What Things Do People Invest In?

This is the third of ten investing basics articles and we'll cover the different kinds of things you can buy to create your own portfolio.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

This is the third of ten articles in the Filthy Rich Animal Investing Basics Series.

If you like what you see and haven't yet subscribed or would like to share with a friend, please visit this link. It's free!

I’ve been working out at OrangeTheory Fitness. I like it because the routine changes daily, with a mix of cardio, strength, functional exercises, and flexibility, so I'm never bored.

More importantly, these various forms of exercise are necessary to improve health and avoid injury.

You’ve probably seen people who just lift and do no cardio. They’re not exactly the picture of health.

The same is true for your investments.

You have to build a balanced portfolio. And that means diversifying, choosing securities from different asset classes.

Stocks, Bonds, Mutual Funds, and ETFs. What's the difference?

But first, let's get the jargon out of the way. Here are some definitions you need to know.

- A share of stock represents ownership in a company and often grants you the right to vote for directors and on important corporate events, like a merger with another company. An example is owning shares of Apple.

- A bond is a loan that you make to a company or government entity, which will be repaid back to you over time with interest.

- Mutual funds are professionally managed portfolios that may hold just one asset class, like stocks or bonds, or combinations of asset classes, like stocks and bonds.

- ETFs, or Exchange Traded Funds, are similar to mutual funds but can be bought or sold whenever the stock market is open and have the benefit of low expenses and taxes.

What is an asset class?

An asset class is a group of financial investments sharing similar characteristics, behavior, and regulations. The largest being stocks, bonds, or cash.

With some asset classes, like stocks, you can even go a level deeper. For example, large-cap U.S. stocks (companies like Apple) are a distinct asset class, as are emerging market small-caps or non-U.S. value stocks.

Commodities including gold, steel, wheat, and cattle, and real estate are alternative asset classes. They're hard to buy, unless you're a pro. But ETFs make it easier.

Bonds, aka fixed income, can be broken down into sub-classes like short-term, investment-grade corporate, or even emerging market bonds.

Crypto is an asset class, too, although it’s so new and prone to volatility that it should not be the largest holding in your investing portfolio.

Diversification lowers your risk while increasing your returns.

When you diversify across asset classes, you decrease your risk by spreading investments across different types of vehicles. Your college professor would tell you that your overall returns might even go up!

When stocks drop, bonds often rise, limiting losses you might have otherwise. So, when stocks rebound, you're already starting from a higher place than if you were only invested in stocks.

That's what a diversified portfolio does. It smooths your returns and mitigates volatility.

Less risk is a good thing!

Still not sure?

Here's an example. You know the story of the race between the tortoise and the hare? The hare is so confident that he naps just before the finish line... and loses to the slow tortoise!

Stocks are like the hare. Stocks usually outperform the slow-moving, tortoise-like bonds. Now, bonds may be slow, but they don't nap. Stocks, on the other hand, can have multi-year periods where they don't do so well.

Combine the tortoise and the hare, and you've got a winning combination that never sleeps.

Diversification: It's not how many funds you own, it's what's in them that matters.

Some people think that when it comes to diversifying, the more ETFs they buy, the merrier their portfolio will be. But that's not accurate.

Imagine that you could bet on the outcome of a race that featured five different tortoises and five different hares. You might think that placing bets on three of the hares made you diversified. But one tortoise might still emerge victorious. As we all know, every hare loves a good nap! You need to own a tortoise AND a hare.

Diversification is about having exposure to all of the important asset classes.

The 60/40 Portfolio

A simple example of traditional diversification is the 60/40 portfolio. It holds 60% stocks and 40% bonds.

Sure, you could simply buy two ETFs, one that held stocks and one that held bonds.

Or, you could get additional diversification by being more granular with each asset class and buying different ETFs that gave you access to different types of securities within those asset classes.

Here's an example with eight asset classes and an ETF that represents each. Keep in mind, this is an illustration, not a recommendation. There are plenty of other ways to effectively slice and dice a 60/40 portfolio.

Stocks 60%

- 18% Large-Cap U.S. Stocks: SPDR S&P 500 ETF (SPY)

- 10% Mid-Cap U.S. Stocks: iShares Core S&P Mid-Cap ETF (IJH)

- 7% Small-Cap U.S. Stocks: iShares Russell 2000 ETF (IWM)

- 10% Developed Markets (Non-U.S.) Stocks: Vanguard FTSE Developed Markets ETF (VEA)

- 5% Emerging Markets Stocks: Vanguard FTSE Emerging Markets ETF (VWO)

- 10% Real Estate Investment Trusts (REITs): Vanguard Real Estate ETF (VNQ)

Bonds 40%

- 25% U.S. Treasury Bonds: iShares 7-10 Year Treasury Bond ETF (IEF)

- 15% Investment-Grade Corporate Bonds: iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD)

This portfolio combines U.S. stocks, international stocks, and bonds to balance growth potential with stability, keeping diversification across sectors and regions.

In your retirement portfolio, it’s generally best to keep things simple. This isn’t the same as “buy and hold,” which isn’t necessarily a great idea all the time.

