This Is the Part About Tariffs Nobody Is Saying Out Loud

Although specific tariffs will impact some products individually, there is a bigger story and concern you should know about.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The jury is still out on how tariffs will impact commodity prices. There will be winners and losers across sectors and products; those details will reveal themselves and change daily. Thus, it is a fool's errand to try to predict the future by guessing how the next X or Truth Social post will impact the markets. All we can do is be aware of what happened the last time we found ourselves in this environment.

The bigger story is how the tariffs change the economic landscape and how individuals alter their behavior accordingly. The Trump administration, particularly Treasury Secretary Scott Bessent, has told us its goal is to thwart inflation and interest rates. Tariffs appear to be their tool of choice.

The economic reset and uncertainty that come with tariffs are deflationary. This is because if stock prices retreat, the wealth effect also subsides. If consumers perceive themselves as “less wealthy,” they close their wallets, and prices soften.

Current statistics suggest that 10% of top earners consume half of the goods and services sold in the U.S. This population group is likely many of the same people who have amassed small fortunes with asset price appreciation (homes, stocks, crypto). In short, the heavy-lifting group might suffer the most from an asset decline. If so, consumer spending becomes vulnerable.

Additionally, if stocks continue to behave more like risk assets than a printing press for risk takers, then Treasuries could rally as investors seek a safe haven. Portfolio reallocation might be all that is needed for interest rates to go lower.

What Does All of This Mean for Commodity Prices?

If we move to a lower inflation and low-interest rate environment, commodity rallies will be smaller and selloffs will be longer due to changes in investor behaviors (money flows). Although most have forgotten due to a few years of wild commodity market volatility, commodity markets are designed to go lower over time. This is because technology is deflationary, and as time goes on, we generally become better at producing renewable agriculture or even non-renewable fossil fuels.

Without inflation pressures, the days of massive influxes of cash into markets like crude oil and corn to hedge a portfolio from inflation are behind us. In recent years, we have seen multiple inflation hedges take commodity prices for a ride that fundamentals couldn’t support. Eventually, those markets returned to levels that made more sense; corn and soybeans are prominent examples. Further, if the government begins removing underlying stimulus from the economy (excess money supply and government spending), the heyday of speculative euphoria is also behind us. To illustrate, meme stocks like GameStop GME, cryptocurrencies, and commodities such as crude oil, natural gas, and even cocoa and coffee probably wouldn’t have been as dramatic if the economy wasn’t awash with money created in the aftermath of the pandemic.

Against the Grain

Let’s look at a few markets, including grains (mainly soybeans). During the last Trump administration, the trade war with China suffocated soybean demand. Beans traded from about $10.50 into the $8.00 area. Corn was deflated before Trump entered office but remained subdued between $4.50 and $3.00.

We are entering Trump 2.0 with grain prices at the higher end of the Trump 1.0 tariff war envelope. We believe the market had priced most of the tariff tantrum before the 47th President ever stepped foot in the White House. Nevertheless, significant and sustainable rallies will be challenging.

Down Baby, Down?

