Will the Fed Drop Policy Clues at Jackson Hole?

All eyes are on the upcoming big event, so let's look at the possibilities. Also, let's chart the S&P, check on the Putin-Trump talks and what's ahead.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

One item stands above all of the others this week. There are not a lot of earnings reports to look forward to, though there are a few headliners that will be reporting. There are not a lot of macroeconomic data-points scheduled for release. Outside of Housing starts and existing homes sales, there's nothing at the headline level that will cross the tape this week economically.

Oh yeah, I almost forgot (no, I didn't): There is one high level economic event on the docket for this week. Like your birthday, it happens but once a year. Traders, investors and economists look forward to it for months, and this year is no different. It kind of signals the end of summer, more so for folks in our line of work than even Labor Day or the start of football season.

Of course, I am speaking of the Kansas City Fed's annual Economic Symposium at Jackson Hole, Wyoming. What joy. The great outdoors. The wild west. Real Americana. Oh, and white paper after white paper, most of which will never be read by anyone who does not have to read them for work. Of course, the white papers and the public display of sometimes more siloed economic thought that we would like, are not the main events.

The main event will occur on Friday morning. Fed Chair Jerome Powell will speak from Jackson Hole at 10 a.m. ET this Friday. Trading volumes may ebb a bit this week in front of that event. I kid you not. A week ago, it was almost expected that Powell would use his address this Friday to pivot the central bank toward a looser monetary posture. After last week's July consumer price index print, a print that showed almost no inflation across tariff impacted industries, the pivot was still a "go" even if only in our heads.

Then came a producer price print for July that was too warm to touch. Ouch. That print knocked those of us that thought we knew our stuff on our collective tail. That print has, or should have, every one of us who has preached (hand raised), thinking twice about what the FOMC should do next. Do I still think the FOMC could cut the target range for the Fed Funds Rate on Sept. 17? Yes, I think I do, but the arrogance in how I express that thought is now gone (good riddance). I am not sure. I feel shame. Though my models still tell me that the Fed Funds Rate is at least 1 percentage point too high, how can I be sure after a hot print like that? Maybe the data is wrong? Don't even go there, Sarge.

Carry On Wayward Son

Masquerading as a man with a reason

My charade is the event of the season

And if I claim to be a wise man, well

It surely means that I don't know

- Kerry Livgren (Kansas), 1976

About 'Jackson Hole'

Not about the location. About the Fed's annual working retreat. The Kansas City Fed has hosted an annual economic / monetary policy symposium since 1978. In 1982, the event was held at Jackson Hole, Wyoming for the first time and never left. This year's symposium officially kicks off on Friday and will be held over the weekend, but in truth will actually get underway this Thursday evening.

The theme this year will be "Labor Markets in Transition: Demographics, Productivity. and Macroeconomic Policy." This is quite fitting as three weeks prior to the event, the Bureau of Labor Statistics informed America that they had badly miscounted job creation and had to revise both the May and June data for non-farm payrolls down to near zero while also reporting a weak month of July.

As discussed above, there is some thought that Fed Chair Jerome Powell will use his Friday address to tee up the September meeting for a change in policy as he did last year. At last year's symposium, Powell said bluntly, "The time has come for policy to adjust." A few weeks later the Federal Open Market Committee cut its target range by a half percentage point.

The reason last year's cuts were so controversial was that this came just six weeks ahead of a national election, despite the fact that data at the time did not support a rate cut. That broke with multiple decades of precedent. The Fed would squeeze in another half point of rate cuts prior to the new year, which was 2025.

This year, there were for a number of months, conditions that did indeed support easier policy. After last week's producer price index, we have to wonder if that window of opportunity has closed and if it has closed this quickly, we also have to wonder if maybe it was indeed prudent of this Fed Chair to drag his feet on taking that step. Time will tell.

