There's Been a Change in Sentiment, Even if the S&P Hasn't Moved

Investors' concerns have yet to ripple through to stock prices.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

With the rally on Friday, nothing changed. Not the charts, not the indicators. But I cannot stop marveling at the sentiment change in the last few weeks.

We had some high levels of complacency as we headed into February. Oh sure, maybe tech/growth stocks weren’t exactly working well but you had the staples, energy, materials, etc. to trade and tech was treading water. Those ‘others’—the 493-- have stalled out. Very few have given back more than a handful of points but stall they have. That, in my estimation is the result of the overbought condition we saw in the 493.

But sentiment remained complacent.

Then software started crumbling. Sentiment got a bit shaky. Then Alphabet faltered. And Meta’s big earnings pop gave it up. Amazon went plop, following Microsoft back to the spring lows.

Slowly we saw the complacency dissipate. Oh, trust me, it did not turn to fear, but it surely turned to, hey wait a minute, what happened to my growth stocks?

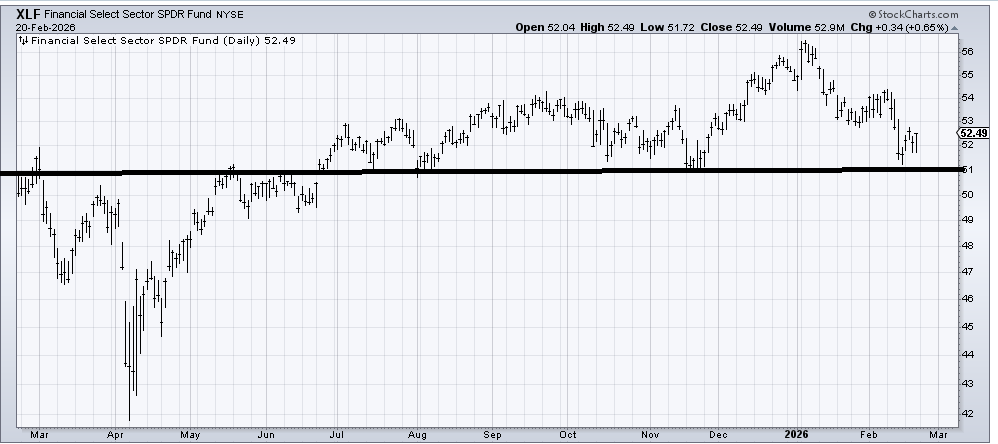

And while software and tech/growth in general was faltering, the financials, which everyone had decided were the place to be in 2026 joined the faltering. The XLF has not broken 51 but do you think all those so bullish on banks and financials entering the year thought the XLF would be down on the year two months in? And do you think any of those folks thought the XLF would be trading where it was in July?

Yes, I know it’s the private credit/private equity charts that have crumbled—heck I have been pointing those charts out to you for months—but even JP Morgan (JPM) , which has not made a lower low (that’s good) is trading where it was in September.

And now everyone is hooting about Blue Owl (OWL) , which I believe I first flagged for you back in September. So sure, it’s a problem, but let’s see if it can hold this 10-ish area for now.

This is a long way to say that maybe it is understandable why, at least using the options ratios, folks are no longer embracing this market as they had two months ago, or even a month ago.

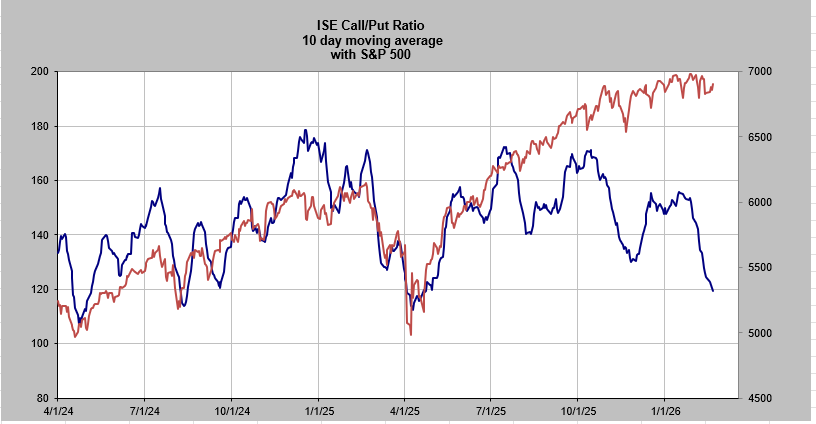

Friday’s rally did not seem to change that, even though beloved big/mega cap tech stocks rallied. The put/call ratio remained elevated, although, not panicky, at .90, despite the market’s rally. The ISE call/put ratio was 1.04. To show you how low that is, it is the lowest reading since April 30th last year when it was double digits at .98.

The ten-day moving average of the ISE call/put ratio is now closing in on the same level it was during the Tariff Tantrum a year ago. What strikes me is that all the other lows in this indicator have seen a commensurate decline in the S&P. Not this time.

This change in sentiment without a serious change in the S&P, which is in its narrowest range to start the year since 1966, is fascinating and I’m not sure what to do about it except continue to believe if we can break down from this S&P range we will see panic in a hurry.