Will It Be a November to Remember After October's Failed Shakeout?

What does a month that's been the best for the S&P 500 since 1950 hold in store for investors this year? Here's everything you need to know to prepare for the week ahead.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Let the holidays begin? Something like that.

October is finished and with it the perceived dangers of autumn. I think. The expected negativity of September passed with only a few "not so scary" red candle days to show for the month. We thought, especially with its history, that October might try to shake us out and indeed October did try. Even the government shutdown couldn't force any of the October selloffs to truly take root. Not even the October 10 session, when the S&P 500 gave up 2.7% and the Nasdaq Composite was roasted for 3.6%, could make that happen.

Despite, or maybe in spite of that government shutdown, and a more hawkish Fed than expected, the U.S. economy has fared better than many expected. In addition, inflation has slowed more than many expected as tariffs have impacted economic activity to a lesser degree than thought while padding the U.S. Treasury's otherwise desperate fiscal situation. On top of that, the U.S. made a flurry of positive-looking trade deals with Asian nations towards the end of the month.

That all added up to gains of 4.7% for the Nasdaq Composite and 2.3% for the S&P 500 for the month that is often thought of as the most volatile for many traders and investors of a certain age. That does not mean that "they" won't try to shake us out in November. If neither September or October acted as they normally would, then it would be reckless to assume that a regularly positive month such as November would also act "normally."

Still, it's hard to ignore the fact that the Stock Trader's Almanac claims that November is the best month for the S&P 500 since 1950, averaging a return of roughly 1.9%. In fact, Fidelity reports that since 1945, the rolling six-month period of November through April is our market's topperforming rolling six-month period, averaging a return of 7%.

About That Shutdown

I was hoping. I was wrong. There were no signs of life from the U.S. Senate over the weekend. I had thought that with the expiration of food subsidies, even if a way must be found (maybe, for the moment) to keep those benefits going and with Election Day this Tuesday (tomorrow) that one side or the other might flinch.

Today (Monday) is Day 34 of this shutdown. The previous record for any shutdown is 35 days. A new record now seems almost a certainty.

President Trump appeared on "60 Minutes" on Sunday night. He said that he thought that the Democrats would eventually vote to reopen the government, but added, “The Republicans have to get tougher. If we end the filibuster, we can do exactly what we want.”

I would be really careful about going that route. Once that dam breaks, it's broken for good.

Markets

The Nasdaq Composite has now closed in the green for seven consecutive months. The S&P 500 has a six-month winning streak going at this time. On Wednesday, the FOMC cut its target range for the Fed Funds Rate by 25-basis points and announced the end of its "quantitative tightening" program by the end of this month. This would all seem to be dovish in nature.

The only flies in that ointment there would be that Fed Chair Jerome Powell sounded almost hawkish in his press conference and as many voting committee members (one) dissented in favor of no rate cut as did dissent in favor of a larger rate cut. That said, those looking for further rate cuts might take solace in the fact that the dovish dissenter was Fed Governor Stephen Miran who likely is not going anywhere, and the hawkish dissenter was Kansas City Fed President Jeffrey Schmid who will vote on December 10 for his last time until 2028.

Magnificent Seven stocks stole the show last week. Microsoft (MSFT) left investors mildly disappointed, while Meta Platforms (META) scared investors right out of their socks (and shares). However, Alphabet (GOOGL) , Apple (AAPL) and Amazon (AMZN) all did or said what investors wanted to hear.

Lastly, markets cheered to some degree as President Trump returned home from a weeklong trip to Asia with new/improved trade deals/trade truces having been made/extended with Malaysia, Cambodia, Vietnam, Thailand, Japan, South Korea and China.

The Week That Was

What the mid-major to major U.S. equity indexes did last week, as the president concluded a successful trade-focused trip to Asia, and the Fed cut rates while announcing the end of QT... Oh, and as the federal government concluded an entire month of closure.

- The S&P 500 gained 0.26% on Friday and 0.71% for the week.

- The Nasdaq Composite gained 0.61% on Friday and 2.24% for the week.

- The Nasdaq 100 added 0.48% on Friday and 1.97% for the week.

