Trump Trades Up in Asia

Let's look at the president's newest trade deals, chart the market and see what's ahead this week.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Rock! Rock! (Till You Drop)

Hold on to your hat, hold on to your heart

Ready, get set to tear this place apart

Don't need a ticket, only place in town

That'll take you up to heaven and never bring you down

Rock, rock, 'til you drop

Rock, rock, never stop

Rock, rock, 'til you drop

I say Rock! Rock! To the top

- Lange, Clark, Allen, Savage, Elliott, Willis (Def Leppard), 1983

One Heck of a Start!

The Trump administration announced a series of trade deals over the weekend as the president began his key trip to Asia in Malaysia to speak at the 47th Association of Southeast Asian Nations summit in Kuala Lumpur. The trip will culminate later this week in South Korea when Pres. Trump and Xi of the U.S. and China will meet at the Asia-Pacific Economic Cooperation Forum.

The president traded off reduced tariffs for deals that include such items as rare earth metals and minerals with southeast Asian nations ahead of that meeting, which after the Australia deal last week, further strengthens the U.S.' hand going into the later part of the week. Southeast Asia in aggregate, is now a larger source of goods for U.S. purchasers than is China, so this is fairly huge news. The U.S. struck deals with Cambodia, Thailand, Malaysia and Vietnam.

The deal with Cambodia has that nation dropping all tariffs on U.S. agricultural and industrial imports in exchange for an exemption of its 19% tariff on hundreds of Cambodian exports to the U.S. Thailand, similarly, has agreed to eliminate trade barriers on 99% of U.S. exports to that nation including industrial and agricultural goods in exchange for exemptions on a number of goods facing 19% tariffs in the U.S. Both of these nations agreed to offer U.S. customers preferential access to rare earths and critical minerals.

The president also announced new or more detailed / enhanced deals with both Malaysia and Vietnam. While Vietnam has become a key exporter of goods to the U.S, Malaysia became the third nation over the weekend to agree to provide the U.S. with access to rare earths and /or critical minerals. Perhaps the real topper over the weekend, was the U.S. president's announcement of a formal ceasefire between Cambodia and Thailand after the two nations clashed earlier this year. Cambodian Prime Minister Hun Manet announced his intent to nominate Pres. Trump for the Nobel Peace Prize for his efforts in brokering the peace deal.

The Warm-Up Act

U.S. and Chinese officials both reported progress described as "constructive" in trade talks over the weekend as U.S. Treasury Sec. Scott Bessent and Chinese Vice Commerce Minister Li Chenggang met in Kuala Lumpur ahead of this week's meeting between the heads of state of the world's two largest economies. The Treasury Sec. was quoted in the Wall Street Journal saying, "I think we have a very successful framework for the leaders to discuss on Tuesday." The Journal also quoted the Vice Commerce Minister commenting that "The two sides have reached preliminary consensus."

These preliminary talks covered many issues that have come between the U.S. and China such as export controls over key products and / resources, cooperating in the tamping down of the illicit fentanyl trade and the suspension of increased reciprocal tariffs. Specific trade talks covered rare earths, agricultural products, semiconductors, and even the Tik Tok social media property.

According to the Journal, Bessent was asked if the U.S. and China would extend the trade truce that had been set to expire on Nov. 10th (250th birthday of the United States Marine Corps, by the way). Bessent responded, "Coming out of this meeting, I would say yes, but that is at the end of the day, President Trump's decision."

In a Sunday morning appearance on the CBS News show "Face the Nation," Bessent told Margaret Brennan that China intends to make "substantial purchases of U.S. soybeans. Hmmm... Where have I heard that one before?

Not Everything Came Up Roses

Late Friday afternoon, Pres. Trump announced that an additional 10% tariff would be imposed on imports from Canada after the province of Ontario had run an anti-tariff T.V. ad that had been spliced and pieced together featuring former U.S. Pres. Ronald Reagan's words from a 1987 radio address in order to mischaracterize Reagan's intent.

Reagan was actually, in that particular address, explaining why he had to impose new tariffs on Japanese exports. Reagan's intent and the fact that he was increasing tariffs at the time are not mentioned in the ad. Ontario agreed to pull the ad, but not until after the second game of the World Series, which this year involves the only Canadian-based team in Major League Baseball. This obviously angered the U.S. president. Hence, the increased tariffs.

