Trump's Rattling the Cage. But Rattle Too Much and Things Start to Crack

Let's look at possible consequences of tariffs as a 'negotiating tool' and the odd results of that consumer confidence survey.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The furious pace of executive orders and headlines coming out of the Trump Administration continues. And the chaos both are creating could have ripple effects on markets, especially as the tariff tough talk could force countries and companies to shift plans.

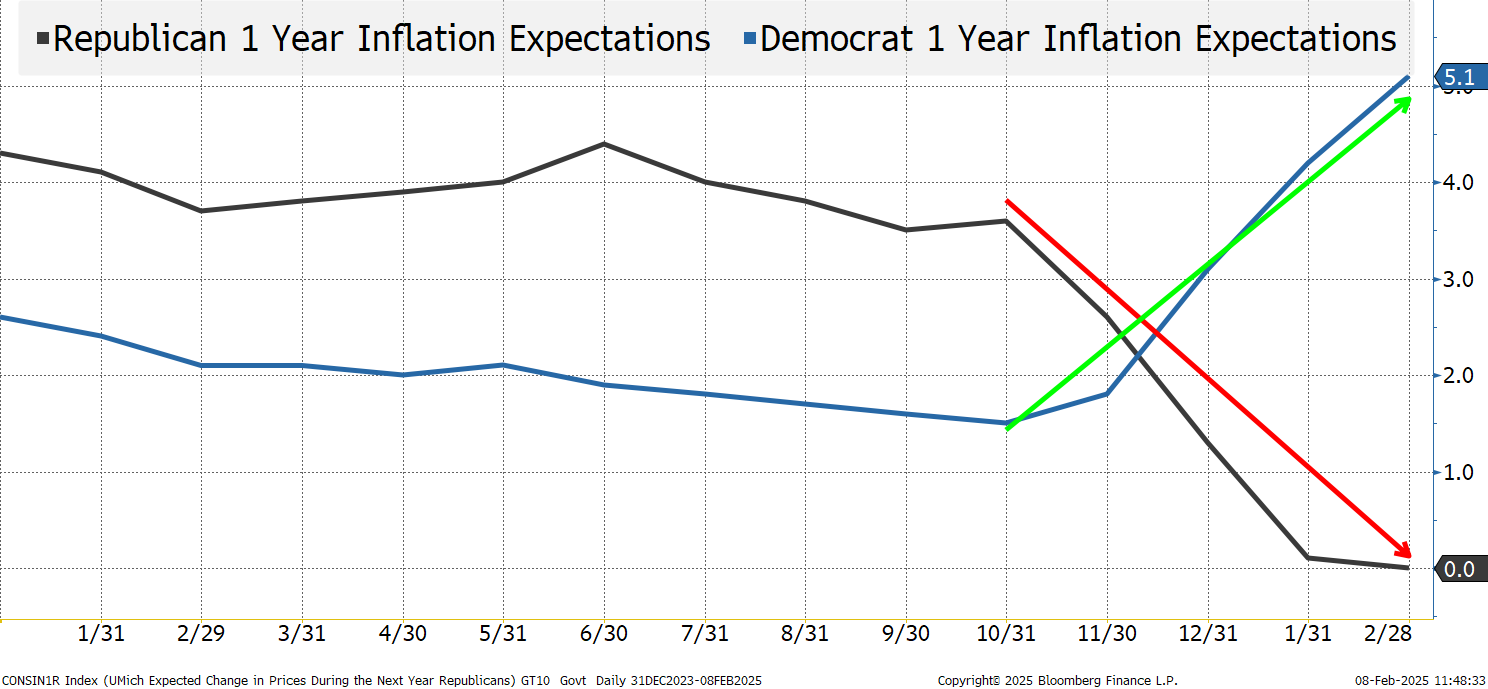

But let's look at an interesting survey that landed on Friday: The University of Michigan Consumer Confidence data. By late Friday morning, the stock market had started to decline. Until that moment, it had done fairly well, even as yields increased on the back of the jobs report. Then out came U-Michigan report, showing one-year inflation expectations jumping from 3.3% to 4.3%. The move raised some questions I’ve often had about inflation expectations:

- Why does the Fed place so much weight on inflation expectations, particularly from survey data?

- Inflation, for professionals, is difficult to estimate with any degree of certainty, why would individuals be better at it? I’ve always felt a response choice from high, above average, average, below average and low would be more helpful.

- But in this particular report, the discrepancy between Republicans and Democrats is almost mind boggling to me:

I am surprised by how big this discrepancy is and makes me question the veracity of the data that helped cause markets to move on Friday.

Tariff Talk

Reciprocal tariffs also came up on Friday, adding to the problems stocks and bonds were facing. This is very much in line with my current concerns and view that this year will be messy, but manageable.

The market seems to have settled on the view that these are all just negotiating ploys. That has led to muted or short-lived market reactions. While we were fully on board with fading last weekend’s tariff war (kind of comical to write that sentence), we are not so comfortable fading tariffs now.

Both Canada and Mexico got 30-day reprieves (to some extent) just for agreeing to do what they had already been planning to do on some level. Small win for the president, but not overwhelming. In the case of Canada, I expect the president to decide that it wasn’t enough, and he needs more tariffs. I think that is a mistake for many of the reasons (regarding supply chains) listed last weekend in my report, "The New Trump Tariffs." The complexity of existing agreements and the efficiencies built into the supply chain will be disrupted, causing more harm than good for both countries.

There are many in the administration (presumably based on U-Michigan responses) that like the idea of getting more and more revenue from tariffs (to cut taxes). I cannot say that I completely disagree with that view, but it could be taken to extremes.

You can rattle the cage (so to speak) so often before the people inside that cage start making some plans of their own. Tariff uncertainty, even if intended to be a bargaining tool, could turn into tariffs depending on the responses, but could also cause changes to supply chains as companies get tired of the risk. If you assume, as I do, that supply chains are fairly optimized to be efficient, changes (for whatever reason) will be problematic (with inflation being the first potential issue).

Expect more noise on tariffs as the market has become too complacent, and I think that it is now far more likely to face a downside, rather than an upside, surprise from “negotiations.” A different view from what I had last weekend, but things move fast in 2025.

Bottom Line

Look for moderately higher yields.

On equities, look for some overall weakness in U.S. markets. Expect value- and equal-weighted indexes to outperform market-weighted indexes. Be wary of small caps. As much as I’d like to include small caps in my list of outperformers, they seem more likely to bear the brunt of tariffs and policy mistakes than large companies. Just above 5,800 on the S&P 500 is my target, with risk of a big move to the downside if markets decide we’ve been too optimistic about what can be done quickly. Longer term I’m optimistic, but I don’t like the overall market right now (especially since I don’t think yields/the Fed will be helpful).

Look for foreign markets to outperform the U.S. (positioning is so tilted the other way, that it won’t take much to get this going). Especially if the dollar continues to increase on the back of tariffs.

I don’t like commodities themselves, but I do like the commodity producers and those companies that play an important role in the extraction and processing of commodities.