Trading Up: A China Deal Emerges

Progress is cited in high-level tariff breakthrough, pharma stocks lower as prescription drug executive order set, and let's chart the market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I wanna fly like an eagle

To the sea

Fly like an eagle

Let my spirit carry me

I want to fly like an eagle

'Til I'm free

- "Fly Like an Eagle" Steve Miller (Steve Miller Band), 1976

Sunday Evening

Tick, tick, tick, tick... the world waited with heightened anticipation. OK, maybe not the world, but all traders and investors who make a living in the financial markets waited. They waited for the Sunday evening opening of equity index futures markets on the East Coast. I've always found it a little bizarre how those from other walks of life simply don't know that on Wall Street, Monday morning starts on Sunday evening and that, no, Wall Streeters cannot go out and do something fun on Sunday nights. They have to be at their desks by 6 p.m.

Well, this Sunday night was a much bigger deal than most. This past Thursday, U.S. Treasury Secretary Scott Bessent and U.S. Trade Representative Jamieson Greer traveled to Switzerland to meet with their Chinese counterparts. The volatility, up or down, that had prevailed across U.S. financial markets for months simply dissipated last week, as managers slipped into a more cautionary posture ahead of the event.

These "trade talks" went on for eight hours on Saturday and carried on for several hours into the Sunday session. Both sides were apparently ready to talk all the way into Tuesday, but there would be no need. Pres. Trump posted on social media after the Saturday session had ended, "A very good meeting today with China, in Switzerland. Many things discussed, much agreed to. A total reset negotiated in a friendly, but constructive manner. We want to see, for the good of both China and the U.S., an opening up of China to American business."

💵💰 Everyone’s guessing — our experts aren’t. Get the real playbook for Investing in Uncertain Times at TheStreet Pro’s exclusive Quarterly Meeting on May 14th, 2025 at 12PM ET. (Don’t miss it) 💵💰

'Substantial Progress'

Scott Bessent spoke of "substantial progress" on Sunday afternoon, adding, "We will be giving details tomorrow, but I can tell you that the talks were productive."

Greer commented, "It's important to understand how quickly we were able to come to an agreement, which reflects that perhaps the differences were not so large as maybe we thought."

Wait, Sarge, did he say the word "agreement?" He sure did.

In turn, the Chinese delegation described the meetings as "candid, in-depth and constructive."

Xinhua, the state-run Chinese news agency reported that an "economic and trade consultation mechanism" had been agreed to that would involve recurring discussions. News agencies around the globe reported that the U.S. and Chinese governments will be making a joint statement on Monday.

Needless to say, Asian stocks traded higher, European stocks traded higher and U.S. equity index futures opened higher on Sunday evening only to trade sharply higher than where they opened as the overnight session melted into morning.

What We Do Know...

The U.S. and China have apparently agreed to suspend most tariffs on each other's imported goods. The 20% tariff imposed on Chinese goods over China's role in the trade of the illegal and deadly drug, fentanyl, will stand. The U.S. will cut President Trump's "reciprocal" tariff rate on Chinese goods from 125% to 10%. In return, China will cut their "retaliatory" tariff rate from 125% to 10%.

These reductions are originally set for 90 days, while the two sides delve deeper into these trade talks, which are still evolving. China has also agreed to suspend or completely cancel non-tariff obstacles to free trade adopted in response to the onset of this trade war.

Not only are global equities trading higher, Chinese equities and U.S. equity index futures have soared. In addition, the U.S. Dollar Index has moved higher. Despite the stronger dollar, most commodities are trading higher as well. But precious metals are weaker as there now appears to be fewer investors seeking safe haven. Treasury yields moved higher overnight for the same reason, as investors moved capital from debt securities to equities. U.S. investors should not be surprised to see something of short squeeze this morning as risk managers force net-short portfolio managers to panic.

Targeting Drug Prices

As had been anticipated, Pres. Trump also announced on Sunday, that he would sign an executive order on Monday (today) morning, whose goal will be lowering prescription drug prices in the U.S. The president posted to social media: “Our Country will finally be treated fairly, and our citizens Healthcare Costs will be reduced by numbers never even thought of before. On top of everything else, the United States will save TRILLIONS OF DOLLARS.”

The president is instituting a policy referred to as "Most Favored Nation" where the U.S. government will pay prices for prescription drugs tied to what other countries pay. I have seen estimates where this will cut prices depending on the drug by 30% to 80% for American consumers. Ahead of the event, Moderna MRNA, Eli Lilly LLY, and Merck MRK led big pharma lower, as those stocks gave up 12.17%, 10.81% and 8.67% respectively over the past week. For that week, the Dow Jones US Pharmaceuticals Index gave back 7.03%, while the Dow Jones U.S. Biotechnology Index lost 6.43%.

