This Commodity Market Eerily Resembles 2014. That's Not a Good Sign for Bulls.

Will the market repeat 2014? If a seasonal and repeat pattern play out as expected, here's what to expect, including the most common strategy during this time of year.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In 2014, the corn market was coming off a wild inflationary cycle, during which prices were in the $8.00-per-bushel range. The selling finally dried up near $4.00 before rallying about $1.00. By May 2014, the market had begun to soften; by September, the harvest lows reached close to $3.30.

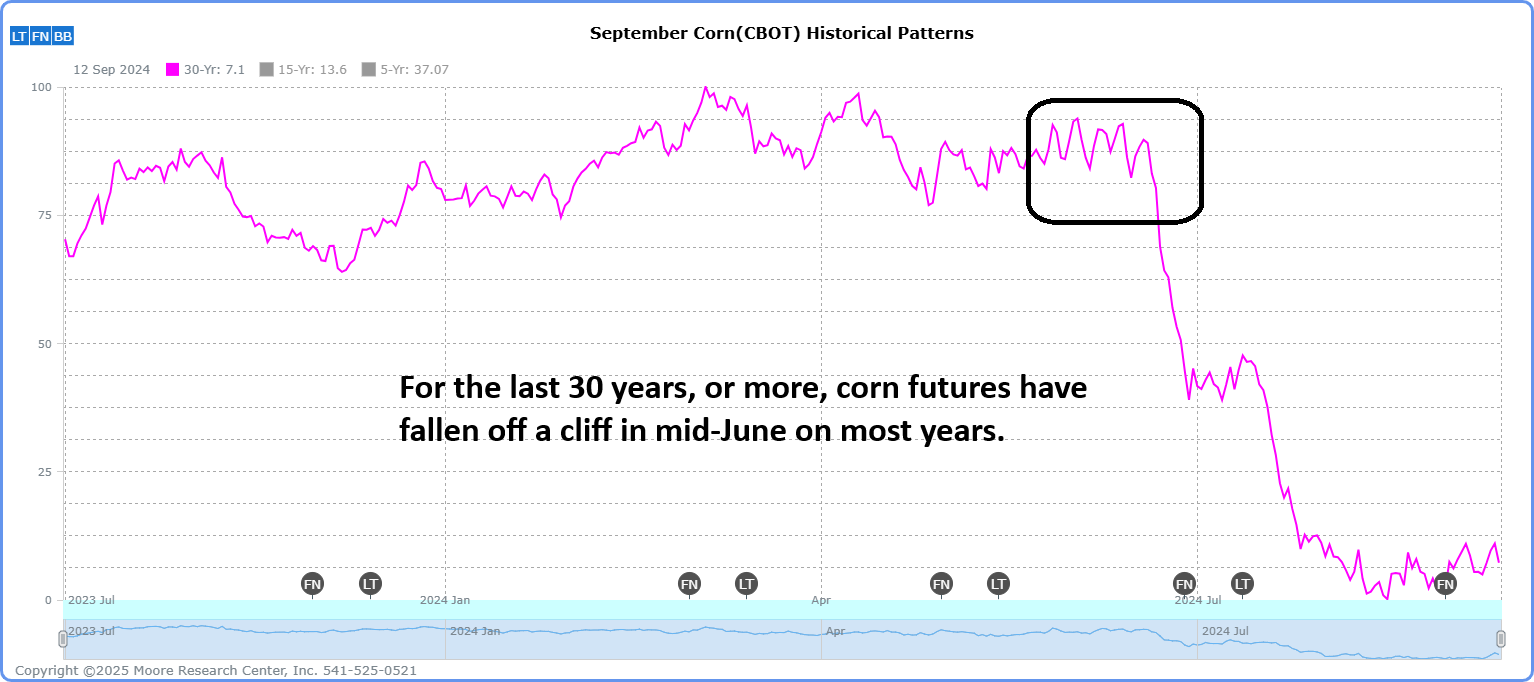

Unless something surprises the corn market in the next week or two, it will be difficult for prices to find a different path this time around.

Can Mother Nature alter the course of the corn market? Yes. But the window of opportunity for such an event is closing quickly. The seasonal high for corn is due next week, and the die already appears to be cast.

Every year, commodity funds begin a selling campaign in mid-June, and we would expect any WASDE report rally to be sold into. In fact, during this time of year, the most common strategy is to sell 10- to 20-cent rallies aggressively.

If this seasonal and 2014 repeat pattern plays out as expected, the monthly trendline near $3.50 would be a reasonable target for the bears and perhaps those speculators looking to play the upside, beginning to put money to work. That said, we wouldn’t expect a return to $5.00 plus pricing. History suggests we will need a few years of “lower for longer” prices to work off the chaos that occurred over the last five years.