Markets

Equities had a strong five-day period last week. In fact, stocks had their best week since early August with several indexes including the S&P 500 and Nasdaq Composite closing out the Friday session at all-time records. There were a number of catalysts. The third-quarter earnings reporting season has gotten off to a markedly better than expected start. In addition, the confirmation on Thursday of the upcoming Trump - Xi meeting and Friday's release of a cooler than expected September consumer price index report for September got traders and investors fired up ahead of this week's Federal Open Market Committee policy meeting.

The Week That Was...

What the mid-major to major U.S. equity indexes did last week, as stocks hit new records for the first time since early October, yes early October (LOL)...

- The S&P 500 gained 0.79% on Friday and 1.92% for the week.

- The Nasdaq Composite gained 1.15% on Friday and 2.31% for the week.

- The Nasdaq 100 added 1.04% on Friday and 2.18% for the week.

- The Russell 2000 gained 1.24% on Friday and 2.5% for the week.

- The S&P Smallcap 600 popped for 0.83% on Friday and soared 3.02% for the week.

- The S&P Midcap 400 gained 0.58% on Friday and 2.32% for the week.

- The Dow Transports added just 0.22% on Friday but lost a nasty 1.41% for the week.

- The Philly Semis ran 1.89% on Friday and 2.94% for the week.

- The KBW Bank Index soared 2.07% on Friday and a whopping 3.62% for the week.

On Friday, six of the 11 S&P sector SPDR ETFs closed out the session in the green, led higher by Technology (XLK) , the Utilities (XLU) and the Financials (XLF) . Energy (XLE) easily led the losers.

For the week, nine of the 11 S&P sector SPDR ETFs traded higher with Technology again, leading the pack at +3.02%. Energy and the Industrials (XLI) both gained more than 2% over the five days. Two defensive sector funds, the Utilities and the Staples (XLP) closed in the red for the week.

