Trading Safer Than Investing, KOSPI Down, RTX & Lockheed at White House

The chart tells me it's safer to trade right now, weapons makers go to Washington, and South Korean stocks get hurt amid war on Iran.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Metal Health

Well, I'm an axe grinder

Piledriver

Mama says that I never, never mind her

Got no brains

I'm insane

The teacher says that I'm one big pain

I'm like a laser

Six-string razor

I got a mouth like an alligator

I want it louder

More power

I'm gonna rock it till it strikes the hour

- Banali, T. Cavazo, C. Cavazo, Dubrow (Quiet Riot), 1983

You Kids Ready?

It's 28 rounds in a 30-round clip. Why? So, you don't eff up the spring. Now, they say that's bull. I'll stick to what the Vietnam vets told me, thank you very much. Iodine pills in the water. Tastes like crap. Better do it. Are you freaks ready for Wednesday? It may get nuts out there.

Financial markets moved around violently on Tuesday. Sort of like Monday. Equities opened deep in the hole. Then the "take 'em" boys showed up to grab the dip. Only this time, those dip buyers could not take the bus all the way home. This time, they left the major indexes dangling with losses. This time the S&P 500 would not kiss its 21-day exponential moving average. Swing traders checked out. This time, the S&P 500 could not kiss its 50-day simple moving average. Professional managers said "Hang on a sec." Everyone asks, "What now?" Everyone wants to know if the 200-day simple moving average is now in play.

The war in the Middle East, which only started on Saturday, poses some real risk to energy markets if not global economic growth. That's not necessarily a bad thing, at least strategically. OPEC and friends have agreed to increase production. We all know that the frackers in the U.S. can do the same and probably even overdo it. I think the threat of increased inflation beyond the short-term due to the difficulty in transporting energy-related commodities is probably overblown.

The threat to the global economy? That's a different matter. There's no doubt that the removal of inexpensive, not to mention illegal Venezuelan and Iranian oil from the black market will put a dent in mainland China's ability to maintain the recent pace of growth in its gross domestic product. There is no doubt that the removal of mass produced inexpensive and illegal Iranian weaponry from the playing board will make it difficult for Russia to keep its boot on Ukraine's neck. Are those net positives in the long run? You are the judge. All the while; the world's largest sponsor of global terrorism is neutralized.

Friday!

February jobs day? Sure. More importantly, Reuters is reporting that executives from major defense contractors to include both RTX Corp (RTX) and Lockheed Martin (LMT) will be at the White House to discuss the increased pace of production for certain offensive and defensive weapons. RTX has already agreed to a deal to produce 1,000 new Tomahawk missiles per year. We need more.

The 2025 reconciliation bill calls for $25 billion to purchase munitions and increase that production. Better make it $50 billion. There will likely be a supplemental bill written to that effect. The president said on Monday that the U.S. has a "virtually unlimited supply" of munitions. The president added "Wars can be fought forever... using just these supplies." I get the messaging. The walls do have ears. The fact is that the major defense contractors are cash flow beats. That fact will not change anytime soon.

Holy South Korea!

The KOSPI Index sold off 7.24% on Tuesday, which was the most severe selloff for South Korea's blue chip equity index since 2024. Foreign investors were recorded as having sold a record $3.5 billion in Korean equities for that day as Samsung Electronics and SK Hynix gave up 9.9% and 11.5% respectively. Why? Simple. Concerns that there will be a major price shock due to the war in the Middle East that impacts the market for Liquefied Natural Gas.

The South Korean economy is heavily reliant upon LNG to provide energy, and the two Korean semiconductor manufacturers require a great deal of energy to keep their fab facilities online. It gets worse. On Wednesday, the KOSPI Index continued with its crash, giving up 12.1% for the day. Remember, there are circuit breakers in place, so crashes occur in slow motion nowadays. It's not like 1987 when we had to simply take it on the chin, but at least that crash was over in a day. The Kosdaq, which is South Korea's home to small and medium-sized companies, lost 14% on Wednesday.