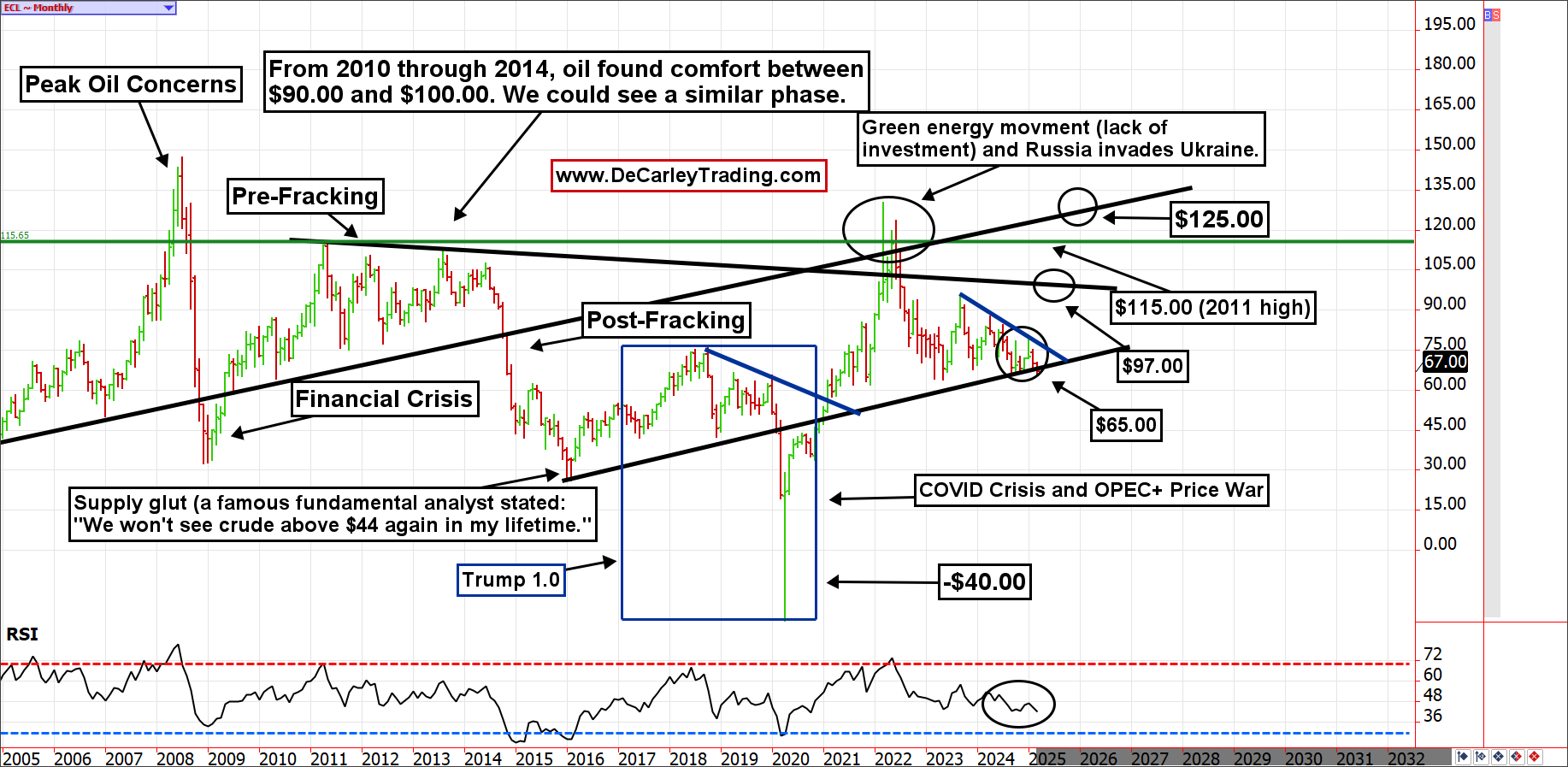

The new administration has made its “drill baby, drill” policy regarding crude oil well-known. However, it feels like the market has incorrectly adjusted its opinion of what constitutes high and low crude oil prices.

Since the Russian invasion of Ukraine, a consensus has decided that $65.00 per barrel is cheap. Yet, in a post-fracking world, $65.00 to $70.00 is expensive for all intents and purposes. What we saw in 2022 and 2023 was an exception. If so, a break below trendline support in the mid-$60.00s could quickly revisit $50.00 and maybe even $40.00 oil.

