U.S.' Stealth Attack on Iran, Trump's Verbal Attack on the Fed, My Take on the Charts

Let's see what just happened over the weekend, what could happen next from Tehran and what's ahead on the market calendar.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It began at 12:01 ET on Saturday morning when a group of B-2 stealth bombers made by Northrop Grumman NOC made a show of launching from Whiteman Air Force Base in Missouri and flew west toward the Pacific Ocean and toward Guam, very visibly refueling in the skies near Hawaii. The strike force of seven B-2 bombers slipped away from the larger group unnoticed, to fly east over the Atlantic Ocean strictly adhering to radio silence, or at least only minimally communicating and began a more than 18-hour flight to the target area.

Readers only have to look back to Friday morning's Market Recon column right here at TheStreet Pro. I commented on Karoline Leavitt's words that Pres. Trump would make a decision on taking military action in Iran "within the next two weeks." I wrote:

"While it is true that this president through four plus years of leadership has proven to be a president that prioritizes peace much more so than probably any other president in my lifetime, it is also true that if I knew that I was going to punch you in the mouth in the next few minutes, I would probably act like I had no interest in fighting. Until I thought you relaxed your guard."

Turns out that at least when it comes to taking offensive to deter something far worse, this president and I think a little bit alike, because that's exactly what he did this weekend. The bombers were refueled multiple times throughout a mission whose round-trip flight would run more than 36 hours. As the strike force entered the area of responsibility for CENTCOM, they were linked up with F-22 fifth generation stealth fighters by Lockheed Martin LMT and F-35 fifth generation stealth fighters (Lockheed Martin) for protection and to be used as decoys. F-16 fourth generation (Lockheed Martin) and F-15 fourth generation Boeing BA fighters provided cover as well. "Operation Midnight Hammer" was underway.

Seventeen hours after the aircraft left the base near Kansas City, a U.S. Ohio-class Submarine by General Dynamics GD surfaced more than 400 miles away from the intended impact area and fired approximately 30 Tomahawk land attack cruise missiles (made by RTX RTX toward their target. About 100 minutes after that, or 18 hours and forty minutes after takeoff, the lead B-2 bomber dropped two GBU-57 Massive Ordnance Penetrator Weapons better known as bunker-busters (Boeing) on the Iranian nuclear installation at Fordow.

Twelve bunker busters in all would hit their marks at Fordow, while an additional two scored bullseyes at the installation at Natanz. A short while later, the Cruise missiles struck paydirt at Isfahan. The aircraft involved then exited Iranian airspace, the bombers headed back to Missouri, the fighters back to their stations. Incredibly, as far as we know, Iranian air defense never even saw the U.S. aircraft and were still trying to figure out what had happened even as those aircraft had all exited the area of operations.

Really, a Good Job ...

I don't like to give the U.S. Air Force and U.S. Navy a ton of credit. I don't need their egos growing out of control. Readers, I'm just kidding about that. This was a job extremely well done. The flight crews on those bombers count just two. The only way a seven-aircraft, two-person-per-craft crew could possibly fly a nearly 37-hour mission, coordinating with 125 fighter and support aircraft along the way, while also coordinating with the surface fleet, all while also avoiding open, intercept-able channels of communication is just incredible.

That takes training. Tons of training and an absurd level of discipline. I like to make fun of our friends in the services who don't sleep outside and don't dig foxholes, but this was an elite level of execution. Nice job to all, even you squids. On a personal note, I lost my best friend from infantry school back on October 23, 1983. He was in Beirut on that awful day. I wore something written on my helmet in remembrance of him for the rest of my first stint in the military. You can use your imagination.

I think of him as I write this piece. Forever young. Killed at age 19, when his barracks collapsed. Here I am in my 60s. That kid bought a broom at a convenience store in Jacksonville, North Carolina, so he could keep our barracks clean even when we were off duty and the cleaning gear was locked up. Who does that? What a nice guy.

Immediate Aftermath

Iranian state media had reported on Sunday that Iran's parliament had voted to close the Strait of Hormuz. But the final decision in that government does not lie with their parliament. Iran's national security council gets the final say. A rough 20% of the planet's consumption of crude oil passed through those waters in 2024, plus about a third of the planet's consumption of liquified natural gas.

It would probably be a huge mistake economically for Iran to close those waters as that would hamper China's ability to purchase oil from Iran and China is Iran's best customer. On Sunday evening, crude oil opened higher but was not nearly as strong as some had feared earlier in the day. US equity index futures opened on weakness on Sunday evening, but also to the surprise of some, not nearly the level of weakness that some had expected.

As I work through the zero-dark hours on Monday morning, WTI Crude is actually flat from where it went out on Friday afternoon and US equity index futures are up slightly. European equities have also opened slightly higher.

The Week Past

Stocks, in general, closed lower, but not tremendously so on Friday on elevated triple-witching expirations trading volume. This exacerbated losses that were already in place across most of our mid-major to major equity indexes. Treasury yields worked their way lower throughout the week as the U.S. Ten-Year and Two-Year Notes paid 4.38% and 3.9% respectively at week's end. The U.S. Dollar Index also strengthened last week. This came in response to the Federal Open Market Committee policy meeting that culminated on Wednesday.