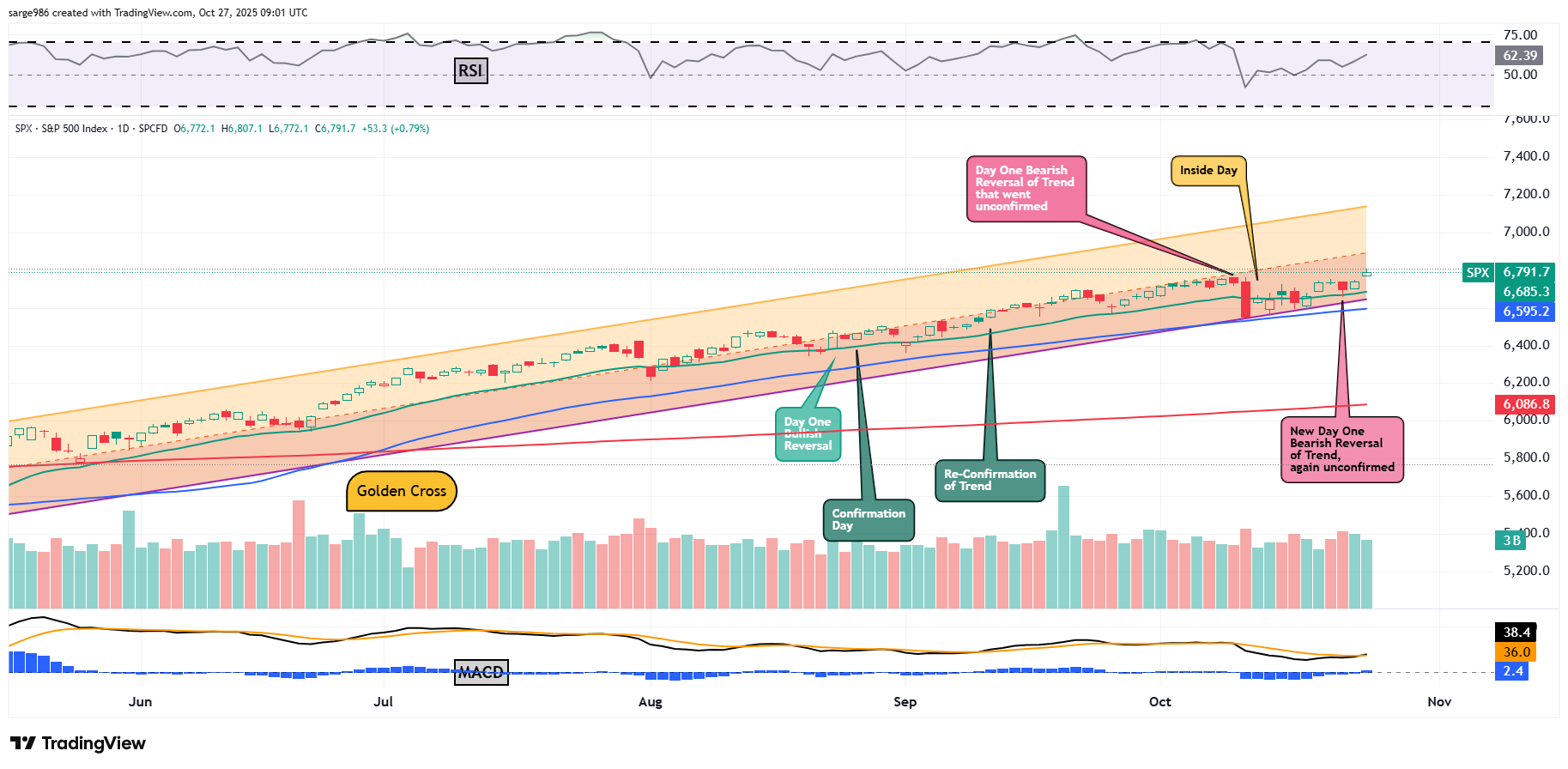

The Chart...

Last week, we discussed the "Inside Day" that occurred on Monday, Oct. 13 and how it had signaled a short-term decrease in volatility. Since that day, noted in yellow above, the S&P 500 has continued to work its way higher, despite two true (and three overall) failed attempts to confirm a "Day One" bearish reversal of trend. At this point, despite an honest attempt to shake investors out of this market in October, which was something we had predicted in this column, the S&P 500 remains on its bullish trek.

Trekking where? Not that there won't be more profit taking or another attempt to shake us out, but markets remain on trend for a positive holiday season / year end run as economic growth resumes with the end of the government shutdown, lower taxes kick in, easier monetary policy is implemented by the FOMC and the U.S. experiences some mild disinflation (not deflation) going forward.

Readers will note that Relative Strength for the S&P 500 has returned to its more robust stance, after reaching into neutral territory two weeks ago. The indicator remains nowhere near reaching into anything that looks to be technically overbought. The daily Moving Average Convergence Divergence is also starting to look a bit more bull friendly.

Within that indicator, the histogram for the 9-day exponential moving average has crossed back above the zero-bound. That's probably short-term bullish. In addition, the 12-day EMA has crossed back above the 26-day EMA, while both of those lines remain in positive territory. These are short to medium-term bullish signals.

Earnings

According to FactSet, for the third quarter, with 29% of the S&P 500 having reported, 87% of those companies have pleasantly surprised on earnings while 83% of those companies have surprised in the right direction on revenue generation. The fast start to earnings season and increased guidance in general, has boosted the blend of Q3 earnings results / growth expectations for the S&P 500 to 9.2% from 8.5% last week and from just 8% two weeks ago. Revenue growth expectations now stand at 7.0%, up from 6.6% last week and up from 6.3% two weeks ago. For the full calendar year of 2025, Wall Street now sees S&P 500 earnings growth at 11% on revenue growth of 6.3%, up from 6.2% last week.

Back to the quarter, Technology, the Financials, Utilities and the Materials are expected to be the outperformers with projected earning growth of 18% or more. The Materials are new here as last week, realized and expected growth for the sector improved from 13.1% all the way to 18.0%. Just three sectors are now projected to suffer a year-over-year earnings contraction led to the downside by Energy. Last week, the Consumer Discretionaries sector saw consensus for its y/y earnings growth for the quarter rise from -1.3% to +0.3.

Valuation

Still using data provided by FactSet, and aided by improved forward looking guidance, the S&P 500 ended last week trading at 22.7-times 12 months' forward-looking earnings, up from 22.4-times a week ago. This is still well above the five-year average of 19.9 times for the index as well as its 10-year average of 18.6-times. The S&P 500 also ended last week trading at 28.8-times trailing 12 months' earnings, up sharply from 28.4-times a week ago. That also stands well above the five-year (25 times) and ten-year (22.8 times) averages for the index.

