These Are the 3 Enemies of Trading

Let me show you how focusing on these areas can hurt your investing.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

One of the favorite games of traditional Wall Street and the financial media is predicting market turns. As the market hits new highs, there is a parade of pundits, bears, and pessimists telling us disaster awaits. Despite their historic inability to predict these turns with any degree of precision, they keep on doing it because it attracts attention.

Invariably, the market will correct, and these "experts" will count on the fact that everyone has forgotten they have been wrong for many months and at a much lower level. The secret to being a market timing expert is to keep repeating an incorrect prediction because market cycles will eventually work in your favor. The only thing that matters is the last prediction — not the dozen previous ones that were mistimed.

The Emotional Trap of Doom and Gloom

The problem with this constant stream of doom and gloom is that it drives investors to make emotional decisions. Rather than focus on a strategy for controlling risk, we are tempted to dump our best stocks and lock in gains.

Ironically, bearish warnings often create conditions for even more upside as the market climbs a "wall of worry," squeezes shorts, and promotes a fear of missing out.

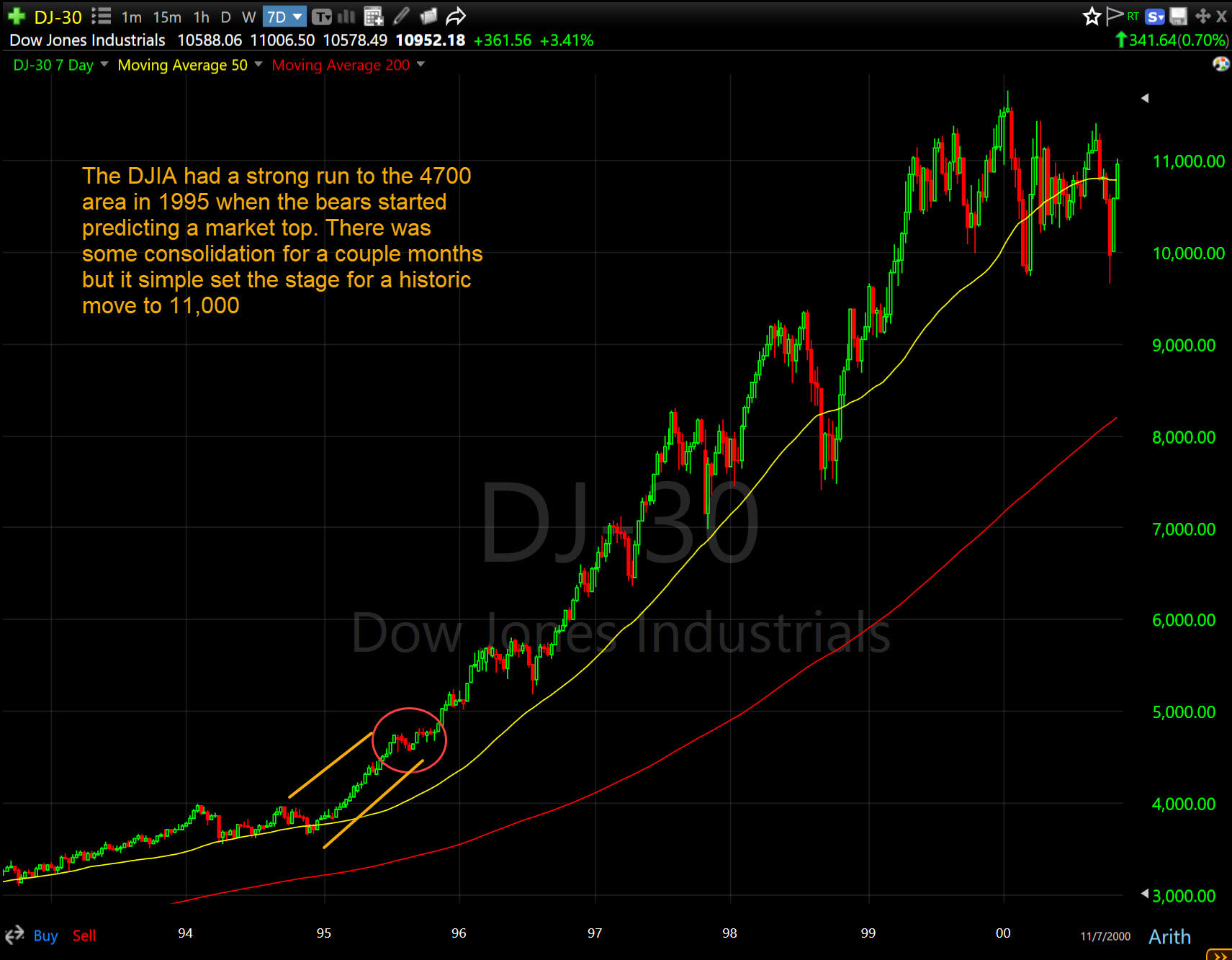

Famed Fidelity mutual fund manager Peter Lynch addressed this issue in an article in Worth magazine back in 1995. The article was titled "Fear of Crashing," and what is particularly interesting is the first sentence: "The Dow's passing 4700 has brought new worries about a nasty correction."

The bears were arguing many of the same things we hear 30 years later: "Too many mutual funds are chasing too few stocks, stocks are overpriced, the dividend yield on the Dow is at an all-time low, and — this one is my favorite — not enough investors are worried."

Here is what happened to the Dow Jones industrial average after it hit the ridiculously extended level of 4700

The Illusion of the Indexes

In that Worth article, Lynch cites the frequency of market corrections. If we update those stats to today, the comment would be: "Stocks have declined 10% or more on over 100 occasions since the turn of the 20th century. That's roughly one correction occurring every 15 months. And on roughly 22 of those occasions, stocks have declined 25 percent or more. That's one nasty bear market roughly every 6 years."

The problem with this data is that the media loves the indexes. If we didn't have indexes, we wouldn't have this problem with emotional reactions to bull and bear markets. If we focus on individual stocks, things are much different.