Should Powell decide to punt the topic into September and allow more data to come in ahead of making such a decision, he could simply discuss the relationship between full employment and inflation. In recent years, the Phillips Curve has not worked as well as it does in the textbooks, as the economy and all markets have been perverted by both irresponsible fiscal policy and reckless monetary policy.

Powell could illustrate how the central bank will have to prioritize one of the Fed's dual mandates over the other as labor markets cry out for lower short-term interest rates, but inflation is suddenly asking for more caution. Powell could also discuss changing the Fed's approach to fighting inflation and simply working toward a target instead of trying to average a target rate over time. This is something that Wells Fargo WFC senior economist Sarah House has been writing about of late.

I Don't Know

Everyone Goes Through Changes

Looking to Find the Truth

Don't look to me for answers

Don't ask me, I don't know

- Ozzy Osbourne, 1980

Last Week

Domestic equity markets were hot until cooling off ahead of the weekend. As mentioned, the inflation data came in a bit wonky. At the consumer level, it was manageable. At the producer level, not really. As we know, producer prices don't always lead consumer prices, but they can. In this case, with no consumer-level inflation across tariff-impacted industries, but plenty of producer-level inflation across those same industries, we know that corporate margin was, at least for July, compressed.

Away from the inflation-focused data, July Retail Sales were strong enough at both the headline and the core, but July Industrial Production was weaker than we would have liked. By that time, the markets and the world were watching what was happening in Alaska. While, undoubtedly, markets would react well to any kind of peace agreement or even a cease-fire in eastern Europe, it's hard to say exactly what did happen in Alaska on Friday.

While it is obvious that Presidents Trump and Putin of the U.S. and Russia had a positive meeting, there is no peace yet. Pres. Putin has apparently made what is acceptable to him known. Now, Ukrainian Pres. Zelenskyy of Ukraine will travel to Washington for a Monday meeting with Pres. Trump. At least five or six European heads of state will travel with him. Will Pres. Zelenskyy be willing to trade territory for a security guarantee led by the U.S.? We should know more at some point later today.

Weekly Numbers

What the major to mid-major U.S. equity indexes did last week, as the nation focused on inflation and the world focused on Alaska:

- The S&P 500 gave up 0.29% on Friday but gained 0.94% for the week.

- The Nasdaq Composite gave back 0.4% on Friday but gained 0.81% for the week.

- The Nasdaq 100 dropped 0.51% on Friday but gained 0.43% for the week.

- The Russell 2000 fell 0.55% on Friday but gained a whopping 3.07% for the week.

- The S&P Smallcap 600 gave up 0.67% on Friday but soared 3.15% for the week.

- The S&P Midcap 400 lost 0.58% on Friday but gained 1.55% for the week.

- The Dow Transports dropped 0.4% on Friday but added 2.1% for the week.

- The Philly Semis surrendered 2.26% on Friday but gained 1.32% for the week.

- The KBW Bank Index fell 1.96% on Friday but tacked on 1.32% for the week.

On Friday, four of the 11 S&P sector SPDR exchange-traded funds closed out the session in the green, led higher by Health Care XLV and the REITs XLRE as traders moved into the defensive sectors. Two of these funds closed unchanged and five closed in the red. The Financials XLF were the big losers on Friday.

For the week, seven of the 11 S&P sector SPDR ETFs traded higher, led in a northerly direction by Health Care and Communication Services XLC. Defensives on the whole, did not have a good week, as the Utilities XLU and Staples XLP claimed the bottom two rungs on the weekly performance tables.

The GDP Game

Last week, the Atlanta Fed left their GDPNow model for the third-quarter unrevised at growth of 2.5% (q/q, SAAR). Among other regional central bank district branches running close to real-time GDP models, the New York Fed's estimate for Q3 growth now stands at 2.06%, up from 2.02%, while the Cleveland Fed's model for the third quarter stands at growth of 1.93%. The St. Louis Fed finally released an initial GDP estimate for the third quarter and it's a doozy. St. Louis, as of this weekend, sees Q3 GDP at "growth" of -0.3%.