- The Russell 2000 gained 0.54% on Friday but lost 1.36% on the week.

- The S&P Smallcap 600 added 0.12% on Fridaybut gave up 2.84% for the week.

- The S&P Midcap 400 gained 0.61% on Friday but surrendered 1.59% for the week.

- The Dow Transports added just 1.02% on Friday and 2.82% for the week.

- The Philly Semis gained just 0.18% on Friday and a nifty 3.61% for the week.

- The KBW Bank Index added 0.37% on Friday but gave back just 0.03% on the week.

On Friday, seven of the 11 S&P sector SPDR ETFs closed out the session in the green, easily led higher by the Discretionaries (XLY) . Defensive sectors took four off the bottom five slots on the daily performance tables.

For the week, eight of the 11 S&P sector SPDR ETFs traded lower with the REITs (XLRE) , Materials (XLB) , Staples (XLP) and Utilities taking a real pounding. Again, pain for the defensives.

Technology (XLK) was the runaway winner as semiconductor stocks continued to run wild. Marvell Technology (MRVL) gained a stunnning 11.4% for the week, followed by Nvidia (NVDA) at +8.7%.

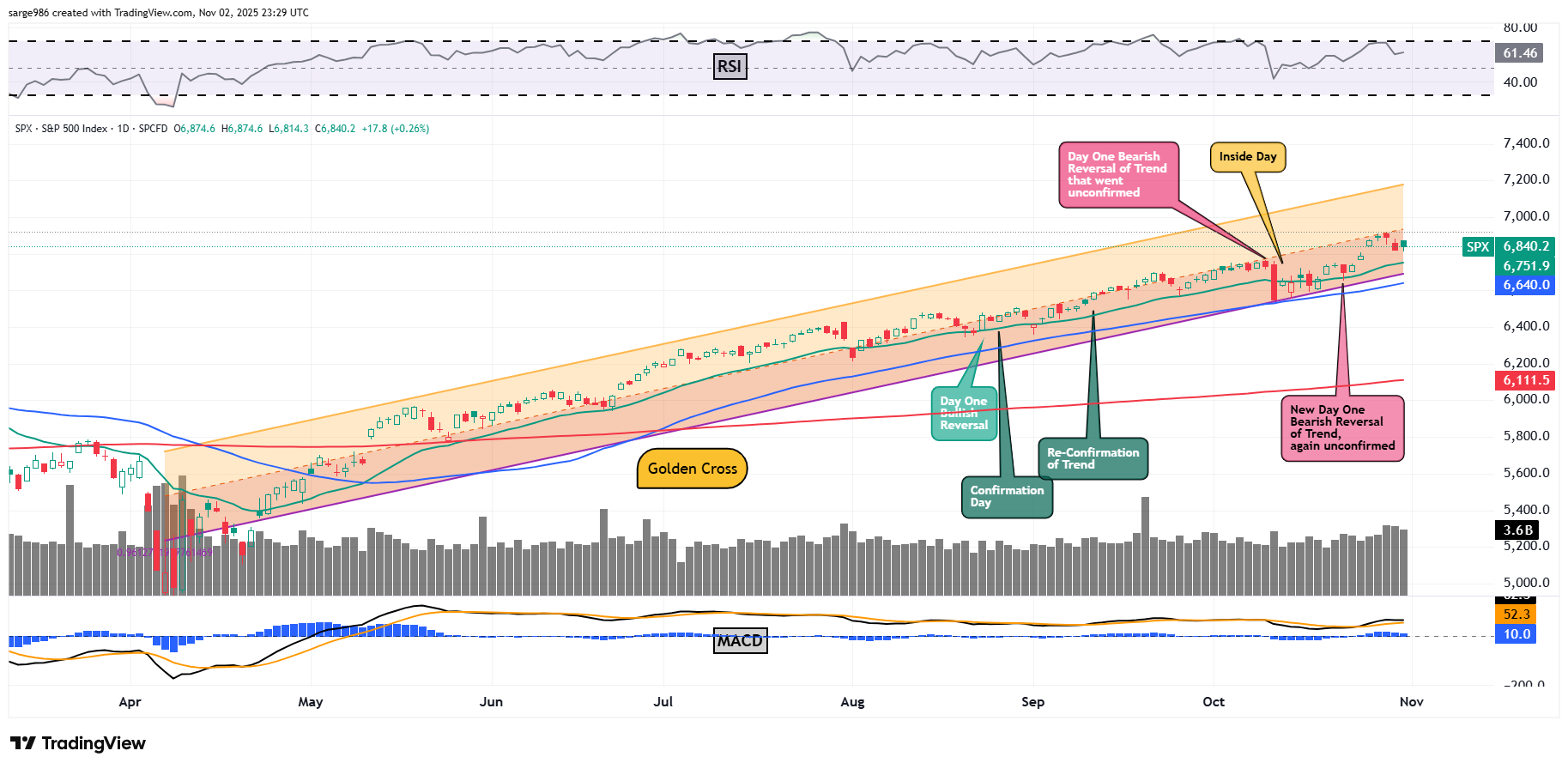

The Chart

Last week, while the index generally moved in a northerly direction, markets showed some broad indecisiveness. Friday's positive session, for me, came close to being a "Re-Confirmation of Bullish Trend Day" as both the S&P 500 and Nasdaq Composite had positive sessions. Breadth was decent too.

What gives me pause is this: While aggregate trading volume was higher across the board, winners beat losers at both exchanges and advancing volume rounded declining volume, the small-to mid-cap stocks took a beating and it was the final trading session of the month. That can make for some wonky outcomes. It does not have to make for a winky outcome. It can. We may declare this a reconfirmation in hindsight. Trust me, I want to call it. I'm the guy calling for a year-end melt-up, but I have to call balls and strikes, not what I want to see.

Readers will note that Relative Strength for the S&P 500 has remained rather robust for about two weeks now since leaving neutral territory, all without entering into a technically overbought state. The daily moving average convergence divergence (MACD) is now postured bullishly without reservation. Within that indicator, the histogram for the 9-day exponential moving average (EMA) has been back above zero for more than a week. That's a short-term bullish signal. In addition, the 12-day EMA had crossed back above the 26-day EMA, and held that crossover all week. Both of those lines remain in positive territory, which is a short to medium-term bullish signal.