Samsung Electronics gave back another 12% on Wednesday as SK Hynix gave up about 10%. I'd like to blame the selloff on market concentration as these two names make up almost 50% of the KOSPI in terms of weighting. But the even deeper losses at the Kosdaq defy that logic. This may be a simple case of foreign investors exacting the repatriation of capital in a time of crisis from a market where they have the largest profits. Year to date for 2026, the KOSPI had been up an incredible 48% coming into this week and is still up 21%. That's on top of the 75.6% gain made by that index for the full calendar year 2025. I think they'll be OK.

Marketplace

European markets are now open. That was mixed. U.S. equity index futures have swung from heavy losses to sharp gains just in the past couple of hours, so we do have that. The U.S. Dollar Index is trading lower after Tuesday's surge. Crude oil seems to be holding Tuesday's gains. Treasury debt securities have not rebounded but do seem to have stabilized. Then there's stocks.

U.S. equities had a rough day on Tuesday, but as we know, now that humans have been almost completely replaced at the point of sale, sentiment plays a smaller role in day-to-day performance than ever before. Sentiment still matters as far as investment is concerned, but trading is done by algorithms and algorithms have no institutional memory.

On Tuesday, the S&P 500 gave up 0.94% as the Nasdaq Composite surrendered 1.02%. Small to mid-caps had an awful day. The S&P 400 lost 1.77% as the Russell 2000 lost 1.79%. Semiconductors? Don't ask. Pressured by what is going on in South Korea, the Philadelphia Semiconductor Index was punished for a beatdown of 4.58% on Wednesday. SanDisk (SNDK) , Micron (MU) and Lattice (LSCC) led the losers.

Note... I had a reader email me and ask if SanDisk was a Korean memory chip maker. For any reader wondering, the answer is "no." SanDisk is very much an American company and was spun off from Western Digital (WDC) about a year ago.

Breadth

Not minty fresh at all. Kind of like what you imagine after eating a sardine & swiss on wheat bread with pesto and onions. Ten of the 11 S&P sector SPDR exchange-traded funds closed out Tuesday in the green as only the Communication Services (XLC) sector was able (just barely) to post any kind of gain. The Materials (XLB) , thanks to the dollar's move and the Industrials (XLI) easily led the losers with Tech (XLK) in third (or ninth) place.

Losers beat winners by a rough seven to two at the NYSE and by about eight to three at the Nasdaq. Advancing volume was able to take a 43.1% share of composite Nasdaq-listed trade, but just a meager 22.1% share of composite NYSE-listed activity. Aggregate trading volume grew on a day-over-day basis as well, making the session's activity more meaningful. Trade increased by a whopping 16.9% across Nasdaq-listings from Monday and by 6% across NYSE-listings.

