Three Key Commodities Heading for Bust as Producers Ignore Inevitable

Cattle, coffee, and cocoa producers have enjoyed historical rallies but unusually high input costs spell disaster ahead.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Cattle, coffee and cocoa producers have enjoyed historical rallies. Unfortunately, unusually high input costs to produce these commodities have left them with a bad taste in their mouths.

Despite high commodity prices and massive cash revenue, profit-making has been difficult for some producers due to elevated energy, labor and fertilizer costs.

Conversations and research have led me to believe that many producers in these categories have assumed the markets will rightfully and automatically compensate them with prices above and beyond their production costs. As a result, they are focused on price appreciation rather than the risk of the inevitable commodity bust. I believe this is a mistake and will add to the downside volatility when it finally arrives.

With enough time, high commodity prices always cure high production prices because of demand destruction and producers flooding the market. I am unaware of an exception to this rule, yet we’ve been repeatedly told, “This time is different."

Extreme weather and aggressive political agendas have caused significant price volatility in recent years. Producers face real hardships, but humans have consistently improved at producing commodities over time due to technological advances, better equipment, and trial and error. In essence, commodity markets can put together spectacular rallies, but they are designed to go down in the long run.

Nevertheless, some markets, such as cocoa and orange juice, go rogue by holding elevated prices far longer than the typical boom-and-bust pattern. Let’s look at the “C” markets on our radar.

Coffee

Just four years ago, coffee prices were so low that producers were suffering from a suicide epidemic. At the time, the Brazilian real was entrenched in a bear market, putting pressure on crop prices in the region. Ironically, the real is just as weak today, but shifts in the currency markets have caused it to have the opposite effect on the price of coffee.

I believe this is temporary and will eventually start working against the coffee rally. During this time, the coffee market suffered from a chronic oversupply due to favorable growing conditions and improved farming methods. At the end of the bear market that ended in mid-2020, the fundamental coffee narrative was so bearish that it would have been unfathomable to predict that prices would more than triple by late 2024.

In my view, we are currently experiencing the opposite scenario. Fundamental analysts are given no reason to expect coffee prices to retreat; despite elevated prices, global demand has remained firm as emerging markets such as China grow increasingly fond of the beverage. Further, droughts in Brazil and Vietnam and later frost in Brazil have thwarted yields and left stocks-to-use ratios tighter than ever. Yet, perhaps all the buyers have already reacted to the outsized bullish news flow; if so, sustaining this pricing will be impossible.

In commodities, the most obvious path for prices based on an overwhelming fundamental narrative is rarely the path markets take. The most common conclusion is an unwinding of overcrowded thinking and positioning.

Everyone loves coffee, but demand is not guaranteed. Prices eventually alter the behavior of consumers and retail businesses that rely on commodities. For instance, some coffee shops have shifted their focus to drinks with less coffee (frappes, lattes and teas). Consumers might trim from two cups to one cup and might entertain the idea of coffee alternatives purported to have more health benefits.

I can assure you that I love coffee more than the average Joe (pun intended), but coffee is not critical for survival. Societal preferences change over time, and high prices encourage such transitions. It wasn’t that long ago that wine makers were swimming in demand and profits. Still, with the younger generation opting for other substances, alcohol, and particularly wine, sales have fallen sharply. Just a few years ago, this would be unimaginable.