In a typical year, the median S&P 500 stock has a 52-week high that is approximately 45% to 55% higher than its 52-week low. This is often hidden because when one stock is at its low, another is at its high. The index "smooths" this out. According to recent market studies, roughly 90% of S&P 500 stocks have 52-week ranges wider than the index itself.

Why are we worrying about the volatility of the indexes and the media-created definitions of "correction" and "bear market" when the stocks you own are far more volatile than the indexes themselves?

Anticipation vs. Reaction

Lynch's article contains one of his more famous quotes: "Far more money has been lost by investors preparing for corrections or trying to anticipate corrections than has been lost in corrections themselves."

How do investors avoid this problem of losing money by anticipating market corrections? There are two ways.

The first is to focus on quick reactions to changing price action rather than predicting the future. Don't sell a great stock because someone on television said there is a "bubble" in AI stocks and the market is sure to crash.

There is no question that bear markets and market corrections will occur in the future, but there is no way to time them with great precision. The best approach is to wait for signs of deteriorating price action, then set stops and reduce your risk. You may give back some gains if you keep riding a trend that is extended, but quite often, trends continue far longer than seems reasonable or logical. You build a huge cushion of profits when you ride a trend and can afford not to time an exact turning point. You don't need to sell at absolute tops to produce exceptional returns.

Let Your Stocks Lead the Way

The second way to deal with market timing is to focus on the individual stocks you own rather than the indexes. Let your stocks determine the level of your market exposure. When the stocks you are holding start showing signs of distress, then your money management rules should force you to do some selling and raise your cash levels.

If more stocks continue to break down, then your cash levels will rise, and you'll be in great shape if the indexes start to top. If your stocks are performing well, then you want to hold them regardless of what the indexes may do.

The combination of a reactive approach and focusing on individual stock holdings is the best way to time the market. When you embrace this form of market timing, the predictions of the bears don't sound that brilliant or insightful. They almost never get it right anyway.

At the time of publication, DePorre had no position in any security mentioned.