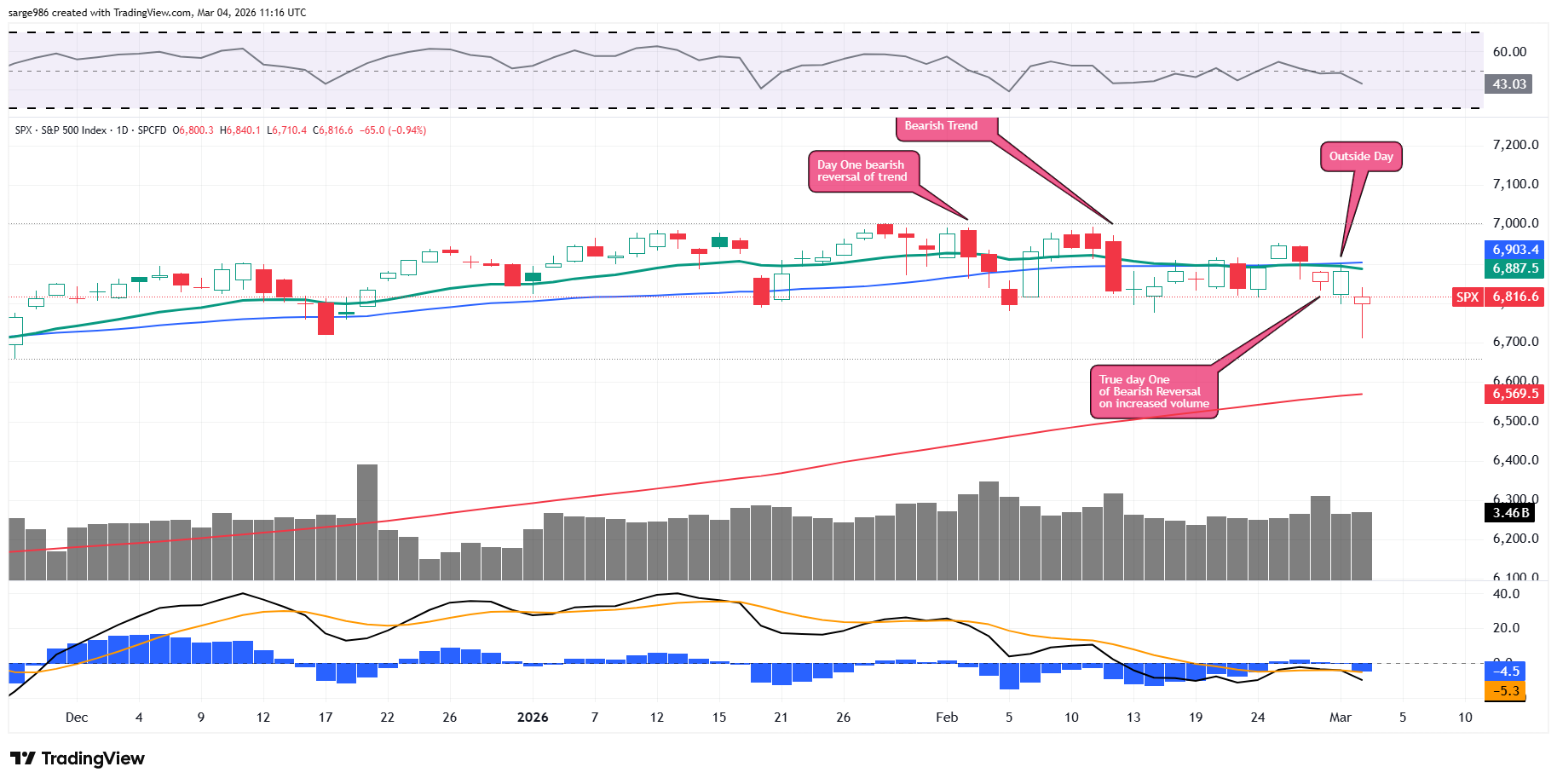

The Chart

Readers will see that the "up" day on Monday, which was an "Outside Day" really did foretell an increase in short-term volatility as we inferred here in this column. The day looks to have possibly been a pause, too, which is a necessary that must appear to confirm a change in trend. Does that mean that Tuesday was a confirmation of a downward change in trend that started last week? Technically, yes. However, one of the requirements is an increase in trading volume.

Note that the increase in trading volume across the membership of the S&P 500 on Tuesday from Monday is so slight, that I am a little cautious in trusting it. One thing I do know is this. If the index cannot quickly reconnect with its 50-day simple moving average, then risk managers will enforce what authority they do have over portfolio managers and force a reduction in overall long-side exposure to large-cap U.S. equities.

That line needs to be engaged with and quickly. Both Relative Strength and the daily moving average convergence divergence are sending warnings. My thoughts? Trading is safer than investing, at least until we see something a little more concrete than this.

Economics

(All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.09%.

07:00 - MBA Mortgage Applications (Weekly): Last 0.4% w/w.

08:15 - ADP Employment Report (Feb): Expecting 47K, Last 22K.

09:45 - S&P Global Services PMI (Feb-F): Flashed 52.3.

10:00 - U of M Consumer Sentiment (March-F): Flashed 102.0.

10:00 - ISM Manufacturing Index (Feb): Expecting 53.5, Last 53.8.

10:30 - Oil Inventories (Weekly): Last +15.989M.

10:30 - Gasoline Stocks (Weekly): Last -1.011M.

The Fed

(All Times Eastern)

2:00 p.m. - Beige Book.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: (ANF) (3.58)

After the Close: (AEO) (.71), (AVGO) (2.02), (OKTA) (.85)

At the time of publication, Guilfoyle was long RTX equity.