The Numbers

What the major to mid-major U.S. equity indexes did as equity markets struggled through the week just completed. Volatility obviously took an early May break.

- The S&P 500 gave up 0.07% on Friday and 0.47% for the week.

- The Nasdaq Composite closed flat on Friday and down 0.27% for the week.

- The Nasdaq 100 closed down just 0.01% on Friday and down 0.2% for the week.

- The Russell 2000 gave back 0.16% on Friday but gained 0.12% for the week.

- The S&P Small Cap 600 gained just 0.03% on Friday and gained 0.52% for the week.

- The S&P Mid Cap 400 lost 0.08% on Friday but gained 0.49% for the week.

- The Dow Transports surrendered 0.64% on Friday, but just 0.26% for the week.

- The Philly Semiconductors gained 0.81% on Friday and 1.58% for the week.

- The KBW Bank Index gave up 0.21% on Friday but gained 0.85% for the week.

On Friday, six of the 11 S&P sector SPDR ETFs closed in the green, led higher by Energy XLE and the REITs XLRE, while Health Care XLV took a moderate beating. The Financials XLF closed flat for the session.

Similarly for the week, six of the 11 sector SPDR funds closed in the green, led in a northerly direction by the Industrials XLI at +1.14%. Health Care was absolutely roasted over the past five days, giving up 4.22%. Big pharma was simply steamrolled ahead of Pres. Trump's expected executive order later this morning targeting prescription drug prices.

Earnings

First quarter earnings season is now getting down to the late innings as those still left to report mostly come from the ranks of the retailers along with some stragglers from the tech sector. This has been a much stronger than expected earnings season so far. According to FactSet, with about 90% of the S&P 500 having reported, 78% of firms so far have beaten earnings expectations while 62% of firms so far have beaten expectations for revenue generation.

On a year-over-year basis, the S&P 500 is now running at a first-quarter blended (earnings & expectations) growth rate of 13.4% for earnings, up from 12.8% last week and just 7.2% several weeks ago. Revenue growth is running at 4.8%, up from 4.6% two weeks ago. Interestingly, it still appears that the first quarter may have pulled economic activity forward from the second quarter. Consensus for Q2 earnings growth is down to 5.2% from 5.7% a week ago and from 9.1% five weeks ago. Q2 revenue growth is currently seen at growth of 4.0%, down 4.6% a little more than a month back.

For the first quarter, health care is currently running way ahead of the pack, with earnings growth of 42.9%. Communication services is a very distant second place at growth of 29.1%. Three sectors are still expected to post Q1 earnings contractions, down from four sectors two weeks ago, led lower by energy (-12.7%) and staples (-6.7%).

For the full calendar year of 2025, Wall Street now sees earnings growth of 9.3%, down from 9.5% a week ago, and 11.3% five weeks ago. Expectations for full year revenue growth have fallen from 5.4% to 4.9% over those same five weeks.

As far as valuation is concerned, the S&P 500 went into this past weekend trading at 20.5 times forward looking earnings, up from 20.2 times a week ago and 25.3-times 12-month trailing earnings, up from 25.1 times a week back. These valuations are both now well above their five-year averages of 19.9 times for forward looking earnings and 24.8 times for trailing twelve-month earnings, respectively.

The GDP Game

Last week, the Atlanta Fed revised their GDPNow model for the second quarter up to growth of 2.3% (q/q, SAAR) last week from 1.1% the week prior. There is still no estimate for Q2 GDP ex-the gold trade at this time. Among other regional central bank district branches running close to real-time GDP models, the New York Fed's estimate for Q2 growth now stands at 2.42%, up from 2.34%, while the Cleveland Fed still sees Q2 growth of 1.97%.

The St. Louis Fed finally published their initial model for the second quarter at growth of 1.51%. Where is my trusted Hedgeye Nowcast Model? After literally nailing the initial BEA estimate for Q1 GDP, Hedgeye's model for the second quarter is running just below 1.4%.