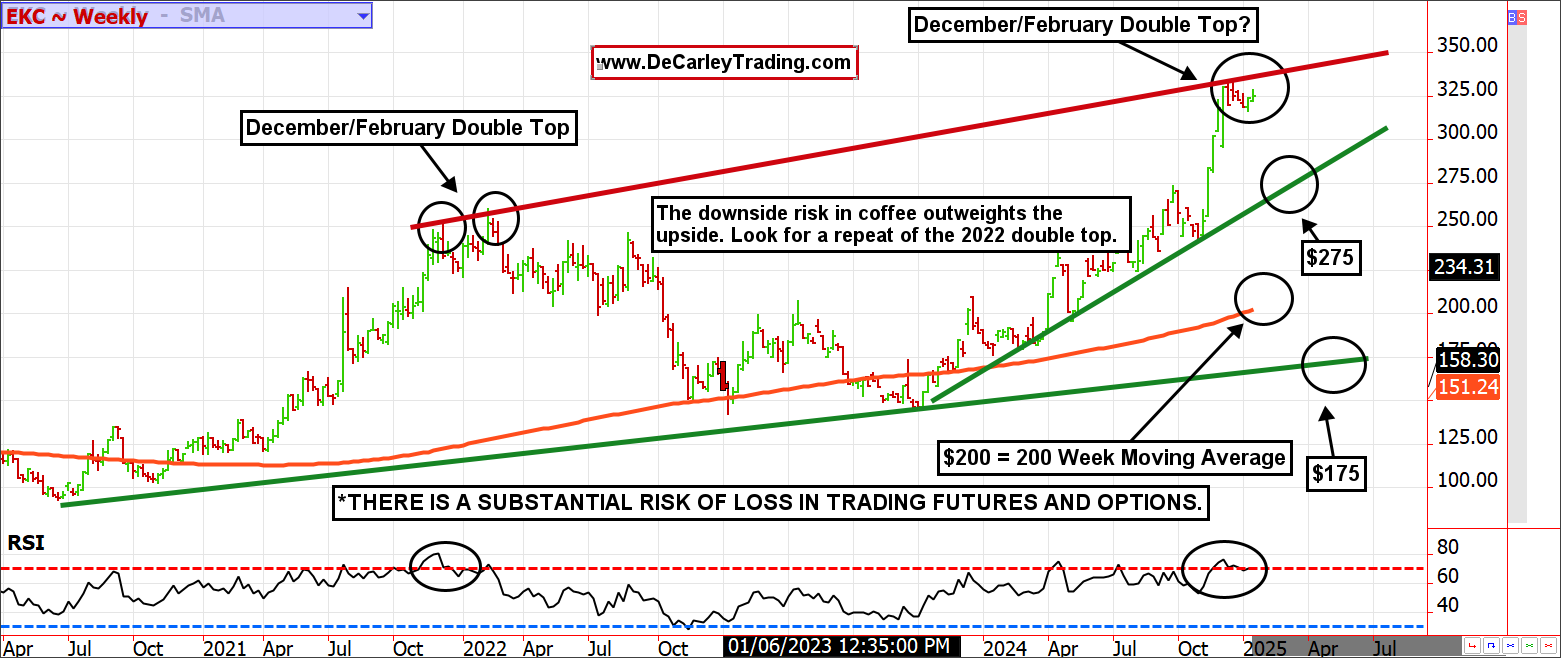

Even if this isn’t the top in coffee, a selloff to the trendline would put us near $275, and the 200-week moving average could act as a magnet; that sits at $200. Finally, another trendline comes in near $175. Markets take the escalator up and the elevator down. We should all be prepared for a $1.00 handle in coffee again; it won’t be next week, but it will almost certainly happen.

Cattle

The U.S. has been facing the lowest per-head cattle inventory since 1951 due to perpetual droughts and a few years of obscenely high feed costs. Like coffee, high cattle and beef prices have not deterred consumers as much as one would expect. Las Vegas Strip steakhouses are charging $80 to $140 for a premium steak and don’t seem to be having any issues filling seats in their restaurants. No thanks.

The bullish narrative for cattle is deafening. Few can imagine a scenario in which cattle prices decline. As a result, we are getting word of an uncivilized cash market in which buyers are willing to acquire beef at any cost. This feels like the 2006 real estate market in Las Vegas and Phoenix; nobody questioned price, math or their ability to pay; they only cared about the acquisition. In the years following, homes in Las Vegas collapsed by as much as 80% in some zip codes (including mine).

We can’t see the future, but I’ve seen what has happened in the past when humans behave in this manner. The last time cattle supply was similarly tight was in 2014 (and before that, it was 60-plus years prior); the result wasn’t higher prices. The result was a market top that took an entire decade to regain.

Cattle prices are bumping against a trendline, and the monthly RSI diverges from the underlying futures price. Cattle can go higher, but the gains would likely be temporary.

On the other hand, the downside risk is deep and real. The pain could be prolonged when the rug is finally pulled on the cattle market. Thus, ranchers should be hedging aggressively up here. The risk of being early to hedge is minimal, but the risk of being late could be catastrophic.

Cocoa

The cocoa market has wholly disconnected from reality and fundamentals. The price of cocoa hasn’t quite figured that out yet, but eventually it will. We believe anything above $6,000 was and is out of bounds. Prices will eventually revert to a normal range under $6,000 and probably closer to $2,000. We wouldn’t trade it with either futures or options due to a lack of liquidity and massive margins.

Yet, we wanted to point it out as an example of a commodity market that has gone rogue. This chart should linger in our minds whenever we speculate on other commodities. There is no limit to the chaos in markets because emotional human behaviors have no limit.

At the time of publication, Garner had no positions in any securities mentioned.