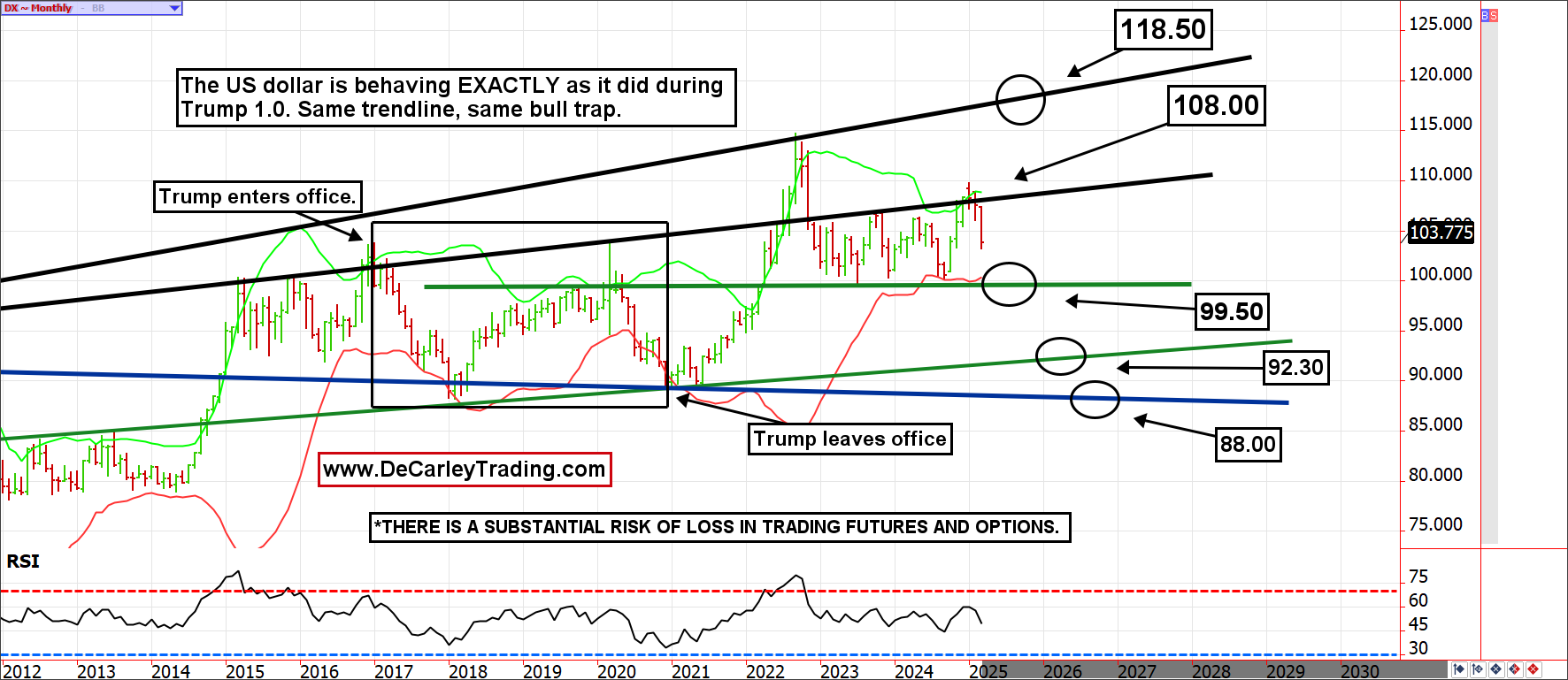

Dollar's Behavior Mirrors Trump 1.0

Some are surprised by the dollar's weakness following the Trump inauguration, but the market merely mirrors what happened last time. Ironically, the same trendline that rejected the dollar rally in Trump 1.0 has done so thus far during the sequel. If history repeats, the greenback selling could be just getting started.

Lower interest rates and inflation should allow the chart analysis to play out. We wouldn’t be surprised to see the dollar index deep into the 90.00s. Eventually, this would be considered bullish for most asset prices but before we get to that juncture, we likely need to see more froth removed from risk assets.

