Warsh Clears Hurdle, Earnings Bonanza Ahead, Econ Data Deluge

Following a wild weekend and another threat to Trump, all eyes now on Iran; earnings including Apple, Meta, Google; and big economic data.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Sunrise Along Shore

All life leaps out to greet the light —

The shining sea-gulls dive and soar,

The swallows whirl in dizzy flight,

And sandpeeps flit along the shore.

From every purple landward hill

The banners of the morning fly,

But on the headlands, dim and high,

The fishing hamlets slumber still.

- Lucy Maud Montgomery (1901)

What a Weekend, What a Week Ahead....

Equity index futures opened lower on Sunday night. As Asian equities traded higher and then European equities opened rather flattish, U.S. equity index futures moved higher as well. Not that the weekend wasn't eventful. The headline grabber over the weekend was the unprecedented third assassination attempt against a U.S. president. What made this attempt so very dangerous was the fact that five of the top six officials in the presidential line of succession were in attendance at the White House Correspondents' Association Dinner in Washington on Saturday evening.

Cole Allen, an apparently lone gunman from Torrance, California armed with a shotgun, a handgun and knives, who had traveled by rail across the country and had stayed at the hotel where the dinner took place, had carefully planned out how to conduct his attack. Investigators have discovered a 1,000-word document left by Allen where he had outlined security at the hotel showing how to get firearms into the building.

Allen, a teacher with obvious problems, will likely be charged on Monday morning after having shot a law enforcement officer who has since been released from the hospital. The officer was thankfully wearing a bullet-proof vest. King Charles of Great Britain is scheduled to visit Washington on Monday. That visit will proceed as planned.

Get er' Done

Over the weekend, Republican Sen. Thom Tillis announced that he will be dropping his blockade of Kevin Warsh's advancement through the Senate confirmation process to become Chairman of the Federal Reserve bank. The catalyst was the dropping by the Department of Justice of the criminal investigation of Powell connected to refurbishments of the central bank's properties in Washington, D.C. that had run significantly over budget.

Tillis, who had opposed the criminal investigation, had the power to keep Warsh's nomination at the committee level and prevent a vote at the senate-wide level. Jerome Powell's term at the helm of the nation's central bank expires on May 15. Powell, who had a very rocky relationship with Pres. Trump, was not renominated to continue in that position. There is a possibility that Powell could stay on as a member of the Fed's Board of Governors into early 2028.

After learning that the criminal probe had been dropped, Tillis said, “With these assurances, I look forward to supporting Kevin Warsh’s confirmation. He is an outstanding nominee, and it is time for the Federal Reserve to move beyond this distraction and return its full attention to its mission.”

The War

Market, last week, finally appeared to dismiss concerns of the conflict in Iran. Financial markets seem to have either priced in a lasting peace or at least seem to believe that the Strait of Hormuz will reopen safely to the passage of commercial seafaring vessels. Axios reported on Sunday evening that whoever is in charge in Iran had made a new peace offer to the U.S.

The new proposal would reopen the Strait and extend the existing ceasefire so that the parties involved can work toward a permanent end to the war with talks concerning Iran's nuclear weapons program also coming later. Pres. Trump has indicated that he will meet with national security and foreign policy officials on Monday to discuss a response. A White House spokesperson said, “As the President has said, the United States holds the cards and will only make a deal that puts the American people first, never allowing Iran to have a nuclear weapon.”

The Past Week...

The S&P 500 and Nasdaq Composite, among other domestic equity indexes, dealt with some turbulence, but still managed to post a fourth consecutive winning weekly candlestick. The continued positivity was driven by optimism for the reopening of the Strait of Hormuz, a first quarter earnings season that continues to impress and another slate of macroeconomic data that has easily outperformed expectations. March retail sales that roared were the big-ticket item this past week for economists. The semiconductors were the stock market stars last week as Arm Holdings (ARM) and Advanced Micro Devices (AMD) . gained 40% and 24.9% respectively over the five-day period. Intel (INTC) gained 23.6% on Friday alone.

Week Ahead

What matters moving forward...

- The Situation in Iran: This is still the most important item under the microscope, if something goes wrong. As long as the market senses progress, this situation seems to have been moved by investors to the back burner.

- Macro: This will be a fairly heavy week for the release of domestic macroeconomic data. The headline release will probably be March personal consumption expenditure inflation data on Thursday morning along with personal spending and personal income for that month. On the way there, we'll run through February home prices on Tuesday morning along with the Conference Board's April survey for consumer confidence. On Wednesday, March durable goods orders will cross the tape as will data for housing starts and building permits for the months of February and March. Finally, on Friday, the results for the ISM manufacturing index (PMI) for April will be published.

- The Federal Reserve: The Federal Reserve's Federal Open Market Committee will make a policy decision on Wednesday that will culminate with an official statement and press conference that afternoon. This is usually a big deal, but with near certainty that this will be Jerome Powell's final appearance as Fed Chair, markets may just shrug off anything he has to say that sounds like opinion.

