Weaker Dollar Could Be Welcome as Fed and Treasury Take Tandem Approach

As the Fed and Treasury seem to work together to lower yields, the Trump administration could be rooting for a weak dollar.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I will spend a few minutes on the Federal Reserve because it is pretty much obligatory ahead of the FOMC, though hopefully my view has been quite clear.

I got to cover a lot of topics that generated a lot of feedback on Wednesday morning on Bloomberg TV (Academy’s segment starts at the 6:45 mark).

A Fed Surprise?

I have been fixated on ways the Fed and Treasury could “surprise” the market by working together to lower yields across the curve (not just fed funds). One of our August interviews got condensed into a smaller clip, "Focus On Long End of the Curve, Not Fed Cuts: Tchir."

Currently, according to WIRP, the market is pricing in 1.04 cuts at this meeting, 1.9 cuts in October, and 2.8 cuts by the end of the December meeting.

That seems a touch low.

I remain in the 75-BPS-to-100-BPS-cut camp for the year, so there is room to price in a higher probability of four cuts this year than the market currently has priced in.

For this meeting, I see a 0.00001% chance of no cuts (I guess there is always some possibility), but only a 60% chance of 25 BPS, with a 40% chance of 50 BPS. Actually, I only view it as a 25% chance, but this seemed like a good opportunity to dig up a fun report in The Wall Street Journal that we were involved with: "How Do Pundits Never Get It Wrong? Call a 40% Chance" 😊.

The market doesn’t seem to be prepared for a big shift to the dovish side. I think a bigger cut than 25 BPS has a real shot, and that the dots could surprise with more cuts occurring sooner.

My assumption is there are always some people who don’t have a strong opinion, and for ease, just adopt the consensus and/or the recommendation of the leader. So, Chair Powell had what seemed like more support, or conversely, less obvious dissent than really existed.

With the tide changing at the Fed, and other voices gaining strength as we prepare for a new chair, it seems reasonable to assume some of those who just followed along as hawks will now follow along as doves — impacting the messaging.

Any mention of “additional” measures does not seem priced in at all.

It is probably too early to mention that things like another Operation Twist are on the table (Operation Twist is where the Fed sells shorter-term bond holdings to buy longer-maturity bonds).

The Treasury Department announced Increased buybacks. This fits with my theme of a “tandem” approach to managing the yield curve. Where the Treasury and Fed work in conjunction with each other to complement their tools. This helps contain the longer end of the curve, and also likely generates some revenue to create lower deficits (I haven’t confirmed this, but to the extent they are buying bonds below par and retiring them, there should be an accounting gain).

It's probably a touch early for Powell to address some non-traditional programs (though they now seem pretty standard), but even after recent flattening, you seem to be getting this potential option very cheaply. Though maybe he could admit that changes in short-term rates are not as effective (of a policy tool) as they once were.

Finally, we are seeing rate cut expectations increase, while curves flatten for two other reasons, which I’ve mentioned before:

- By having so many credible candidates for the Fed discuss their views, almost all being more dovish than Powell has been, it makes it seem less “egregious” or even “normal” to cut (we were in the “should cut in July camp” but that view has gone from potentially being accused of being politically motivated, to validated by the data).

- Cuts justified by weak economic data (jobs) do not force the curve steeper.

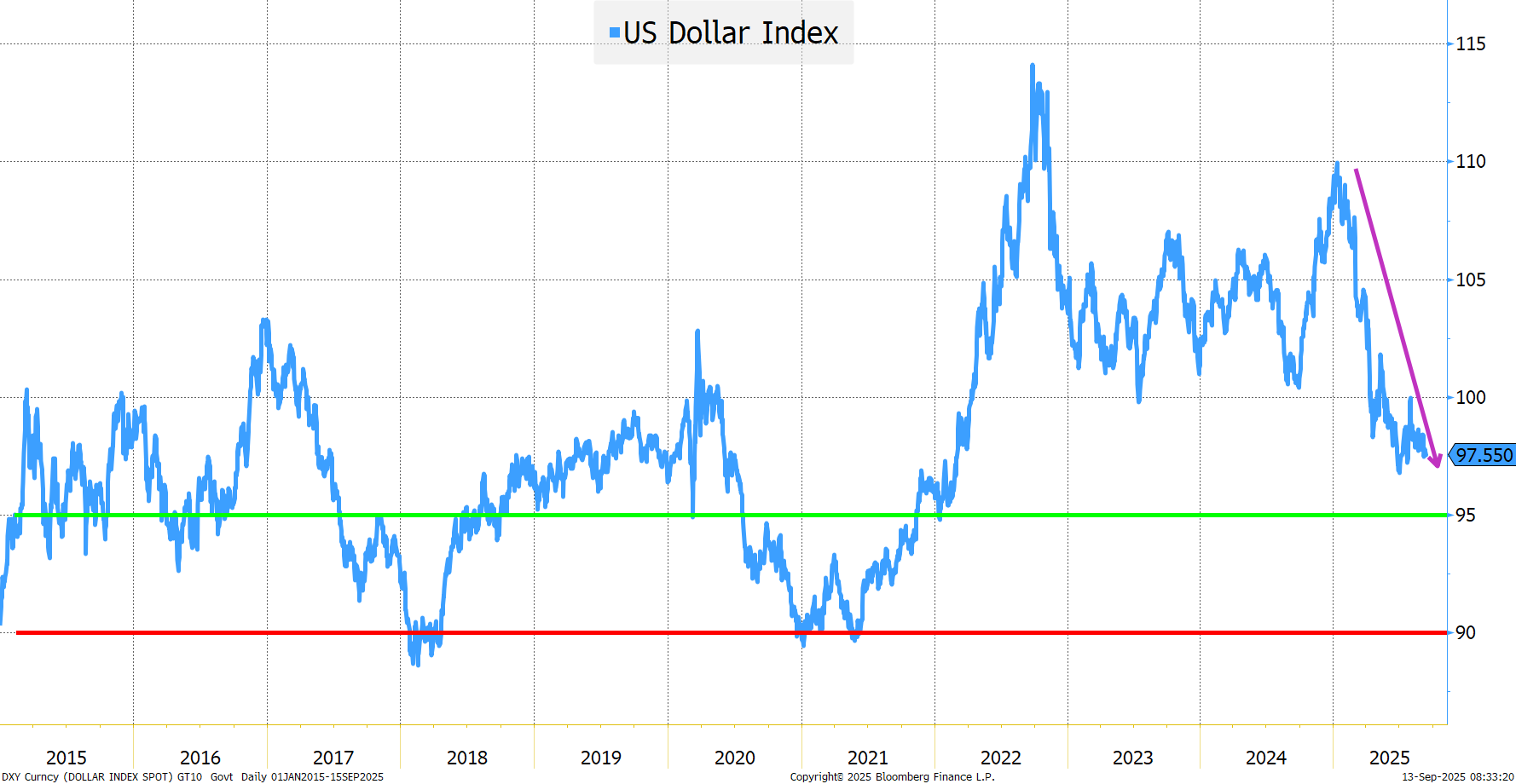

The corollary, or counterpoint, or outlet of this view is a weaker dollar. We could see a break below 90 on DXY. Given the administration’s desire to reduce imports and increase exports, a weaker dollar would likely be viewed (behind closed doors, because we “cannot” publicly say we have a weak dollar policy) as a feature and not a bug.