When the High-Stakes Trades Stop Paying Off, Treasuries Will Be Waiting

Traders and investors have embraced the 'the trend is your friend' mantra in 2025, and it has worked.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Traders and investors have embraced the “trend is your friend” mantra in 2025, and it has worked for those who have plugged their noses and jumped into the crowded pool.

In other words, risk-takers who jump on momentum assets, regardless of fundamentals, have been rewarded, while traditionally diversified portfolios have been left behind.

For instance, the Vanguard Target Retirement 2030 is a textbook 60/40 portfolio with both domestic and international stocks and bonds of various types and maturities; it has yet to recover its 2021 high. Coincidentally, investors in the S&P 500 and NASDAQ indices have outperformed those with exposure to broader allocations. This is because a handful of stocks account for nearly all the gains; however, I suspect most index investors are aware of their actual risk exposure to the hottest stocks.

It is great while it is working to their advantage, but markets are cyclical; what has been working in recent years likely won’t continue to work indefinitely. Of course, nobody can know in advance when and where the inflection point will take place.

I believe society has confused trading with investing. Consider a company like (OKLO) , an advanced nuclear technology company founded in 2013 in Santa Clara, which is burning through cash at a rate of $65 million to $80 million per year. The firm has yet to book a dime of revenue but is trading at $162 per share, or a market cap of just under $24 billion. This swing-for-the-fences idea might work, but it is a high-stakes trade, not an investment. In other words, it should be done with risk capital, not money needed to put kids through college or to buy a house in a few years.

Similarly, money is flowing into gold ETFs at an unprecedented rate under the impression that doing so is an investment in a diversifying safety asset. Yet, gold is a non-income-producing commodity riddled with boom-and-bust cycles. Buying gold while it is up 50% on the year might work out, but it is not an investment; it is a trade, unless you plan on holding for multiple decades.

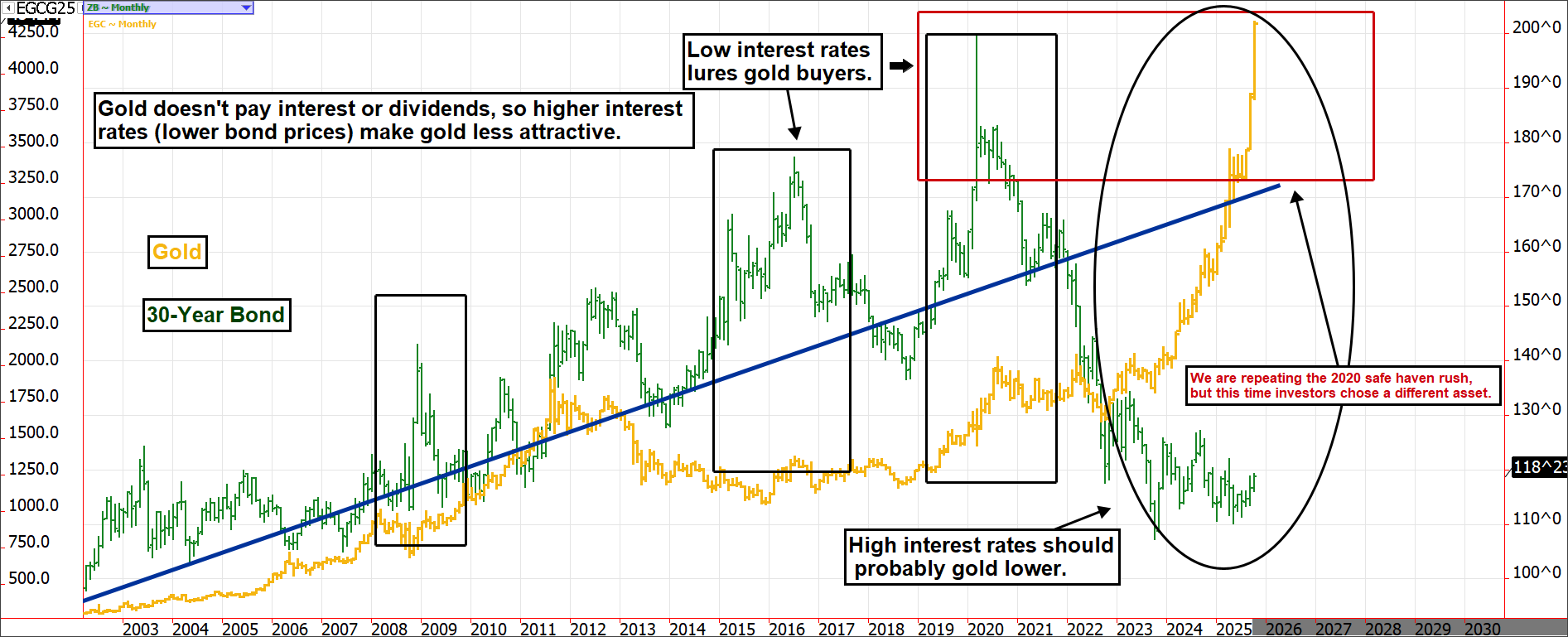

I’ve been sharing this chart all year, but I never dreamt the spread between treasuries and gold, the two primary risk-off assets, would blow out in this manner. Yet, I probably should have seen it coming. After all, we have seen this panicked rush to safety before.

