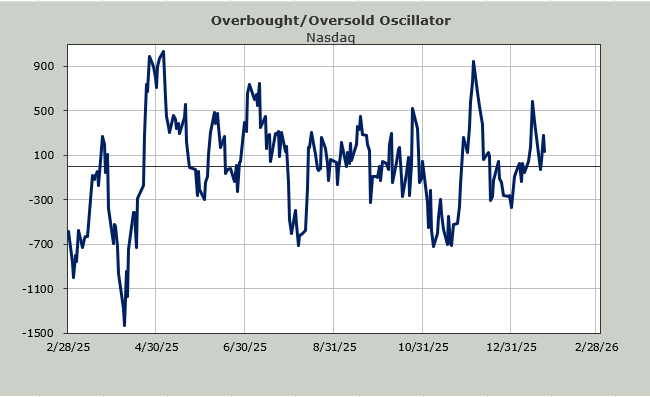

For one week now, I have been of the mind that the market is overbought, and while sentiment is not giddy, it surely is highly complacent. I have not changed my view.

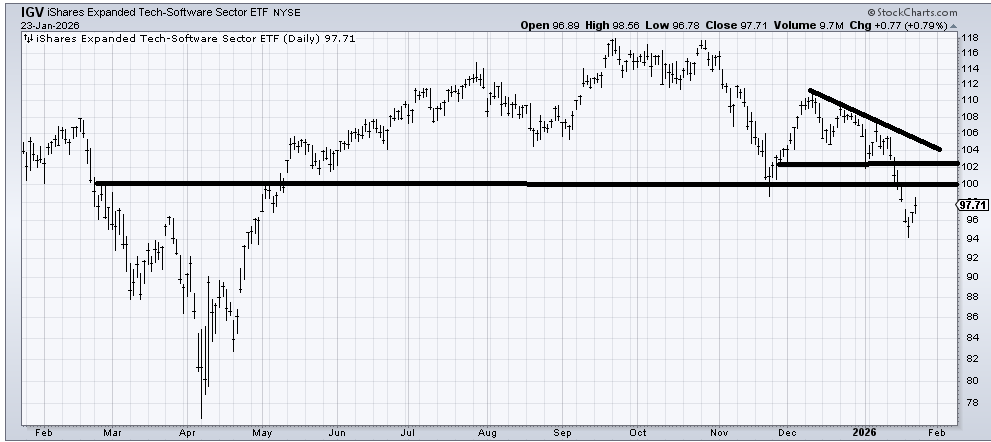

And yes, I know I said I thought the software stocks and some mega cap tech stocks were oversold and due for a bounce, and that it was the 493 that were the most vulnerable, but we got a bounce in IGV, didn’t we? Friday’s rally got to the twin lows around 98 and held on pretty well. The more serious resistance is 100-102, and unless there is a gap up over that area, I expect it to be resistance on the first trip up there.

From my perspective, the market remains in overbought territory, more so in the 493 (think RSP, Russell) than in the mega caps. But consider too that if we got everything to come down at once instead of this constant group rotation, we might get some short-term panic.

If we get some panic, we might get 90% of the volume on the downside. If we get some panic, we might get the VIX to truly look jumpy. If we get some panic on the downside, we might even get a high put/call ratio (think over 1.0).

Since everyone loves a narrative to go along with the charts, I would remind you that I am terrible at narratives. If I had to pick one, though, perhaps it is the move in Dollar/Yen that spooks the market.

Friday’s action was noteworthy. Notice on the chart (blue arrow) where it was so violent in recent times.

And while the S&P and the QQQs look quite different now vs. then, take a look at how markets reacted last summer when the currencies got loose.