Ten of the 11 sectors are still trading above their five-year average valuations, led by Tech (30.3 times) and Consumer Discretionaries (28.9 times). Only the REITs (18.1 times) are not historically overvalued relative to their five-year averages.

The GDP Game

Last week, the Atlanta Fed left their GDPNow model for the third quarter unrevised at growth of 3.9% (q/q, SAAR). Among other regional central bank district branches running close to real-time GDP models, the New York Fed's estimate for Q3 growth was revised up to growth of 2.35% from 2.34% a week ago. The Cleveland Fed's model for the third quarter remained unrevised at growth of 1.99%, while the St. Louis Fed model too was revised higher from a paltry 0.42% to a slightly less paltry 0.59%.

There remains nothing close to a Fed consensus on just how robust economic activity was during the third quarter. It appears that as we expected that the regional Fed districts that run these models are very close to halting the regular updating of said models until there is something close to a regular release of federal data to go on.

Fed Funds Futures

Fed Funds futures trading in Chicago are now pricing in a 97% probability for a quarter-percentage point rate cut this Wednesday afternoon and a 95% likelihood for another quarter point cut on Dec. 10. Those probabilities are down from 99% and up from 94%, a week ago. At present, there are now just a half-point worth of additional rate cuts fully priced in (78% chance) for all of calendar 2026. down from three-quarter points a week ago.

On The Docket...

Without a lot of macroeconomic data to go on with the government shutdown now in its 27th day, investors and traders have had less information to act on in recent weeks. This week, however, even without government agencies reporting their respective numbers, there will be plenty to take in....

... The FOMC will release its next policy statement this Wednesday. The group will end their media blackout period at 2:00 p.m. that day with its official policy statement where a short term rate cut of a quarter point is currently priced into financial markets. Fed Chair Jerome Powell will hold his press conference a half hour later. As anyone making a living off of said financial markets well knows, the press conference is often the most important part of "Fed Day." The FOMC will not again update their economic projections until the December meeting.

.... As long as the government shutdown continues, the macroeconomic calendar will remain light. Once the government reopens, trying to track all of the data will be close to overwhelming for economists, but only the most recent data will matter to traders.

... This Thursday is the "big day" of this market week as long as the Fed does as is expected. On Thursday, Pres. Trump and Xi of the U.S. and China will meet on the sidelines at the APEC summit in Gyeongju, South Korea, and, we hope, cement a trade deal already at least partially agreed to by their respective lieutenants. If a trade deal were too much to ask for, another extension of the current trade truce would be enough to keep Wall Street happy.

.... The earnings calendar will be especially heavy this week, with big tech / the Mag 7 taking center stage. While way too many "headline" level corporations to list will report their quarterly numbers this week, the focus will fall upon Alphabet (GOOGL) , Meta Platforms (META) and Microsoft (MSFT) this Wednesday afternoon followed up by Amazon (AMZN) and Apple (AAPL) on Thursday afternoon. Throughout the week, investors will also hear from United Parcel Service (UPS) , Visa (V) , Boeing (BA) , Caterpillar (CAT) , CVS Health (CVS) , ServiceNow (NOW) , Starbucks (SBUX) , Eli Lilly (LLY) , Mastercard (MA) , Merck (MRK) , Chevron (CVX) and ExxonMobil (XOM) among many others. Readers and fans of the daily "Stocks Under $10" series will be focused on SoFi (SOFI) earnings this Tuesday morning.

.... In other corporate, but not earnings-related, news, Honeywell (HON) will spin off its advanced materials business this Thursday. Honeywell shareholders will receive one share of Solstice Advanced Materials for every four shares of HON owned as of Oct. 17. The new company will trade under the symbol SOLS. Before we get there, Adobe (ADBE) will kick off its three-day MAX Creativity Conference in San Francisco on Tuesday. Nvidia (NVDA) , Amazon and Dell Technologies (DELL) are expected to present.

Economics

(All Times Eastern)

10:30 - Dallas Fed Manufacturing Index (Oct): Expecting -2, Last -8.7.

The Fed

(All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: KDP (.54)

After the Close: NUE (2.16), WM (2.01), WHR (1.39)

At the time of publication, Guilfoyle was long GOOGL, MSFT, BA, SOFI, NVDA equity.