In 2020, the world was reeling with a global pandemic. Investors of all types, and even central bankers, foreign entities and China, were gobbling up U.S. treasuries as quickly as they could. At their peak, the 30-year bond was paying less than 1% of interest per year in the form of coupon payments. Even worse, anyone buying these securities faced historically large interest rate risk. This is because when interest rates rise, bond prices fall. Anyone buying treasuries with almost no yield is betting that the world is so dire that they believe there is more value in the return of money than in the return on money. While it is unlikely the U.S. government will default, holding on to a less than 1% yielding asset for 30 years just to get your money back, plus a small bump, isn’t a fantastic mathematical life choice. Yet, everyone was doing it, and nobody questioned it.

If this sounds familiar, it should. In 2025, we are witnessing a similar rush to perceived safety assets as we did in 2020. However, instead of central banks and China buying treasuries, they have decided to buy gold. Coincidentally, gold, like treasuries, was in 2020 a non-yielding asset that delivers pure price risk. As the market is going parabolic due to panicked and speculative buying, those buyers are taking on excessive risk without considering the potential hangover that might come later.

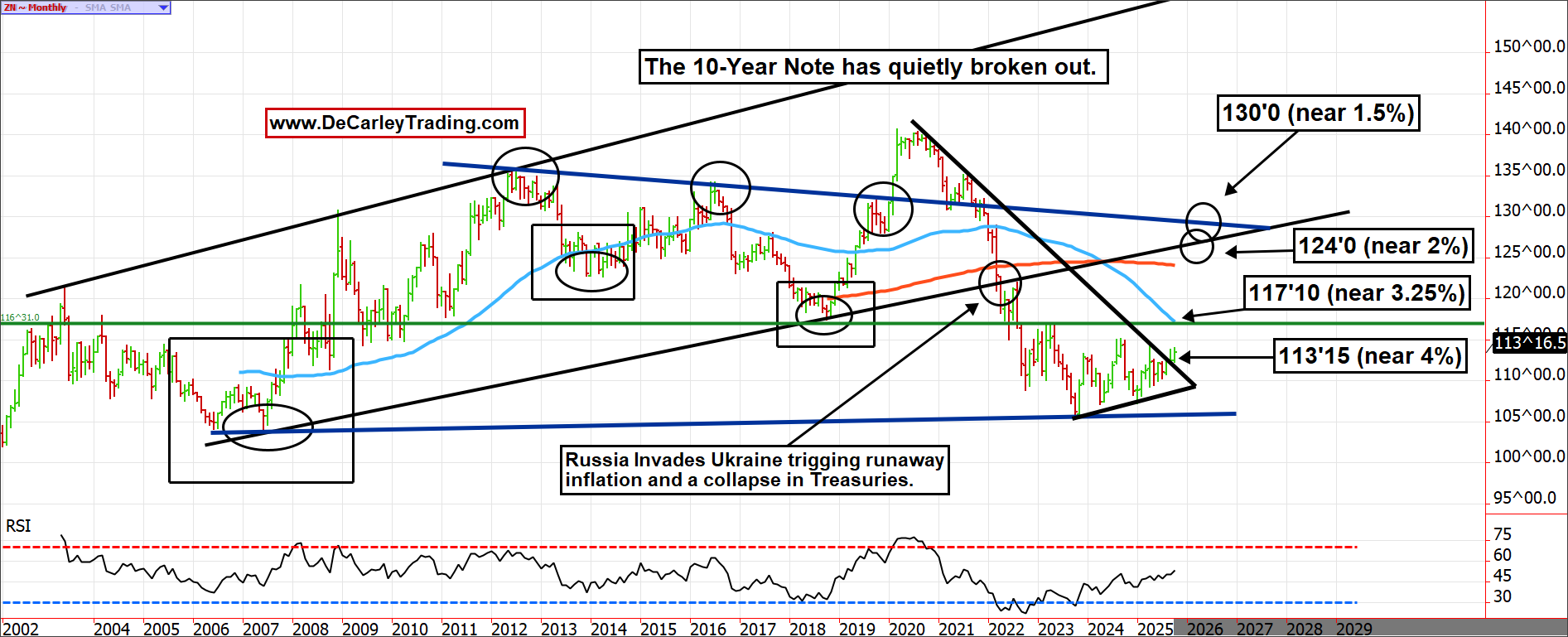

During the treasury heyday of 2020, the gold market was relatively sluggish. It wasn’t the haven of choice and wouldn’t become so for years later. However, we must wonder if the market is getting it wrong this time, as it did in 2020. Unlike in 2020, the 30-year bond is paying investors a little over 4% annually, compared to a return of zero for gold. I realize 4% sounds like a waste of time in a world where assets are appreciating by 25% to 50% regularly, but eventually those unknowingly holding excessive risk exposure will become aware of this. At that time, they might, once again, seek the return of capital rather than return on capital. If so, treasuries could, once again, be the chosen safe-haven. The 10-year note futures contract has quietly broken out, with a high likelihood of a rally that puts the yield in the low 3% area and maybe even lower if the fundamental backdrop changes.

In conclusion, history suggests that the most popular investment today might not be the best-performing one in hindsight. Further, even our fearless leaders at the Federal Reserve, in the European Central Bank or the People’s Bank of China might not be any more intelligent than the rest of us. Sometimes, jumping on the bandwagon and swinging for the fences pays off, but if you are still in the market when the music stops, it can be a whirlwind of pain.

Going into late 2025, I think it is best to ask, “How much can I lose?” rather than “How much can I make?”