When the Chips Are Down ...

Let's assess the damage from DeepSeek (and why things might not be as they appear), see what I bought (Palantir) and sold, and chart the markets.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

"This is just a mild spring zephyr compared to the big wind of '67. Or was it, uh, '76? Oh, well, no matter. Oh, I remember the big blow well."

- Owl, from "Winnie the Pooh and the Blustery Day" (1968)

The Blustery Day

OK. So, Monday was a lousy day. That said, it wasn't a really, really, really lousy day. The "ugly stick" was out and about, as we had said it would be. Parts of the market recovered, though, well before the closing bells had rung their last down at Wall Street and up at Times Square. In fact, while four of the 11 S&P sector-select SPDR exchange-traded funds gave up more than 1% for the session, with Technology XLK down an ugly 4.9%, seven of those funds closed in the green, with both the Staples XLP and Health Care XLV, up more than 2%.

In fact, the ugliness was so concentrated that within the tech space, the Dow Jones U.S. Software Index "only" gave up 1.87%, while the semiconductors were taken out to the woodshed. Choose your favorite index covering that industry. The Philadelphia Semiconductor Index was slapped around for a pummeling of 9.15%, while the Dow Jones U.S. Semiconductor Index suffered the indignation of a nearly 14% beat-down.

Within the semis, some readers might find it interesting to learn that among large caps, Nvidia NVDA, at -16.97%, was not the session's biggest loser in percentage terms, though Jensen Huang's company certainly was, in terms of market cap. Marvell Technology MRVL was roasted for a 19.1% bloodletting. On Monday, I thought the time was at least close to right to start rebuilding my longs in both Nvidia and Advanced Micro Devices AMD, which was down 6.37%. I added to both of those names for the first time in quite a while. The two long positions, after Monday's additions, are now my 16th and 17th largest allocations, so I am not yet overly exposed.

As mentioned in my work on Monday, I also added to Salesforce CRM, Palantir Technologies PLTR, and SoFi Technologies SOFI on weakness. Rounding out the day's action, I exited Dell Technologies DELL as I had never added to the position and my 8% rule had been triggered and I reduced Exxon Mobil XOM for bookkeeping purposes, not because earnings are due this Friday. I never did get that tranche of ServiceNow NOW that I was trying to purchase when I had to cancel because I had mentioned the name in my work, as by the time that piece was published, the discount had vanished as that stock closed up on the day.

A Reset

So, semiconductors and some other AI-focused stocks were re-rated to a degree on Monday, but as mentioned above, U.S. equities did not take a broad beat-down. Heck, the Dow Transports closed up 1.46% on Monday as the KBW Banks gained 0.42%. Sure, the Nasdaq Composite was beaten for a loss of 3.07%, and the S&P 500 suffered a 1.46% smackdown, but smaller caps outperformed large caps in general. While the Russell 2000 gave back 1.03%, the S&P 600 only gave up 0.34%.

Breadth really wasn't terrible at all. Winners beat losers at the NYSE by a rough 4 to 3. Reread that sentence if you have to. Winners beat losers at the NYSE. Losers beat winners by a 3-to-2 margin at the Nasdaq. Advancing volume took a 48% share of composite NYSE-listed trade and a 36.1% share of Nasdaq-listed activity. Aggregate trade was higher for names listed at both exchanges, but remember, for a third time... winners beat losers at the NYSE. This is why we still do not yet have a "day one" bearish reversal of trend, despite consecutive red candles. Technically, the uptrend is still alive.

