U.K. Fancies a Trade Deal, Fed's Unsure, Trump Rewrites Chip Policy

Let's check on the latest in tariff talks, the Fed statement and Trump's shift on a Biden-era AI chip policy.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

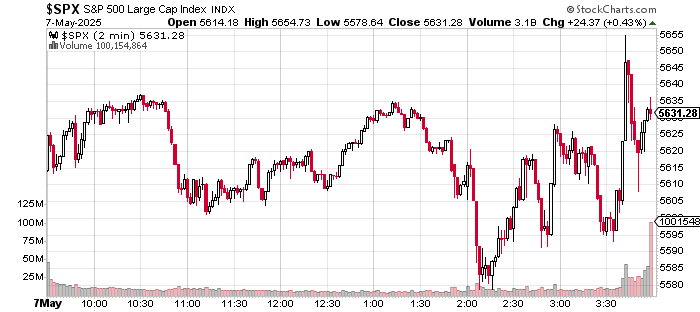

Wednesday afternoon: The Federal Open Market Committee policy statement had just been released at 2 p.m. ET. Equity markets sold off almost immediately. Just a few minutes later, the S&P 500 among other equity indexes would tick at their nadir for the regular session. There were just a couple of ominous words in that statement and the high-speed, keyword-reading algorithms that control price discovery in 2025 picked up on them instantly.

It was 30 minutes later that Fed Chair Jerome Powell took to the podium and answered questions posed by the financial media. Powell did not sound like a policy hawk, nor did he sound dovish. He did sound like he did not exactly know what to do in this environment. While that may cause a reaction of disgust among some who want action immediately, it was also in a way, refreshingly honest.

Powell did not sound as if he and his committee were not open to acting in one way or the other, should the risks to the Fed's dual mandate in regard to supporting both maximum employment (of the economy, not labor market employment) and stable pricing become imbalanced. The news that hit the tape after Powell concluded his press conference, was generally positive concerning trade. Markets reacted in positive fashion going into the closing bell. Subsequently, U.S. equity index futures traded higher overnight.

Readers will note the bottom tick for the S&P 500 just after 2 p.m. ET on this Wednesday chart of the S&P 500. Note as well, the visible algorithmic support that underlines the action from roughly 2:10 p.m. into the 4 p.m. ringing of the bell.

The Statement

The Federal Open Market Committee statement makes readers aware of increased risk. The phrase "Although swings in net exports have affected the data" has been added to the first sentence that concludes with "...recent indicators suggest that economic activity has continued to expand at a solid pace." This informs the public that there are new risks.

The continued use of the word "solid" here surprised me a little and implies to me that Fed officials also saw the glaring (or missing) hole in the consumption+inventories portion (or reduced from the net exports or imports) side of the ledger in last week's gross domestic product report. This will have to be corrected upon revision and could very well return the headline first-quarter print to positive territory. Readers will recall that last week, I had written that there was a problem in the BEA's mathematics, and the formula used to determine GDP had been skewed.

The FOMC reiterates the heightened risks, adding the phrase, "and judges that the risks of high unemployment and higher inflation have risen" to the previously benign quote that "The Committee is attentive to the risks to both sides of its dual mandate". The rest of the statement is a "cut and paste" job lifted from previous statements. This portion simply informs that the target range for the Fed Funds Rate will remain 4.25% to 4.5% and that the Fed's quantitative tightening program, withdrawing excess liquidity from the economy and reducing the central bank's balance sheet will continue as planned.

The Press Conference

Fed Chair Jerome Powell came across as non-committal as possible on Wednesday, which was by design. His intent was clear and that was to publicly preserve central banking optionality whereas monetary policy is concerned. He laid out the same warning that was evident in the statement... "If the large increases in tariffs that have been announced are sustained, they're likely to generate a rise in inflation, a slowdown in economic growth, and an increase in unemployment."

On the future of short-term interest rates, Powell used the term "wait and see" eleven times during the press conference. The Fed Chair was quoted in the Wall Street Journal as saying, "We don't feel like we need to be in a hurry. We feel like it's appropriate to be patient." Then, Powell threw the stock market a bone... "When things develop, of course, we have a record of - we can move quickly when that's appropriate." The algos loved that line.

Trade News

There is some supposedly good news on trade that started breaking on Wednesday afternoon and continues to have a positive impact on U.S. equity index futures as the zero-dark hours speed by and the man in the blackened window fades. For one, U.S. Treasury Secretary Scott Bessent and U.S. Trade Representative Jamieson Greer head to Switzerland this morning to begin trade talks with their Chinese counterparts this weekend.

Second, there is plenty of buzz in D.C. this morning that a U.S. - U.K. trade deal may be signed by both sides later today. This would be the first agreement with a significant trade partner to get across the finish line since President Trump's "Liberation Day" announcement.

Third, and this one is perhaps more significant in the moment than are the previous two. It appears that the Trump administration will not be enforcing the Biden administration's AI Diffusion Rule, which was to go into effect on May 15. The rule, which was planned in the final days of the Biden administration in January, divides the world into three tiers, subjecting most nations on the planet to capped access to AI-capable semiconductor chips.

The Trump administration, according to reports across several news outlets, seeks to do away with the tiered system, which it calls "overly complex" and would like to deal with chip export nations on an individual basis. This could be good news for chip purchasers in India, Switzerland, Mexico, Israel, Saudi Arabia and the United Arab Emirates. This is almost certainly good news for the likes of industry leader Nvidia NVDA and its closest AI chip designing competitor, Advanced Micro Devices AMD. Readers are aware that I re-initiated long positions in both of these names earlier this week.

Marketplace

The S&P 500 and the Nasdaq Composite both returned to their winning ways on Wednesday, with respective gains of 0.43% and 0.27%. The Philadelphia Semiconductor Index ran 1.74% for obvious reasons. The all-important (to economic growth) Dow Transports popped for a gain of 0.72%. Eight of the 11 S&P sector SPDR ETFs closed in the green on Wednesday, led by Technology XLK and followed by the Discretionaries XLY and Health Care XLV. The Materials XLB easily led on the downside.

Winners beat losers on Wednesday by a 5-to-3 margin at the NYSE and by a rough 5 to 4 at the Nasdaq. Advancing volume took a 58% share of composite Nasdaq-listed trade and a 52.2% share of composite NYSE-listed activity. Meaningful? Maybe. Maybe even... probably. Aggregate trade increased by 14.7% on a day over day basis for Nasdaq-listings and by 5.7% for NYSE-listings. Volume was also higher on Wednesday on an "up" day across the membership of the S&P 500 than it had been during either of the two preceding days, which were "down" days.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 234K, Last 241K.

08:30 - Continuing Claims (Weekly): Last 1.916M.

08:30 - Non-Farm Productivity (Q1-adv): Expecting -0.4% q/q, Last 1.5% q/q.

08:30 - Unit Labor Costs (Q1-adv): Expecting 5.3% q/q, Last 2.2% q/q.

10:00 - Wholesale Inventories (Mar): Expecting 0.5% m/m, Last 0.5% m/m.

10:30 - Natural Gas Inventories (Weekly): Last +107B cf.

1:00 p.m. - Thirty Year Bond Auction: $25B.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: CHH (1.37), COP (2.05), CROX (2.49), MTCH (.66), PLNT (.62)

After the Close: AFRM (.32), COIN (1.95), DKNG (-.07), LYFT (.20), MCK (9.83), RKLB (-.09), TTD (.25)

At the time of publication, Guilfoyle was long RKLB, NVDA, AMD equity.