Earnings

According to FactSet, for the third quarter, with 64% of the S&P 500 having reported, 83% of those companies have pleasantly surprised on earnings (down from 87% last week with 26% of companies reporting) while 79% of those companies (down from 83%) have surprised in the right direction on revenue generation. The fast start to earnings season and increased guidance in general, has boosted the blend of Q3 earnings results/growth expectations for the S&P 500 all the way to 10.7% from 9.2% last week and from just 8% a few weeks ago.

Revenue growth expectations now stand at 7.9%, up from 7.0% last week and up from 6.3% a few weeks ago. For the full calendar year of 2025, Wall Street now sees S&P 500 earnings growth at 11.2% (up from 11%) on revenue growth of 6.6%, up from 6.3% last week.

Back to the quarter, Technology, Financials, and Utilities are expected to be the outperformers with projected earnings growth of 20% or more. Materials dropped out of that elite group last week. Three sectors are still projected to suffer a year-over-year earnings contraction led to the downside by Communication Services and Energy.

Valuation

Still using data provided by FactSet, and aided by still improving forward-looking guidance, the S&P 500 ended last week trading at 22.9 times 12 months' forward-looking earnings, up from 22.7 times a week ago. This is still well above the five-year average of 19.9 times for the index as well as its 10-year average of 18.6 times. The S&P 500 also ended last week trading at 29.3 times trailing 12 months' earnings, up sharply from 28.8 times a week ago. That also stands well above the five-year (25.1 times) and 10-year (22.8 times) averages for the index.

Ten of the 11 sectors are still trading above their five-year average valuations, led by Tech (31.5 times) and Consumer Discretionaries (28.5 times). Only the REITs (17.4 times) are not historically overvalued relative to their five-year averages.