- Earnings: First-quarter earnings season is well under way and this will be a very heavy earnings week full of high-profile reports. Reporting on Monday morning will be Domino's Pizza (DPZ) and Verizon (VZ) . On Tuesday morning, we'll hear from Coca Cola (KO) , General Motors (GM) , Spotify (SPOT) , and United Parcel Service (UPS) to be followed by Robinhood (HOOD) , Seagate (STX) and Starbucks (SBUX) on Tuesday afternoon. Wednesday gets really hot. Ahead of the opening bell, SoFi Technologies (SOFI) will report. After the close, Amazon (AMZN) , Alphabet (GOOGL) , Meta Platforms (META) and Microsoft (MSFT) will go to the tape. Come Thursday, Caterpillar (CAT) , Eli Lilly (LLY) , Merck (MRK) , Apple (AAPL) , and SanDisk (SNDK) will all post their quarterly numbers.

Related: Liftoff or Top? Looking Back at History to Understand Today.

The Week That Was...

U.S. financial markets posted a fourth consecutive winning week going into what was a weekend that likely rattled a few cages....

- The S&P 500 gained 0.8% on Friday and 0.55% for the week.

- The Nasdaq Composite added 1.63% on Friday and 1.5% for the week.

- The Nasdaq 100 tacked on 1.95% on Friday and 2.37% for the week.

- The Russell 2000 gained 0.43% on Friday and 0.36% for the week.

- The S&P Small Cap 600 gained 0.56% on Friday and 0.67% for the week.

- The S&P Midcap 400 added 0.22% on Friday but lost 0.14% for the week.

- The Dow Transports lost 0.94% on Friday and an ugly 6.82% for the week.

- The Philly Semis soared 4.32% on Friday and a stunning 10.02% for the week.

- The KBW Bank Index surrendered 1.34% on Friday and 1.2% for the week.

On Friday, just four of the eleven S&P sector SPDR ETFs closed out the session in the green. The winners were obviously led by technology (XLK) , while communication services (XLC) and health care (XLV) led the losers.

For the week, five of the eleven S&P sector SPDR ETFs closed out the session in the green. The winners were led again, by technology, but also energy (XLE) . Health care and communication services were again, the big losers.