Fed Funds Futures

Looking past this week's backyard barbecue in Wyoming, Fed Funds Futures markets trading in Chicago are currently pricing in an 85% probability for a quarter-percentage point rate cut on Sept. 17, and just a 52% likelihood for an additional quarter-point cut on Oct. 29. That's it for the year right now, as these markets are now pricing in just a 39% probability for a total of three quarters of a percentage point worth of rate cuts by year's end.

Interesting

According to a tactical report released by Goldman Sachs GS covering peak retail trading days this year, the three most heavily traded stocks traded by retail investors / traders (on those days) in terms of percentage of shares traded to shares outstanding are Keycorp KEY, Huntington Bancshares HBAN and Ford Motor F. By net amount bought (notional bought minus notional sold) by retail investors / traders, the top three are Advanced Micro Devices AMD, Tesla TSLA and Microsoft MSFT.

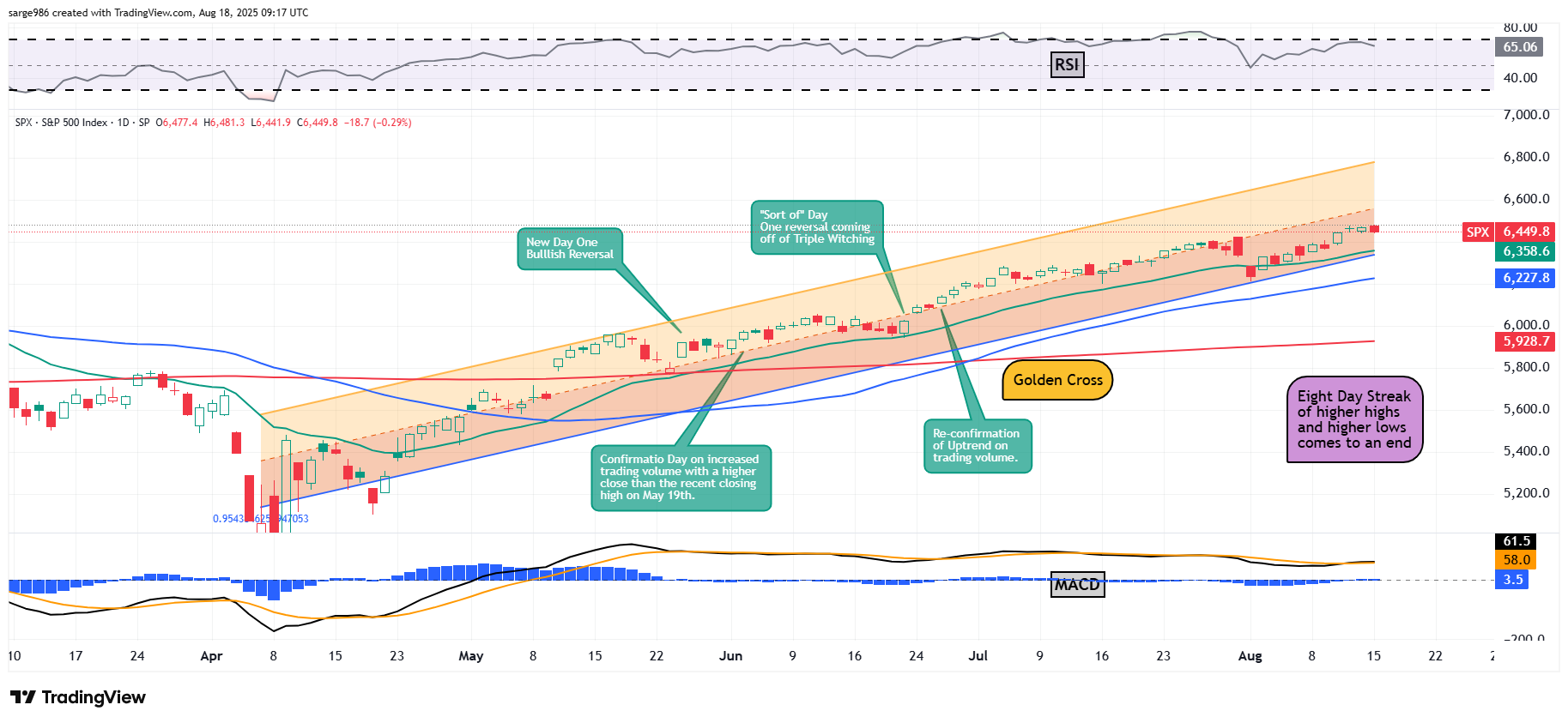

The Chart...

There are two main changes to the daily chart of the S&P 500 from the chart I posted for readers a week ago. One, that streak of higher-lows coupled with higher-highs that we all enjoyed finally came to an end late last week. The streak reached eight days as the index made news highs, Now, for the past two days, prices started to consolidate ahead of the Russo-Ukrainian peace talks and Jackson Hole.

That probably could have been anticipated. Markets will remain susceptible to headline risk this entire week. Lighter trading volume ahead of Powell's speech on Friday could also be a "thing" unless something extremely newsworthy comes out of Presidential Zelenskyy's meeting with Pres. Trump in D.C. late today.

The second significant change is in the daily Moving Average Convergence Divergence below the chart. While the index continues to color within the lines created by this Raff Regression model, and Relative Strength remains robust (but not technically overbought), the components of the daily Moving Average Convergence Divergence have all turned more bullish.

The histogram of the S&P 500's 9-day Exponential Moving Averge is finally back in positive territory after a month on the dark side. In addition to that, the 12-day EMA (black line) has crossed back above the 26-day EMA (gold line). Though the index is obviously going to be impacted by news events this week, this is the most bullish these indicators have looked for at least the short to medium-term future since early to mid-July.