Actually, the move higher for the dollar was probably more in response to the "more patient than many would like to see" approach that Fed Chair Jerome Powell seemed to take during the post-statement press conference. We've already discussed the lack of consistency in Powell's application of monetary policy according to his own standards. Powell has been at times, data-dependent when it suits him or the committee, and at other times, completely forgoing data-dependency in anticipation of a potential burst of inflation that could come at some point down the road.

What Trump Really Thinks ...

This inconsistency in the application of policy has infuriated the sitting president. Pres. Trump again criticized the Fed Chair last week, posting "If he reduced (rates) to the number they should be, 1% to 2%, that 'numbskull' would be saving the United States of America up to $1T per year." to social media. The president then added, "I don't know why the Board doesn't override this Total and Complete Moron! Maybe, just maybe, I'll have to change my mind about firing him? But regardless, his Term ends shortly!" Wow. Tell us how you really feel.

Meanwhile...

On Friday, Fed Gov. Christopher Waller, who President Trump nominated to the Board of Governors during his first term, apparently has decided to audition for the top spot at the central bank. On CNBC, in a morning interview, Waller said, "I think we're in the position that we could do this (cut rates) and as early as July. That would be my view, whether the committee would go along with it or not."

Waller explained himself: "Why do you want to wait until we actually see a crash (in labor markets) before we start cutting rates? So, I'm all in favor of saying maybe we should start thinking about cutting the policy rate at the next meeting, because we don't want to wait till the job market tanks before we start cutting the policy rate." I don't have any inside info, but that sounds like an audition if I ever heard one.

At The Moment

Fed Futures markets trading in Chicago are pricing in an 86% probability that no rate changes come out of the July 30 FOMC policy meeting. There is however, a 70% likelihood being priced in that a quarter-percentage point rate cut is implemented on September 17th and a 71% probability priced in for a second quarter-point rate cut by year's end.

The GDP Game

Last week, the Atlanta Fed revised their GDPNow model for the second quarter down to growth of 3.4% from growth of 3.8% (q/q, SAAR). There is still no estimate for Q2 GDP ex-the gold trade at this time, nor do I expect that there will be one for the period. Among other regional central bank district branches running close to real-time GDP models, the New York Fed's estimate for Q2 growth now stands at 1.91%, down from 2.34%, while the Cleveland Fed still sees Q2 growth of 1.97%. As mentioned last week, this estimate has not budged in weeks.

The St. Louis Fed left their estimate for Q2 GDP revised at growth of 1.46%. As readers can see, there is still nothing even remotely close to a consensus view across the regional Federal Reserve Q2 GDP models available to us, but it does seem that the numbers are trending lower. Where is my trusted Hedgeye Nowcast Model?

They are the only ones that have been consistently close, not just on GDP, but also on inflation, which is why I pay them. After literally nailing the BEA estimate for Q1 GDP, Hedgeye's model for the second quarter is now running just above 1.7%.