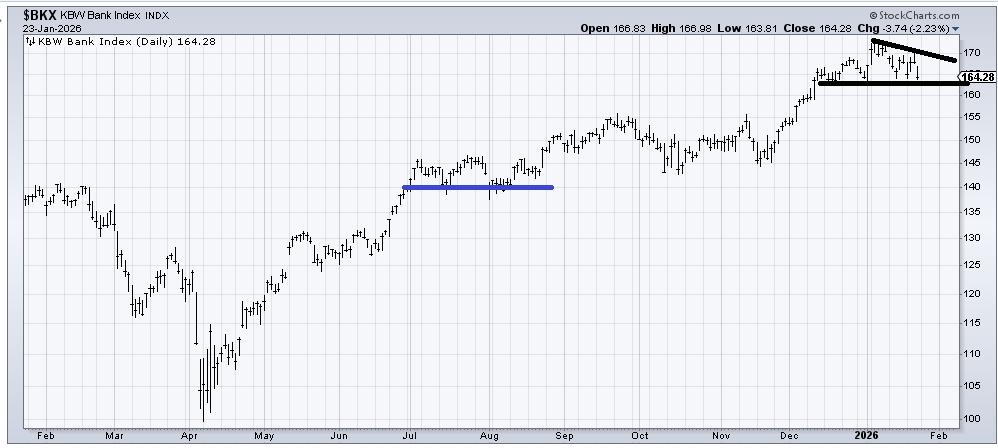

In the meantime, I still think the banks came into this year over-loved and over-owned. The Bank Index is flat on the year. It also finds itself sitting smack at a very flat support line. Last summer, when the currencies got wild, the Bank Index held. So it seems to me this is still the chart to focus on, especially since the Bank Index relative to the S&P has already made a lower low.

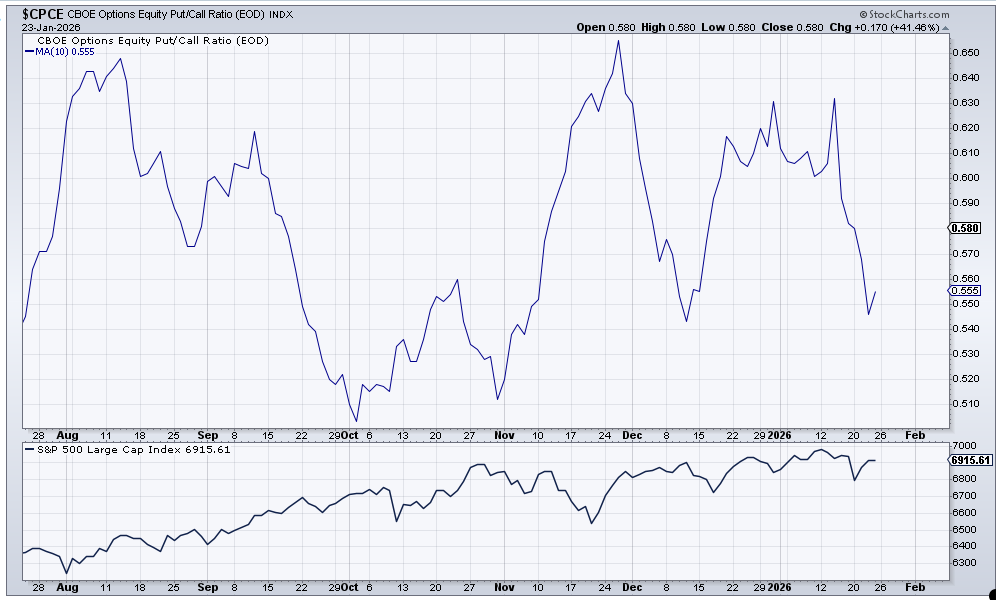

On the sentiment front, there is no need to reiterate all the indicators that lean toward complacency, but now I would add the ten-day moving average of the equity put/call ratio. It is turning upward now. Notice the early October move up coincided with that mid-month whack. The late October reading gave us November’s decline. And most recently, the mid-December reading gave us that move from 6900 to 6700 on the S&P. Oh, sure, perhaps last week’s move down was enough, but we did not see an equity put/call ratio reading over .60 one day last week, so I suspect there is still a move to come.