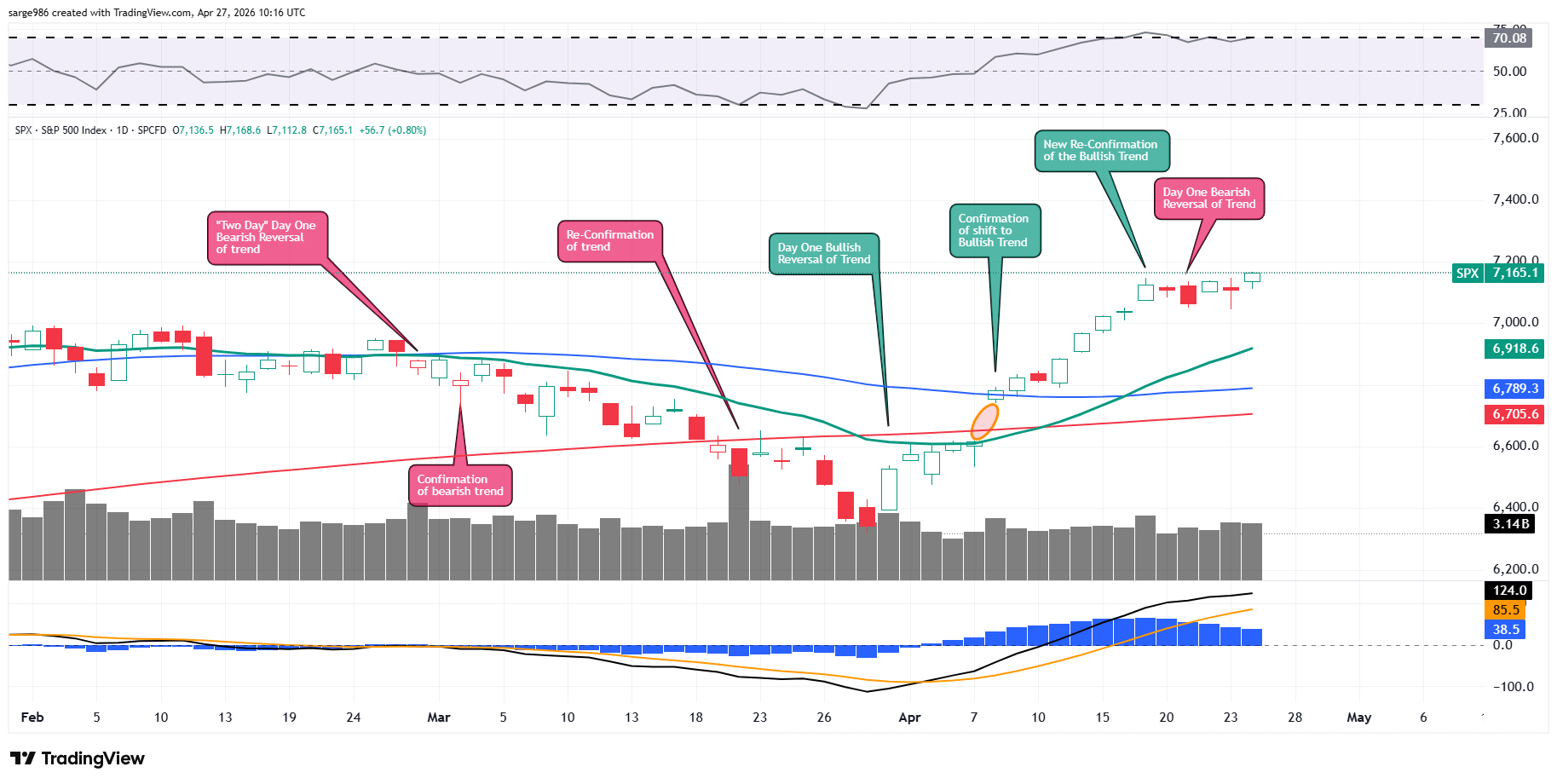

The Chart

The S&P 500 made a low on Tuesday that canceled out the reconfirmation of the bullish trend on Friday the 17th. The index then made a high on Wednesday that canceled out any shot at a confirmation of bearish trend reversal that Tuesday's "day one" had presented. The index closed out the week sort of trendless but moved in generally positive direction on Friday.

The indicators are all still rocking. Relative strength is now scraping up against a technically overbought state and has been for two weeks now. The daily moving average convergence divergence has now moved into an overtly bullish posture and sustained that set-up with all three components looking quite positive, also for two weeks now.

Earnings

As of April 24, according to FactSet, for the first quarter, Wall Street now expects to see year-over-year blended (results & expectations) earnings growth for the S&P 500 of 15.1%, up from 13.1% last week, and up from 11.6% more than a month ago. Wall Street also sees revenue growth of 10.3%, up from 9.9% a week ago. With 28% of the S&P 500 having reported, 84% of companies have beaten earnings expectations, while 81% have beaten sales projections.

For the full year of 2026, Wall Street now looks for earnings growth of 18.6%, up from 18% last week, and up from 14.7% more than a month back, on revenue growth of 9.5%, up from 9.2% last week and up from 7.7% more than a month ago. The outlook for the second quarter also continues to improve quite dramatically. Second quarter earnings growth is now estimated at 20.6%. No joke.

At the moment, the Technology sector is projected to have grown earnings a stunning 46.3% for the first quarter with the materials in second place at growth of 33.1%. Three sectors, health care, communication services and energy are projected to have suffered a Q1 earnings contraction. Still, according to FactSet, corporate profit margins at the S&P 500 level are now running at fifteen-year highs. Not exactly the weak economy you were told to expect, is it?

Valuation

Still using data provided by FactSet, the S&P 500 ended last week trading at 20.9-times 12 months' forward-looking earnings, even with last week, but still down from 21.6-times more than a month prior. This is above the five-year average of 19.9-times for the index as well as being well above its 10-year average of 18.9-times.

The S&P 500 also ended last week trading at 28.1-times trailing 12 months' earnings, up from 27.8-times one week ago, and above levels that the index reached more than a month ago. This also stands well above the five-year (24.6 times) and ten-year (23.3 times) averages for the index.

Ten of the 11 sectors are now trading above their five-year average valuations, led by the discretionaries (28.2 times), the industrials (25.8 times) and technology (23.8 times). Only health care closed out last week undervalued relative to its five-year norm.

Fed Funds Futures

Fed Funds futures trading in Chicago are currently pricing in a 100% probability for no change to be made to the target range for the Fed Funds Rate at the next FOMC policy meeting this Wednesday. There are no rate hikes priced in at any point in the future looking out towards year's end 2027.

That said, there are still no rate cuts priced in for calendar year 2026. In fact, no cuts are priced into these markets until September of 2027. Understand, though, that we can expect that everything will change several times over, as the year progresses, especially as the midterm elections approach. These numbers could change as well as leadership at the central bank is passed from a Chair that had an antagonistic relationship with the Trump administration to one far more comfortable with expected pressure to reduce short-term interest rates.

Economics

(All Times Eastern)

10:30 - Dallas Fed Manufacturing Index (Apr): Expecting -0.8, Last -0.2.

The Fed

(All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: (DPZ) (4.27), (VZ) (1.21)

After the Close: (CDNS) (1.89)

At the time of publication, Guilfoyle was long AMD, SOFI, AMZN equity.