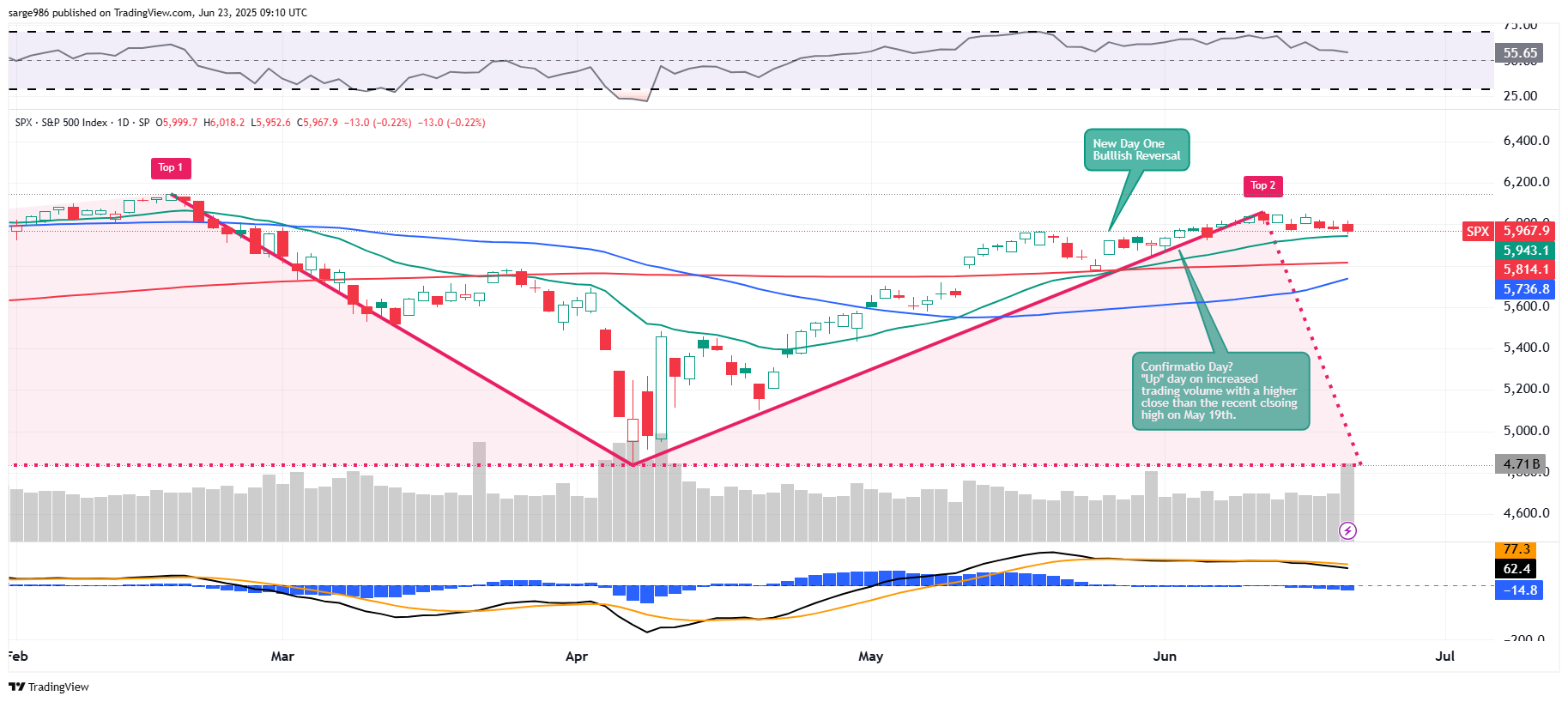

The Chart...

Readers will see that this Double Top pattern of bearish reversal is still intact after last week's mild selloff. Do the markets take a hit in response to the military activity over the weekend and in anticipation of an attack by Iran or Iran's proxies against Americans? Or will there be a relief rally perhaps in response to the fact that one of the most dangerous and belligerent regimes on the planet has been seriously weakened?

Both outcomes are at this time possible. We have not seen a "day one" change in direction nor a "confirmation day" since very early June as added to the chart here...

That means that the general trend for this market is still to the upside, until we see lows below where the index traded at that time. On that note, the daily Moving Average Convergence Divergence for the S&P 500 did start showing increased weakness late last week.

What's Ahead?

The week ahead will be an active one, despite that there will not be a lot of corporate earnings to take in.

- Obviously, geopolitical concerns remain front and center. Does Iran respond militarily? Will Iran's proxies respond? Do the hundreds (or possibly thousands) of Iranian nationals that crossed the southern border from Mexico illegally between 2021 and 2024 contain sleeper cells? This concern is considered to be extremely likely by a number of intelligence community professionals. We have no way of knowing for sure. Americans, the federal government and American businesses will also have to be vigilant whereas the likelihood for cyber attacks initiated by Iranian interests has now increased exponentially.

- The domestic macroeconomic calendar remains active this week. The headline events on the macro side will be May Durable Goods Orders on Thursday, the final revision to Q1 GDP growth on Thursday and May personal consumption expenditure data on inflation on Friday. This morning, we'll see the manufacturing and service sector flash PMIs for June. As far as the U.S. consumer is concerned, the Conference Board will publish their confidence survey for June on Tuesday, while the University of Michigan will revise their June survey on sentiment this Friday.

- The Federal Reserve will be out and about this week, now that the media blackout period going into last week's policy meeting is over. The main event here will be Fed Chair Jerome Powell who will testify before the House Financial Services Committee and the Senate Banking Committee this Wednesday and Thursday. Ahead of those events though, Fed Gov. Christopher Waller, who is rising as an obvious rival to Powell, will speak on both Monday and Tuesday.

- The earnings calendar is extremely light again this week. That said, this week, we will be hearing from a few headline level names. On Tuesday afternoon, FedEx FDX will report. On that note, the company's legendary founder and former U.S. Marine (always faithful) passed away on Saturday at the age of 80. On Wednesday, General Mills GIS reports ahead of the open and Micron Technology MU reports after the closing bell. Finally, on Thursday, we'll hear from McCormick MKC in the a.m. and we'll hear from Nike NKE in the p.m.

Economics (All Times Eastern)

09:45 - S&P Global Manufacturing PMI (Jun-Flash): Expecting 51.2, Last 52.

09:45 - S&P Global Services PMI (Jun-Flash): Expecting 52.9, Last 53.7.

10:00 - Existing Home Sales (May): Expecting 3.95M, Last 4M SAAR.

The Fed (All Times Eastern)

03:00 - Speaker: Reserve Board Gov. Christopher Waller.

10:00 - Speaker: Reserve Board Gov. Michelle Bowman.

1:10 p.m. - Speaker: Chicago Fed Pres. Austan Goolsbee.

2:30 - Speaker: Reserve Board Gov. Adriana Kugler.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: CMC (.85), FDS (4.30)

After the Close: KBH (1.46)

At the time of publication, Guilfoyle was long NOC, RTX equity.