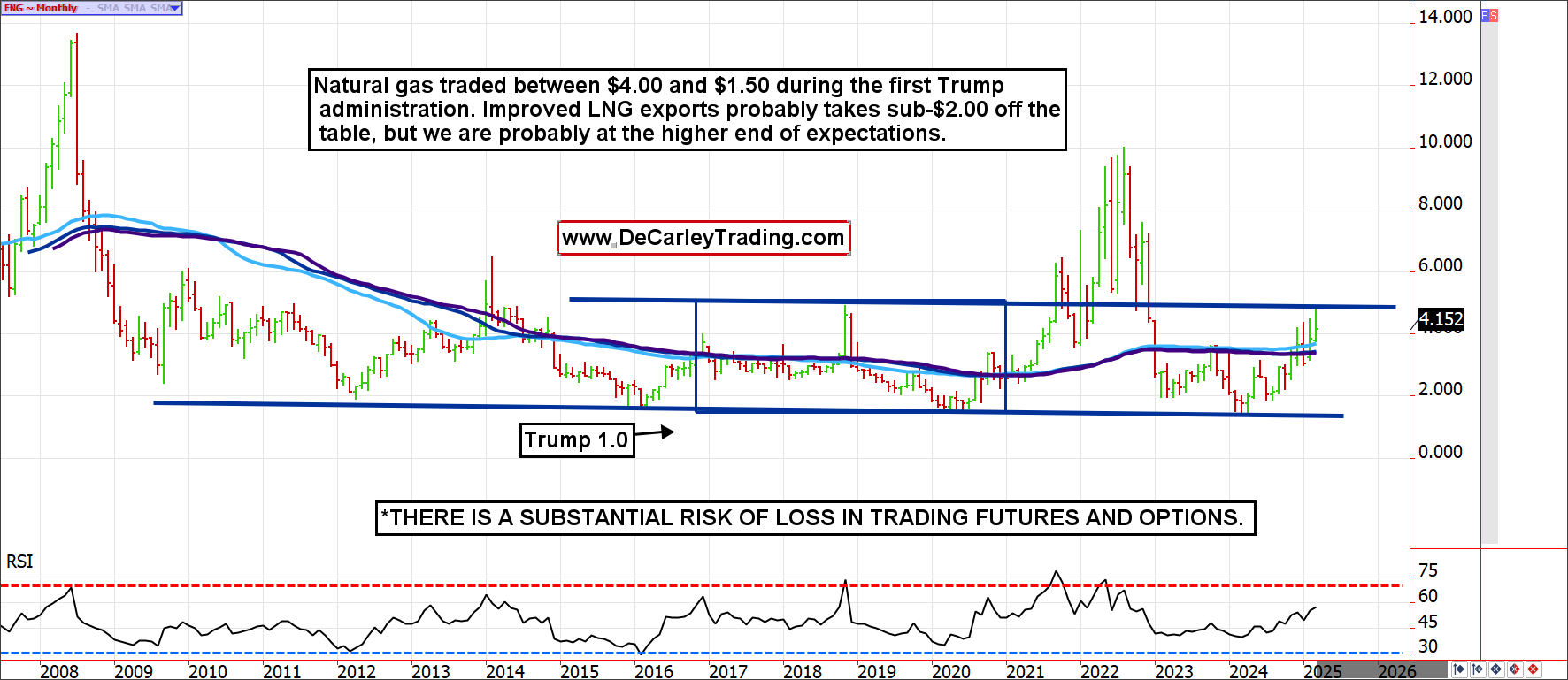

Burned by Natural Gas?

Finally, natural gas. The bulls are excited about natural gas prospects due to the sudden realization that gas is a relatively clean energy source, and the U.S. and its trading partners are working on developing liquid natural gas exports. However, we cannot ignore the fact that more oil drilling will increase the natural gas supply.

Further, gas is still being flared (burned to expose of it) in some parts of the country. Thus, despite hopes of stronger demand, the supply side of the equation is a drag on price.

Bottom Line

In summary, although specific tariffs will impact some products individually, the more significant concern is economic contraction as investors, businesses, consumers, and trading partners work out the details of their new reality. Moreso, Trump 1.0 tariffs didn’t result in widespread inflation, albeit they were disruptive; Trump 2.0 tariffs are likely to prove deflationary.