Why You Should Add Private Market Alternatives Investments Now

Private markets present a timely opportunity to enhance portfolio diversification, improve risk-adjusted returns, and generate reliable income.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Our research and conversations with top tier alternative investment managers leads us to the conclusion that investors and wealth advisors should strongly consider increasing allocations to alternatives now. With public equity valuations at historically high levels, credit spreads near record lows, and structural shifts pointing toward a potential new era of inflation and volatility, private markets present a timely opportunity to enhance portfolio diversification, improve risk-adjusted returns, and generate reliable income. Yet, many advisors and investors remain underexposed, despite increasing access to these asset classes. Now may be the time to lean in.

A Growing Investment Opportunity

Private markets have experienced tremendous growth over the past decade. In 2010, total private market assets were valued at $2.7 trillion, a figure that increased to $9.3 trillion by 2021. By 2028, this market is expected to exceed $19.3 trillion, nearly doubling in size in just five years. This growth is not limited to institutional investors. Wealth management firms and asset managers are expanding investment vehicles to provide high-net-worth clients with greater access to private equity, private credit, real estate, and infrastructure investments.

Private equity remains the largest segment of the private markets, with approximately $3.6 trillion allocated to buyouts, $1.9 trillion to venture capital, and $1.1 trillion to growth equity. Private credit has emerged as a major force, currently valued at $1.6 trillion, as banks reduce lending and direct lending strategies expand. Real estate and infrastructure investments are also growing, with $1.6 trillion allocated to these tangible assets, serving as both an inflation hedge and a source of stable income. Additionally, $1.8 trillion is invested in natural resources and other alternative assets, such as commodities, farmland, and energy projects. (iCapital & Prequin)

Why Invest in Private Markets?

Private market investments offer compelling advantages, particularly in today’s investment climate. One of the primary reasons to consider alternatives is their ability to reduce overall portfolio volatility. Unlike publicly traded assets, private investments tend to have lower correlations with stock and bond markets, helping to smooth out returns over time. In addition, real assets such as real estate and infrastructure provide natural inflation protection, as their valuations and cash flows often adjust with rising prices.

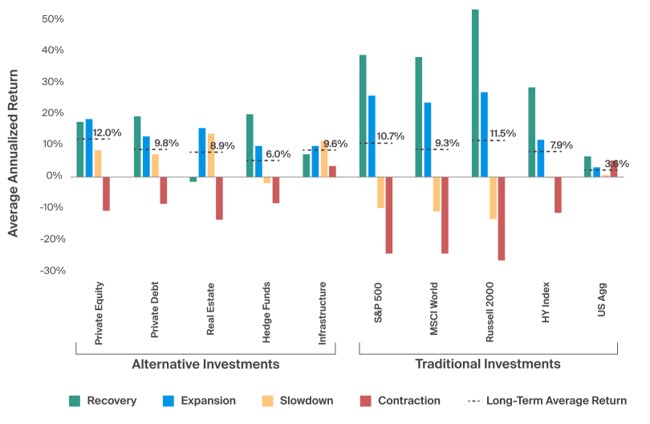

Private credit and private real estate are attractive for investors seeking reliable income streams, often offering higher yields than traditional fixed-income instruments. With public credit spreads near historical lows, the public fixed income markets in the U.S. are not likely to compensate investors for additional default risk. Historically, private equity has offered higher absolute and risk-adjusted returns relative to public markets, particularly when blended into a well-diversified portfolio.

Beyond performance metrics, private markets also present opportunities that are simply not available in public markets. Investors can gain exposure to pre-IPO companies, distressed assets, and specialized lending strategies that provide unique value propositions. As more wealth managers gain access to these investments, private markets are no longer the exclusive domain of institutional investors.

Structural Shifts Are Supporting Alternatives

The macroeconomic environment is undergoing a significant transformation, and several long-term trends are making private markets potentially more attractive. The need for clean energy is driving massive investment in infrastructure, raw materials, and labor, requiring trillions of dollars in both public and private capital. At the same time, shifting labor market dynamics are contributing to wage growth and persistent inflation, making traditional fixed-income allocations less effective as an income source.

Additionally, the move from globalized trade to more localized production is fueling domestic investment in manufacturing, semiconductors, and automation. Policies aimed at onshoring critical industries, such as the CHIPS Act, are reinforcing these trends and creating significant private investment opportunities in U.S.-based production. Meanwhile, the rapid rise of AI and digitalization is driving demand for computing power, energy, and data infrastructure, creating an entirely new frontier for alternative investments.

The second Trump presidency could further reinforce inflationary pressures, with proposed tariffs on Chinese exports, stricter immigration policies, and increased energy permitting potentially prolonging supply chain disruptions and labor shortages. If these factors materialize, inflation could remain persistently high, further strengthening the case for real assets, private credit, and infrastructure investments as hedges.