It’s OK to use an allocation similar to the one above and supplement using specialized ETFs, such as those tracking commodities or real estate.

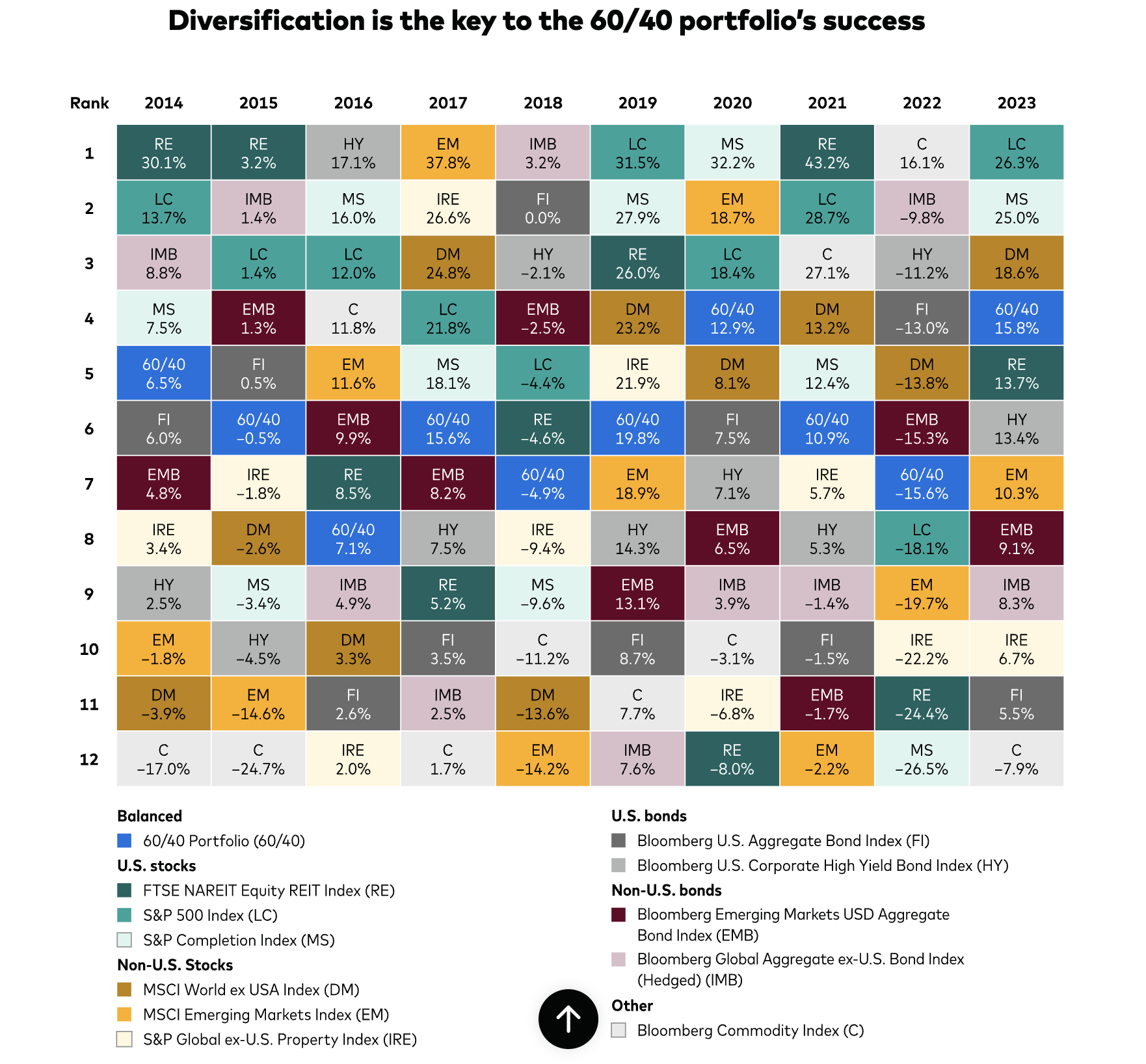

Here's an example from Vanguard of how a 60-40 portfolio has performed vs different asset classes. Notice how RE, real estate is sometimes the best performer and sometimes the worst? But 60/40 just chugs along. It doesn't make money every year, but it's relatively stable.

You might wonder if I’m anti-mutual funds since I keep mentioning ETFs. I’m not, but I generally prefer the lower costs and ease of trading ETFs. You’ll find plenty of mutual funds that can be part of a balanced, diversified portfolio.

If you have a 401(k) at work, mutual funds are probably your only investment option. That’s ok, just don’t make the common mistake of only investing in the funds with the best recent returns. That leads to a concentrated portfolio that might do poorly during the next downturn.

Too much hare and no tortoise.

Keep in mind your reason for long-term investing: It’s not about nabbing the highest return, which requires taking more risk. Instead, it’s about generating the return you need to fund your retirement without outliving your money.

Thanks again for reading and if you haven't yet subscribed or would like to share with a friend, please visit this link. It's free!