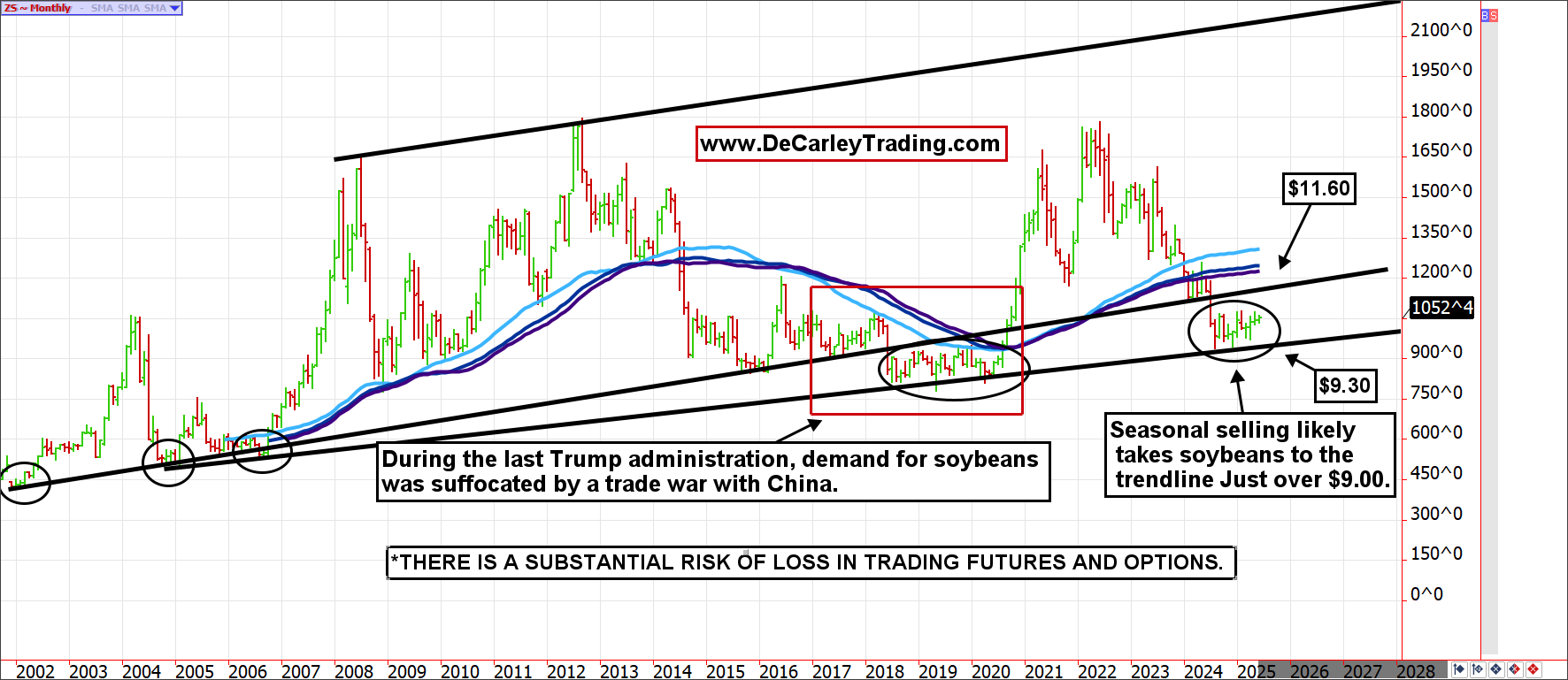

The current soybean chart also resembles the 2014 chart, but we are more interested in the similarities between the previous Trump administration’s trade war with China and the current scenario.

This wasn’t the first rodeo for soybean traders; thus, the market took a step lower before Trump stepped into office to account for the potential of waning Chinese demand. However, we believe that going forward, the two-year stagnation period will likely persist while the trade policy is being worked out. That would likely mean harvest lows closer to $9.00 this season, with any spring rallies limited by $11.60 for the foreseeable future.

It is also worth noting that the grain markets are behaving sluggishly, despite a weaker U.S. dollar. The dollar index, traded on the ICE Exchange, is roughly 10% lower for the year, yet grains are nearly unchanged. Perhaps the currency market has been enabling grain prices to be artificially inflated. If so, a seemingly imminent dollar rally could derail the corn market, pushing prices well into the $3.00s for the front month and soybeans to the low $9.00s.