On The Docket...

I don't think we need a traditional "What's Ahead" section this week. Everything from sentiment to market performance this week will be about hopes for peace in Europe and Jackson Hole. That said, there are other news items out there that could sway markets and move individual stocks. Be cognizant of the following:

The domestic macroeconomic calendar is not especially heavy this week. The focus will be on housing. On Tuesday morning, the Census Bureau will release July Housing Starts and Building Permits. This is the only macroeconomic event this week considered significant for the Atlanta Fed to revise their Q3 GDPNow model after its release. On Thursday morning, the National Association of Realtors will release July Existing Home Sales, the Philadelphia Fed will release the results of its regional manufacturing sector survey for August, and S&P Global will release their flash PMIs for August for both the manufacturing and service sectors.

The earnings calendar remains light this week, but we will be hearing from several higher-profile firms than we have heard from for a couple of weeks. In particular, we'll hear from a bevy of well-known retailers. The results and guidance form that group will offer investors key information regarding the financial health of the US consumer as well as the impacts of the president's tariffs on margin.

This evening, we'll hear from cybersecurity giant Palo Alto Networks PANW. On Tuesday morning, Home Depot and Medtronic MDT will report, followed by home-builder Toll Brothers TOL on Tuesday afternoon. Wednesday morning, Estee Lauder EL, Lowe's LOW, Target TGT and TJX TJX will all publish their numbers. Finally, on Thursday morning, the most important corporate event of the week takes place as Walmart WMT posts its data, followed by Intuit INTU, Ross Stores ROST, Workday WDAY and Zoom Communications ZM that evening.

Economics

(All Times Eastern)

10:00 - NAHB Housing Market Index (Aug): Expecting 34, Last 33.

The Fed

(All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights

(Consensus EPS Expectations)

After the Close: FN (2.63), PANW (.89)

At the time of publication, Guilfoyle was long PANW, WFC, KEY, F, AMD, MSFT, TJX equity.