Who's the Culprit Behind the Alarming Move in Treasuries?

Trade wars and tariffs are influencing U.S. interest rates. Let's run through the likely 'suspects' and what the U.S. can do about it.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

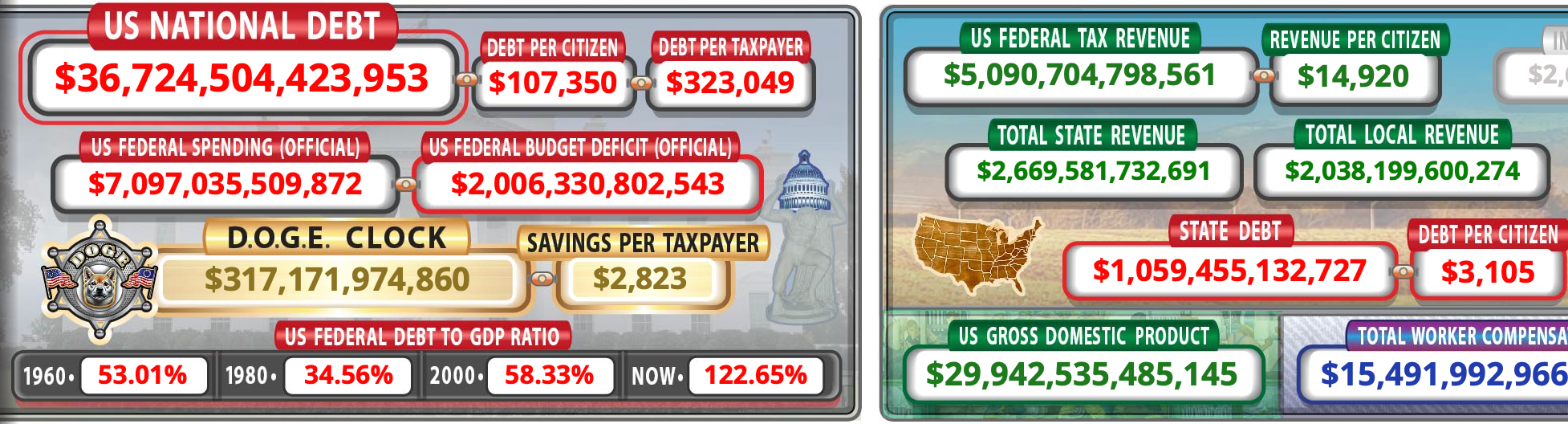

The U.S. has a massive debt, and that debt is growing due to a huge deficit.

Some people use these terms interchangeably, but they’re not the same. What is the difference between the debt and the deficit?

The U.S. needs buyers of Treasuries to finance its massive national debt, which is rapidly approaching $37 trillion. This is referred to as "the debt."

Annual spending is $7 trillion, which is $2 trillion higher than federal tax revenue, which is around $5 trillion. This $2 trillion is known as "the deficit."