Market Signals Suggest Private Markets May Outperform

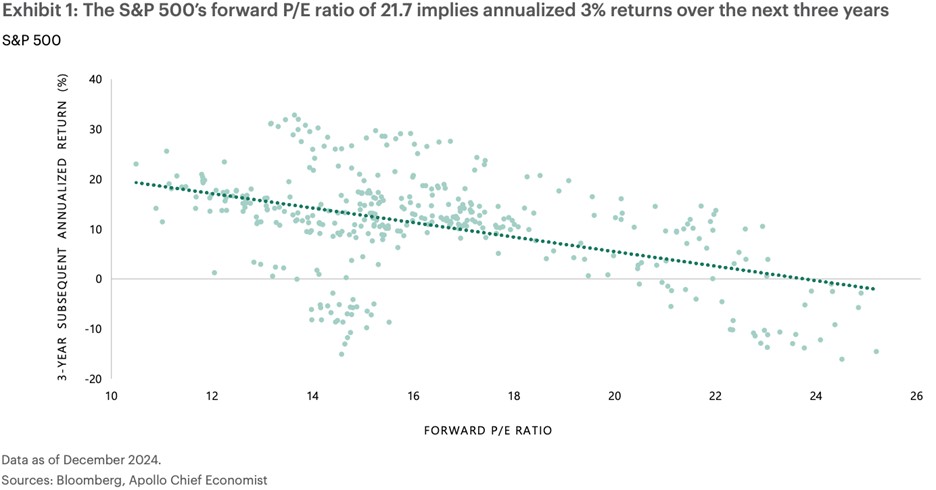

Public market valuations are flashing warning signs that suggest alternative investments could generate better risk-adjusted returns in the coming years. The S&P 500 forward price-to-earnings ratio is currently at 21.7x, which historically correlates with subdued equity returns over the next three years. Bloomberg and Apollo’s research suggest that, based on historical relationships, this implies an expected annualized return of just 3% for large-cap equities. While this doesn’t mean public stocks won’t perform, it does highlight the need for investors to consider alternative sources of return, particularly if they rely on passive indexing strategies.

The public credit markets are also showing signs of distortion. High-yield bond spreads are extremely tight, meaning investors are not being adequately compensated for taking on default risk. This compression in spreads suggests that private credit may offer superior return potential compared to traditional fixed-income allocations.

Additionally, the historical relationship between inflation, interest rates, and asset returns suggests that a higher-volatility regime may persist, narrowing the dispersion of expected returns between asset classes. This shift flattens the efficient frontier, making it even more critical for investors to diversify beyond traditional 60/40 portfolios. In the past decade, a 60/40 portfolio generated an average annual return of approximately 8%, but achieving similar returns in the coming years may require greater exposure to alternative asset classes.

A Key Differentiator for Wealth Advisors

Wealth advisors who develop expertise in alternative investments stand to differentiate themselves in a competitive market. Many high-net-worth investors are interested in alternatives but lack the necessary understanding to allocate capital effectively. According to Brookfield Oaktree, surveys show that 72% of investors would consider alternatives if they understood them better, and 70% would allocate to alternatives if their advisor recommended them. Additionally, 86% of investors are willing to tolerate higher volatility if it helps them achieve their investment goals. Despite this demand, many advisors are not well-versed in private markets, and those who can provide deep knowledge and access to high-quality opportunities will have a significant competitive advantage.

How Advisors Could Approach Private Market Allocation

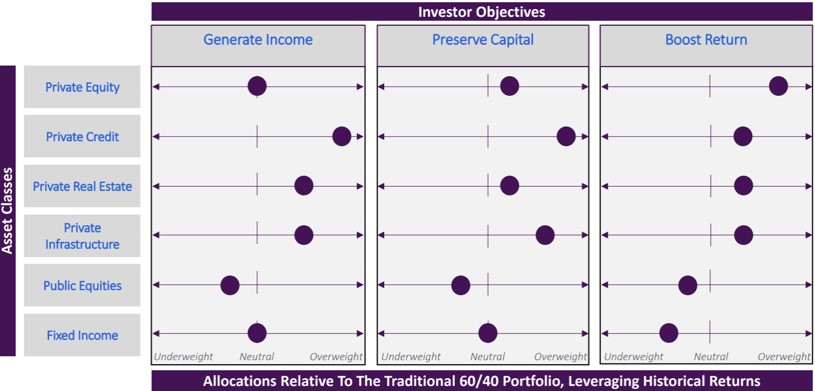

Incorporating alternative investments into client portfolios requires a thoughtful approach based on the investor’s primary objectives. If the goal is maximizing long-term returns, overweighting private equity, private credit, real estate, and infrastructure while reducing reliance on traditional fixed-income securities can enhance performance. If the primary objective is income generation, allocations could favor private credit, real estate, and infrastructure, while public equities should be reduced. For investors focused on capital preservation, an overweight position in private credit and infrastructure can improve the portfolio’s risk-return profile while maintaining stability.

Final Thoughts: It May Be Time to Lean into Private Markets

Given the current investment landscape—high public equity valuations, compressed credit spreads, and a changing macroeconomic environment—the case for increasing exposure to private markets has never been stronger. Alternative investments provide diversification, return potential, and inflation protection, making them an essential tool for advisors looking to navigate the next market cycle effectively. The past decade’s investment playbook may no longer work in the decade ahead, and allocating strategically to private markets could be the key to achieving superior risk-adjusted returns in the coming years.

I would love to hear your feedback, comments, and thoughts. Are you investing in the private market now? If not, what is holding you back? For many people it is a matter of education and specialized guidance.