The GDP Game

Last week, the Atlanta Fed left their GDPNow model for the third quarter unrevised at growth of 3.9% (q/q, SAAR) for a second consecutive weekly period. Among other regional central bank district branches running close to real-time GDP models, the New York Fed's estimate for Q3 growth was also left unrevised at growth of 2.35%. Last week, the Cleveland Fed's model for the third quarter was actually revised upward from growth of 1.99% to growth of 2.0%. The St. Louis Fed model remained unrevised at growth of 0.59%.

With the revision out of Cleveland, something of a consensus among the regional Fed Model actually developed, with St. Louis being the outlier. Interestingly, the models have frozen almost in place due to the government shutdown, the very same shutdown that is very likely at this point making a noticeable dent in fourth quarter economic growth.

Fed Funds Futures

Fed Funds futures trading in Chicago are now pricing in a 71% probability for a 25-basis point rate on December 10, down from 94%, a week ago. At present, there are now just 50-basis points worth of additional rate cuts fully priced in (73% chance, down from 78% a week ago) for all of calendar 2026. This is in line with last week.

On The Docket

Still without a lot of macroeconomic data to go on, which really bugs a numbers nerd like myself, we proceed. Another heavy earnings week awaits. Shall we...

... The Fed will be out in force this week. Sort of. I currently have eight public appearances by Fed officials on my radar for Thursday and Friday, but just three over the first three days of the week. The most influential speakers of the week would have to be either Fed Gov. Michelle Bowman on Tuesday morning or Fed Gov. Christopher Waller on Thursday morning. Both are considered to be finalists to replace Fed Chair Jerome Powell when his term as Chair, but not as a governor, ends this May.

.... As long as the government shutdown continues, the macroeconomic calendar will remain light. Once the government reopens, trying to track all of the data will almost definitely overwhelm economists, but only the most recent data will matter to traders. This would be a "Jobs Week" if the government were operating normally. As things stand, the ADP Employment Report for October on Wednesday morning will be the week's highest impact macroeconomic data-point.

..... The earnings calendar will again be very heavy this week. This evening, we'll hear from Palantir Technologies (PLTR) , followed by Uber Technologies (UBER) on Tuesday morning, as well as Advanced Micro Devices (AMD) and Kratos Defense (KTOS) on Tuesday afternoon. This Wednesday, McDonald's (MCD) will report ahead of the opening bell followed by Arm Holdings (ARM) , Fortinet (FTNT) , McKesson (MCK) and Robinhood Markets (HOOD) after the close. Thursday will bring us results from Datadog (DDOG) , Moderna (MRNA) , Ralph Lauren (RL) , Airbnb (ABNB) , and Take-Two Interactive (TTWO) . Friday will be a very light earnings day this week. There are no headliners reporting.

Other events this week include...

Tuesday - Pfizer (PFE) has until this date to match Novo Nordisk's (NVO) bid for Metsera (MTSR).

Wednesday - Bank of America (BAC) holds its investor day in Boston.

Wednesday - The Supreme Court will hear arguments in regard to the legality of President Trump's tariffs. Arguments for punitive tariffs linked to the illicit fentanyl trade and illegal immigration as well as reciprocal tariffs are likely to be rolled up into one argument.

Thursday - The National Retail Federation is expected to issue its 2025 holiday sales forecast.

Friday - Secretary of War/Defense Pete Hegseth is expected to outline a new process for the procurement and acquisition of defense-related goods and services. The idea will be to speed up the development and introduction of the tools necessary to succeed on the battlefields of tomorrow. Airborne, seaborne and land-based drones will be in focus as will hypersonic weapons and dominating "space" before our near peer adversaries do.

Economics (All Times Eastern)

09:45 - S&P Global Manufacturing PMI (Oct-F): Flashed 52.2.

10:00 - ISM Manufacturing Index (Oct): Expecting 49.3, Last 49.1.

The Fed (All Times Eastern)

12:00 - Speaker: San Francisco Fed Pres. Mary Daly.

14:00 - Speaker: Reserve Board Gov. Lisa Cook.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: (ON) (.59), PNW (3.08)

After the Close: CBT (1.68), (FANG) (2.94), (PLTR) (.17), (QRVO) (2.11), (WMB) (.52)

At the time of publication, Guilfoyle was long PLTR, NVDA, MSFT, GOOGL, PLTR, AMD, KTOS equity; and short AMZN equity.