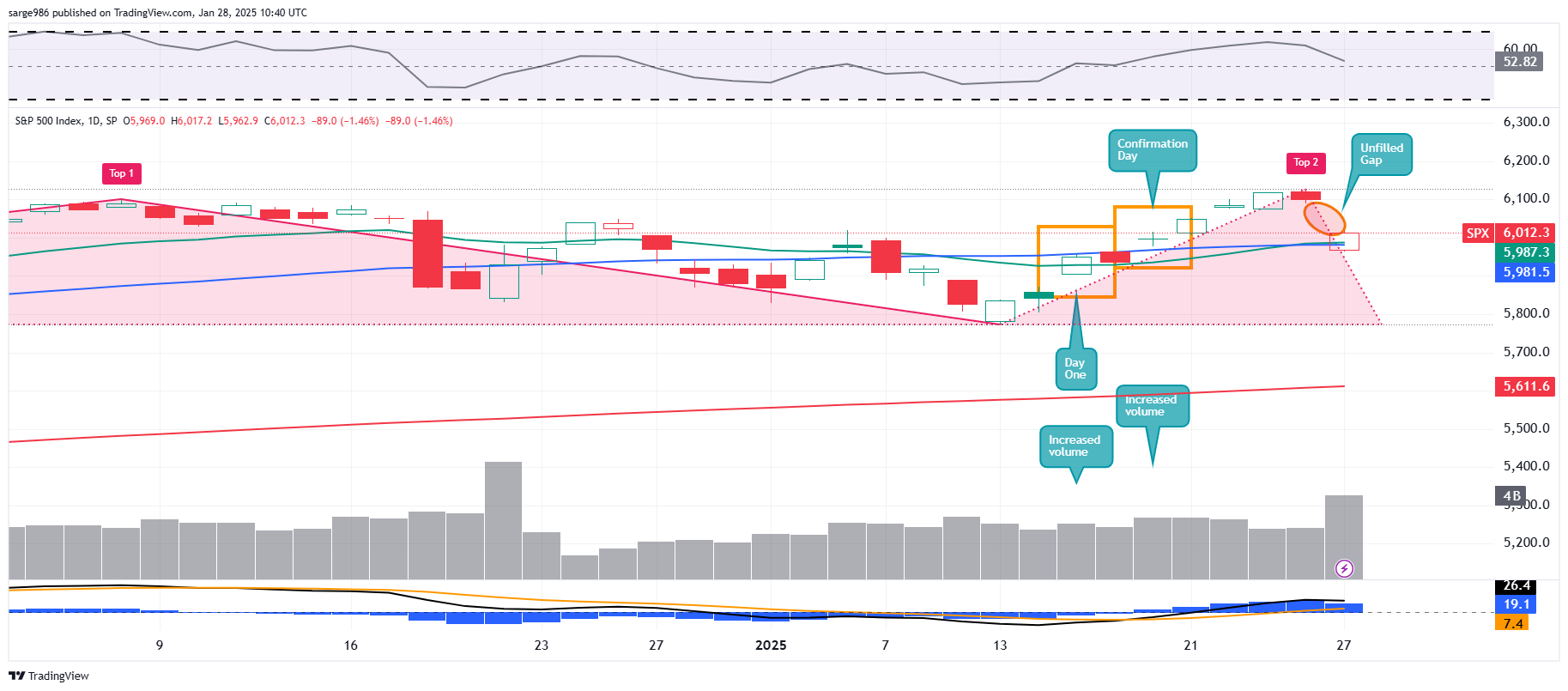

Charts

Readers will see that despite the increased trading volume, the S&P 500 left an unfilled gap in its wake, Relative strength is still better than neutral and all three components of the daily Moving Average Convergence Divergence are reflective of a market still in a bullish trend. Note, too, that the S&P 500 held on Monday above both its 21-day Exponential Moving Average and 50-day Exponential Moving Average. The S&P 500 is not really in bad shape just yet.

The Nasdaq Composite is obviously on much shakier ground. Not only did this index close below the low of its recent "day one" bullish reversal (though not below the low-point of that turnaround), it also gave up both its 21-day Exponential Moving Average, and its 50-day Simple Moving Average.

That put the swing crowd on edge, while forcing portfolio managers to reduce long-side exposure. The positive? The Nasdaq Composite still has not broken contact with its 50-day Simple Moving Average. The negative? The Nasdaq Composite appears to have found resistance on Monday at its 50-day Simple Moving Average.

Caution...

While I was a net buyer on Monday, I am fully aware that without a rally that resumes shortly, both of these major indexes still give the appearance of having put in a double top bearish reversal on Friday. That top needs to be taken out before its sets like cement. That's when the algos will recognize it as a bearish turn.

Is The Threat Real?

Well, DeepSeek's model is open-sourced, so we know it's not phony baloney. That said, how "good" or accurate it is, is not truly verified. How competitive it is beyond the consumer level, is also unverified. We really have no idea if the expense that DeepSeek claimed it took to train and develop the model is accurate, nor do we know if the number of and type of Nvidia chips claimed to have been used are accurate.

There is still a legitimate possibility that much more expensive U.S. models are considerably superior when put to a high-level test. It may be true that the gap between models is less than once thought and that elite level U.S.-designed chips, from Nvidia in particular, are grossly overpriced. Then again, take nothing for granted and trust not a soul. Until we know more.

There is still a legitimate possibility that much more expensive U.S. models are considerably superior when put to a high-level test.

There is always the chance that a technological disruption has truly occurred. This is not really a negative, as it will spur U.S. designers to engage in the fight and if there was a sense of complacency, it is certainly gone now. Either way, the probability for increased demand for AI chips probably only ramps higher from here. Even if margins will not be what they were, quantities sold could increase exponentially with the spread of those selling these chips significantly broadened or democratized.

Finally

On Monday, the U.S. Senate, in a 68 to 29 vote, confirmed Scott Bessent as the 79th Secretary of the U.S. Treasury. Twenty-nine "no" votes? Really? After what this department has been through for the past four years. Literally anyone with any kind of an economics background would likely be a step up.

All one would have to do is understand how to strategically plan for the duration of debt for the department to immediately show notable improvement, after it digs out from the hole that Bessent's predecessor left the Treasury in. Even if the legislature were to continue down its reckless fiscal path, which I hope it does not. Bessent assumes the job with the national debt at a rough $36.2 trillion and with the federal government having spent $711 billion more in fiscal 2025 than it had collected in revenue.

Defense Stocks on Tap This Morning

Go team. Rah!

Economics (All Times Eastern)

08:30 - Durable Goods Orders (Dec): Expecting 0.5% m/m, Last 0.4% m/m.

08:30 - ex-Transportation (Dec): Expecting 0.4% m/m, Last -0.1% m/m.

08:30 - ex-Defense (Dec): Expecting 0.4% m/m, Last -0.3% m/m.

08:30 - Core Capital Goods (Dec): Expecting 0.3% m/m, Last 0.7% m/m.

08:55 - Redbook (Weekly): Last 4.5% y/y.

09:00 - Case-Shiller HPI (Nov): Expecting 4.1% y/y, Last 4.2% y/y.

09:00 - FHFA HPI (Nov): Expecting 0.2% m/m, Last 0.4% m/m.

10:00 - CB Consumer Confidence (Jan): Expecting 105.9, Last 104.7.

10:00 - Richmond Fed Manufacturing Index (Jan): Expecting -8, Last -10.

4:30 p.m. - API Oil Inventories (Weekly): Last +1M.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: BA (?), GM (1.81), KMB (1.51), LMT (6.61), RTX (1.38), SYF (1.92), SYY (.92)

After the Close: CB (5.45), QRVO (1.21), SBUX (.67)

At the time of publication, Guilfoyle was long LMT, RTX, NVDA, AMD, CRM, PLTR, SOFI, XOM equity.