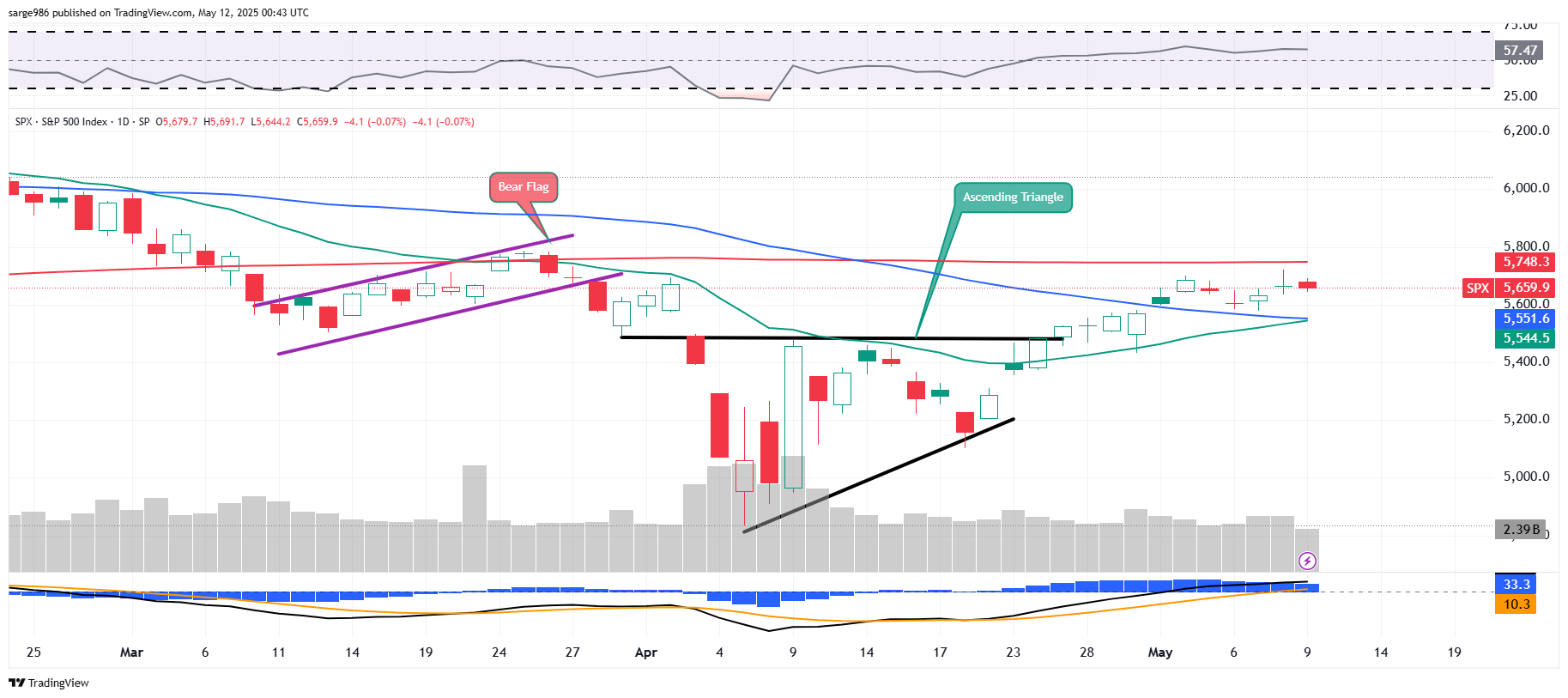

The Chart...

Not a lot has changed since last Monday. The breakout from the bullish ascending triangle pattern that we had discussed in past weeks, grew a little cautious going into this weekend's trade talks between U.S. and Chinese officials in Switzerland. It is worth noting that as the S&P 500 sagged mid-week, there was notable support found at the 50-day simple moving average. Expected resistance at the 200-day simple moving average was never tested from below. It may be this morning if overnight equity index futures prices are any indication.

Relative Strength remains strong, but not close to overbought. More interestingly, the daily Moving Average Convergence Divergence for the S&P 500 is now quite bullish in posture as the 26-day exponential moving average has moved above the "zero-bound" below the 12-day EMA with the histogram of the 9-day EMA still in positive territory. Markets really could not ask for a more bullish short-term set-up than that.

What's Ahead?

- The domestic macroeconomic calendar is extremely heavy this week. Inflation will be the name of the macro game for the week ahead. The headline events of the week will be the Bureau of Labor Statistics' releases of April consumer price index on Tuesday and April producer price index on Thursday. On Friday, we'll see April import and export prices as well as the University of Michigan's advance release of its Consumer Sentiment survey for May. This will include both one-year and five-year inflation expectations. In addition, April Retail Sales and April Industrial Production will cross the tape on Thursday morning.

- The Federal Reserve will be visible this week, in the wake of last week's policy decision. The docket is not extremely heavy with public speaking appearances, but two stand out: Fed Vice Chair Philip Jefferson will speak on Wednesday morning followed by Fed Chair Jerome Powell on Thursday morning from Washington.

- The earnings calendar is the lightest we have seen in more than a month. But there are still several headline-level corporations set to release their numbers over the next few days. On Wednesday afternoon, Cisco Systems CSCO will go to the tape followed on Thursday morning by Deere DE and Walmart WMT. That afternoon, Applied Materials AMAT and Take Two Interactive TTWO will report.

Economics (All Times Eastern)

2:00 p.m. - Federal Budget Statement (Apr): Last $-161B.

The Fed (All Times Eastern)

10:25 - Speaker: Reserve Board Gov. Adriana Kugler.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: MNDY (.70)

After the Close: SPG (2.91)

At the time of publication, Guilfoyle had no positions in any security mentioned.