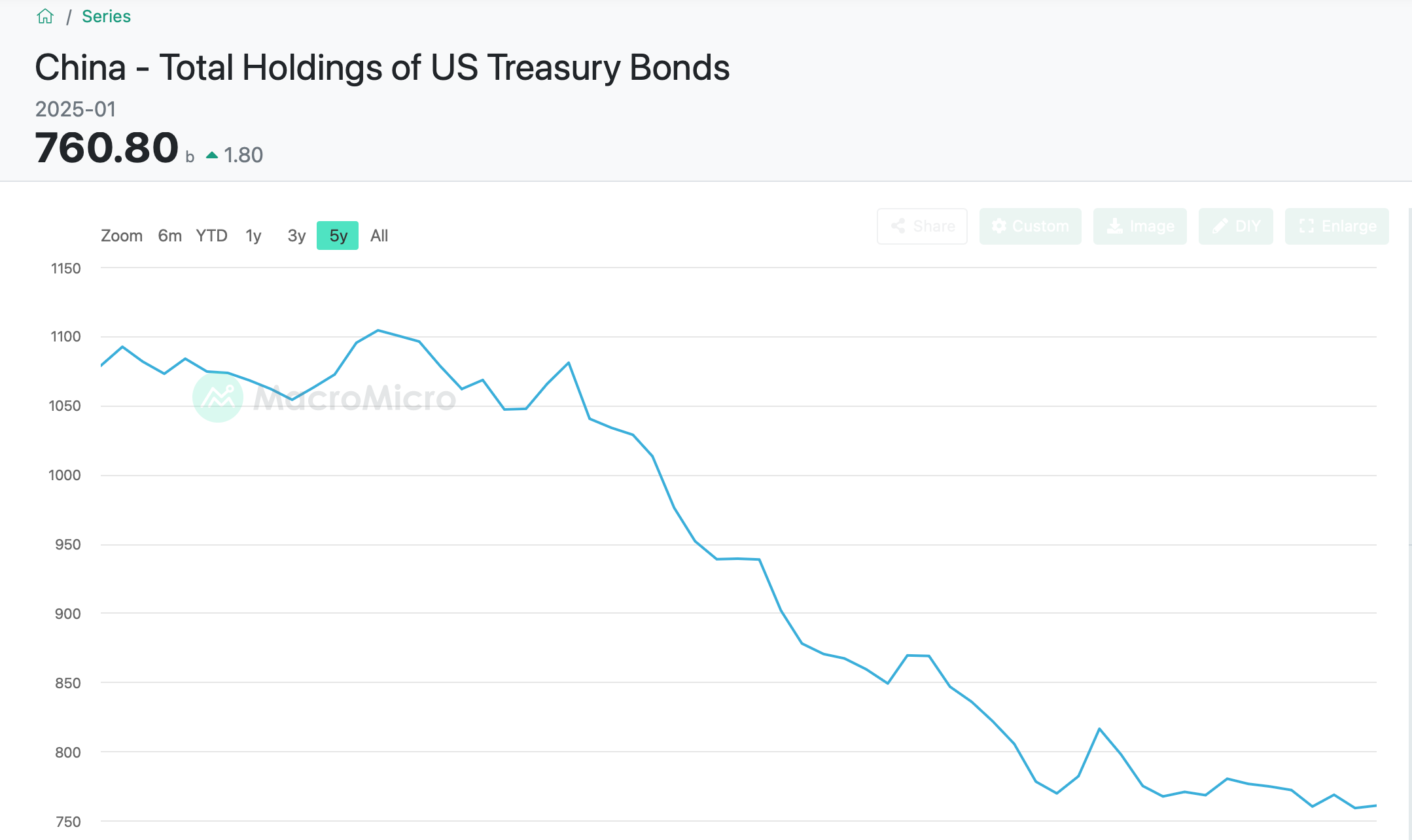

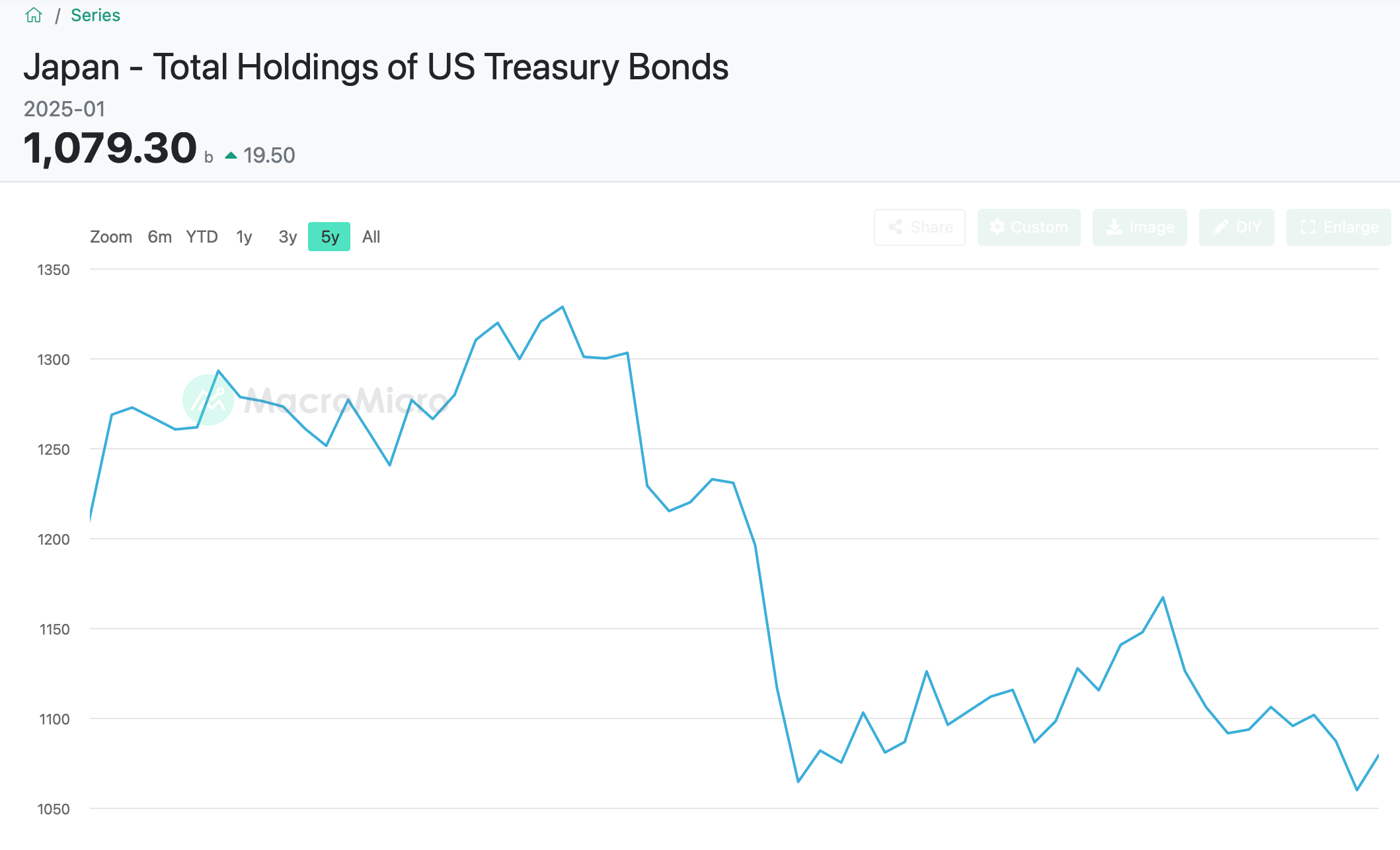

The U.S. finances its debt by selling Treasuries. The biggest buyer of Treasuries is Japan, which holds over $1 trillion. China is second with $760 billion.

Treasuries have an inverse relationship between price and yield. When prices fall, yields climb. The most closely watched Treasury is the 10-year note.

On Friday, April 4, the price of the 10-year hit 106 (arrow). This was its highest price in over two years.

Then on Monday April 7, a massive amount of selling was unleashed. One just week later, the 10-year traded at 102.

Due to the inverse correlation between price and yield, the sharp drop in price sent the yield of the 10-year Treasury soaring (below, arrow).

This rise in yield comes at a bad time for the U.S., which is due to refinance about $9 trillion of its massive debt. No doubt, the U.S. would rather refinance at a lower rate.

Who is the big seller that pushed the 10-year Treasury note from 106 to 102 in just a week? According to the weekly chart, somebody has been a heavy seller of the 10-year in the 106 area for the past three years (arrows).

Over those same years, China’s U.S. Treasury holdings declined sharply. In late 2021, China held $1.08 trillion in Treasury notes. Since then, China’s Treasury holdings have declined by about 30%.

Meanwhile, Japan’s Treasury holdings declined by about 19%. Over this time, the majority of sovereign Treasury buyers were adding to their holdings.

What can we extrapolate from the decline in Japan and China’s holdings over the past three years, combined with heavy selling at the 106 area for the past three years?

If China is the force behind the recent plunge in the price (and rise in the yield) of the 10-year Treasury, this selling is part of a long-established pattern. Therefore, the selling is not necessarily driven by the current tariff dispute.

Japan is also a likely culprit, as that country has been a net seller of Treasuries in recent years.

One theory is that Japan is selling Treasuries, for which it receives dollars, and then sells the dollars to buy yen. The net result would be a stronger yen, which Japan has pursued recently via currency intervention.

This would also explain the fierce selloff of the U.S. dollar in recent weeks.

Hedge funds are a third candidate. With the rise in volatility across markets, it’s not hard to imagine that a fund or funds needed to sell Treasuries in order to raise capital.

The bad news is that if China wants to make refinancing the U.S. debt difficult, it could drive Treasury prices much lower — and in doing so, push yields much higher.

What should the U.S. do about it? Strike a trade deal with Japan as soon as possible.

By working more closely with Japan, the U.S. places additional pressure on China to come to an agreement. It also creates a situation where the U.S. could potentially influence Japan to maintain its current level of Treasury holdings as part of a broader agreement.

At the time of publication, Ponsi had no positions in any securities mentioned.